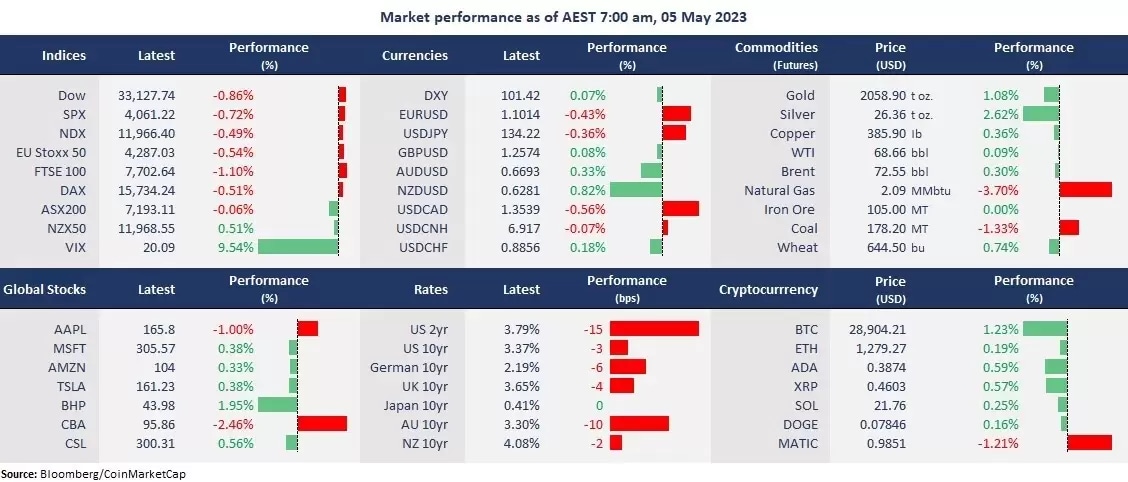

Wall Street fell for the third straight trading day as the regional bank’s rout continued to rattle sentiment. PacWest Bank and Western Alliance Bancorp sank 51% and 39%, respectively, dragging on broad bank stocks, with the KBW Bank Index down 3.7% to the lowest since September 2020. The fear gauge, VIX, jumped 9.5% to above 20 as sentiment soured. The turmoil strengthened bets for the Fed to start cutting rates as early as July. The US dollar strengthened against the Eurodollar after the ECB’s 25 rate hikes as the bank is expected to scale back its tightening steps further despite a hawkish reiteration.

Despite a broad selloff in the cyclical sectors, such as financials, energy, and industrials, tech stocks were relatively resilient, which may be seen to endure better in an economic downturn. Apple’s earnings beat expectations, but the revenue had the second consecutive yearly decline, highlighting a broad growth slowdown in tech companies.

The US non-farm payroll data will also be closely watched, with an expectation that the labour market may show an early stage of slowdown as the US job openings decreased for three months in a row. A weaker-than-expected job data could be bad news as economic concerns are now taking over of Fed’s policy jitters.

Asian markets are set to open lower, with the ASX 200 futures down 0.40%, Hang Seng Index down 0.09%, and Nikkei 225 futures falling 1.75%. However, both Macquarie Group and ANZ bank reported strong half-year earnings, which may buffer the decline in the banking sector.

Price movers:

- 9 out of 11 sectors in the S&P 500 finished lower, with energy, financial, and telecommunication stocks leading losses, all down more than 1%. Real estate and utilities were the only sectors that ended in the green, up 0.92% and 0.73%, respectively.

- Apple’s shares rose 1.4% in after-hours trading amid its Q2 FY23 earnings report as its iPhone sales beat expectations, thanks to China’s reopening. Apple’s earnings per share was at $1.52 vs. $1.43 expected, the overall revenue is at $94.84 billion vs. $92.96 billion expected. Apple services revenue continued its momentum, was at 20.91 billion, or a 5.45% growth from a year ago.

- AMD’s shares jumped 6% on the news that Microsoft is providing financial support to the chipmaker to expand into AI processors, which are called graphics processing units. This AI chip supply is currently dominated by Nvidia, whose shares are seen soaring amid the recent ChatGPT-bolstered demands.

- Oil prices bounced off a session low and finished flat, as the crude oil may have been oversold in the last few sessions. The WTI futures fell about 7% at a point to an 18-month low but rebounded swiftly and finished slightly higher. A softened USD also helped buoy the oil market.

- Gold rose for the third straight trading day but pulled back from a session high as the precious metal faced technical resistance near its all-time high level of 2,070. However, the upside momentum stayed strong and may continue lifting gold to a fresh high.

ASX and NZX announcements/news:

- Macquarie Group (ASX: MQG) reported the FY23 net profit at $A5.18 billion, up 10% from a year ago. 2HFY23’s net profit was at $A2.88 billion, up 25% from 1HFY23, and up 8% from 2H22. The bank’s international income accounts for 71% of its total income. The final ordinary dividend is $A4.50, 40% franked.

- Australia and New Zealand Banking Group Limited (ASX/NZX: ANZ)’s half-year FY23 net interest income increased 20% to A$8.5 billion from a year ago, driven by higher average net loans. Its deposits and other borrowings increased by A$62.8 billion to A$843 billion, up 8% from the same period last year.

Today’s agenda:

- RBA May monetary meeting minutes.

- China’s Caixin services PMI for April.

- US non-farm payroll for April.