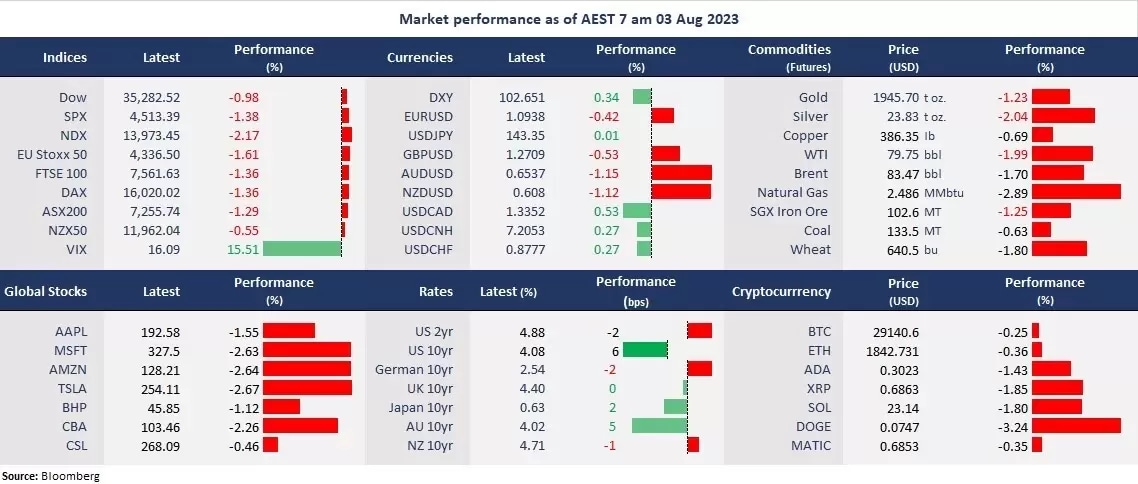

Global stock markets finished sharply lower after Fitch Ratings downgraded the US long-term foreign currency issuer default ratings to AA+ from AAA. The US fiscal management was concerned as the government repeatedly encountered a last-minute discussion on its debt limit, as stated by the rating institution. The debt to GDP ratio almost doubled to 113% in 2007. Wall Street was hit by the unexpected rating cut, coupled with a spike in the long-dated bond yields, sharpening the yield curve. The tech home, Nasdaq, shed more than 2%, and the S&P 500 posted the biggest one-day decline since April.

Fitch’s US downgrade may not be much of a concern itself, but the timing made it a catalyst for the selloff, as equities may be overbought, and a deep correction may have been overdue. The bond jitter was actually triggered by the BOJ’s policy tweak last week when the US 10-year bond yield jumped 12 basis points to above 4%, and it climbed to 4.12% at a point on Thursday, the highest since November 2022.

Risk-off prevailed in the global markets, with the CBOE volatility index surging 16% to above 16 at a one-month high. The US dollar strengthened, sending risker currencies, particularly the Australian dollar and the New Zealand dollar, down more than 1% against the greenback. Commodities were also slashed, with crude futures sliding nearly 2%.

Asian markets closed in a sea of red following Fitch’s US downgrade on Wednesday, with Nikkei 225 slumping 2.3%, the Hang Seng Index losing 2.5%, and the ASX 200 down 1.29%. All 11 sectors in the ASX 200 ended in the red. Futures also point to a lower open across Asia.

Price movers:

- 9 out of 11 sectors finished lower in the S&P 500, with Technology and Communication Services, leading losses, down 2.59% and 2.07%, respectively. Defensive sectors, such as Consumer Staples and Healthcare, outperformed, up 0.25% and 0.06%, respectively, as investors sought safety.

- Qualcomm’s share fell 7% in after-hours trading due to light guidance on declining smartphone demands, despite a beat on earnings expectations. The chipmaker’s earnings per share came to US$1.87, topping an estimated US$1.81. And its revenue was US$8.44 billion, less than the US$8.5 billion expected. The company headset chip sales declined 25% year on year to US$5.26 billion. And it expects earnings of between US$1.80 and US$2.00 per share, at a lower range of consensus of US$1.91.

- PayPal’s shares fell 5.7% in after-hours trading due to a miss on the operating margin in the second-quarter earnings results. The payment platform beat both earnings per share and revenue estimates, reporting at US$0.92 and US$7.29, respectively. However, its adjusted operating margin of 21.4% was below the 22% that the company previously provided.

- WTI futures tumbled below $80 again amid the risk-aversion sentiment.

Despite a larger-than-expected draw in the US inventory data, Fitch’s US credit downgrade pressured risk sentiment as recession fears took the lead on commodity markets again. The US crude stockpile fell 17 million barrels last week, the largest weekly decrease since 1982.

ASX and NZX announcements/news:

- No major announcement.

Today’s agenda:

- Australian Trade Balance for July

- China Caixin Services PMI for July

- BOE Rate Decision

- US Unemployment claims

Maximize your potential gains! Take immediate action and seize the investment opportunities that await you. Login to the platform now!