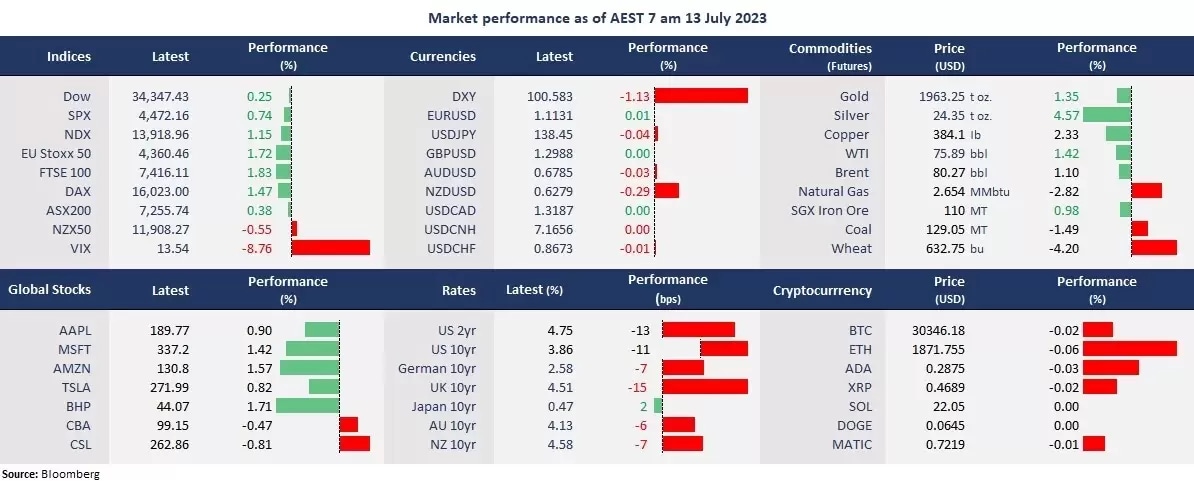

Wall Street posted a three-day winning streak following lighter-than-expected US inflation data. The US headline CPI printed at 3%, lower than an estimated 3.1%, the lowest since August 2021. And the core CPI, excluding food energy, was at 4.8%, also lighter than the 5% expected. Bond yields fell sharply on bets for the Fed to end its rate hike campaign soon. Risk-on prevailed in the equity markets, with growth stocks leading gains. Big tech shares were mostly higher, led by Meta Platforms and Nvidia, both up more than 3%. Banking stocks also extended gains ahead of major earnings as JPMorgan Chase’s shares rose to the highest since February 2022.

A sharp decline in bond yields slashed the US dollar further, with the dollar index down 1.2% to just above 100, the lowest since April 2022. This caused a jump in all the other G-10 currencies, particularly in the Australian dollar and the New Zealand dollar, boosting commodity prices, such as gold and crude oil.

Asian markets are set to open higher. The ASX 200 futures were up 0.87%, the Hang Seng Index futures rose 1.87%, and the Nikkei 225 futures climbed 0.22%.

Price movers:

- 10 out of 11 sectors finished higher in the S&P 500, with Communication Services and Utilities leading gains, up 1.51% and 1.47%, respectively. Healthcare and Industrials were the only two sectors ending in the red finishing flat.

- Nvidia is in talks to help anchor the IPO of Arm Ltd., which is backed by SoftBank. Nvidia was seeking to acquire Arm but unravelled last year. Arm is reportedly in talks with investors, such as Nvidia and Intel, to participate in the IPO deal.

- Apple released iOS 17, featuring contact posters and better auto-correction. The new version of the operation system is available for users to try for free but has not been officially released to the wider public.

- Elon Muskstarts a new artificial intelligence company, xAI, to compete with OpenAI, which backs ChatGPT. Musk was reported to have secured Nvidia's GPU supply to support its large language model plan.

- USD/JPY slumped to the lowest since late May as the dollar declined and bets for the BOJ to tighten its monetary policy strengthened. A breakout of the imminent potential support of 138 may take the pair to 136.

- Both gold and crude oil surged due to the US dollar’s weakness. Gold rose to the highest level since mid-June, while WTI futures topped the key resistance of 75 at a more than two-month high.

ASX and NZX announcements/news:

- Meridian Energy (NZX: MEL, ASX: MEZ) appoints David Carter as a Non-Executive Director with effect from 25 July 2023.

- Mainfreight (NZX: MFT) expects to encounter slowing economic growth in most of the regions in the next 6 to 12 months, indicating high inflation levels weigh on costs.

- Contact Energy (ASX/NZX: CEN) will release full-year Financial Results for 2023 on 14 August.

Today’s agenda:

- New Zealand Food Price Index for June

- Chinese trade balance for June

- US Core PPI