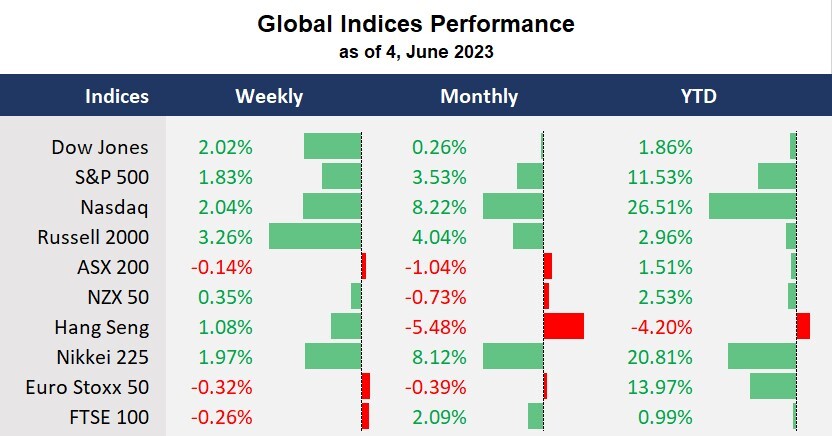

Friday’s strong job data continued to buoy Wall Street, with the three US benchmark indices finishing higher for the week, and all 11 sectors in the S&P 500 ended in the green, suggesting stock markets have switched on the risk-on turbo amid the debt bill’s passage and Fed’s signal for a rate hike pause. At the same time, the tech-rally led Nasdaq to gain for the sixth straight week, up 27% year-to-date, and was the longest winning streak since 2020. Meantime, the fear gauge, the CBOE volatility index, fell to 14.6, also the lowest level since February 2020, before the pandemic-induced market crash. “Go with the flow” may be the case this week, and the economic data we will be watching are primarily from the APAC region, as there will be a relatively quiet week from the US. The RBA’s policy meeting will be in the spotlight, and the country’s first-quarter GDP should also be on investors’ radar.

Notably, the Hong Kong stock markets posted a weekly gain for the first time in the last nine weeks, kicking off June on a front foot. This may suggest that the Chinese stock markets could have been oversold, and the government is expected to further expand its stimulus measures amid the faltering economic reopening. This week, the Chinese trade balance, CPI, PPI, and New Yuan loans are the influential economic data that may impact the APAC region market performance, commodity prices, and related currencies.

What are we watching?

- The USD eases gains: The dollar index finished flat for the week after swinging in directions. The USD’s movement is in check as the Fed may be set to pause the tightening campaign after ten consecutive times of rate hikes since January 2022. Notably, the fund rate-sensitive US treasury, the 2-year bond yield spiked 17 basis points amid Friday’s job data, suggesting that the reserve bank may resume the rate hike cycle even if it suspends hiking in June.

- Chipmaker’s stocks lose steam: The AI-related chipmakers’ stocks, including Nvidia, AMD, and Broadcom’s shares, all finished lower for the week after an AI-powered surge. This could have been caused by profit-taking, suggesting a technical correction may be near.

- Crude oil slips: China’s bumpy economic recovery sparked concerns about weak demands in the oil markets, despite a two-day rebound in crude prices last week as traders bid for a further production cut by the OPEC +. However, any disappointing news from the cartel may continue to crash oil prices.

- Gold encounters a technical selloff: Gold has been pressed by a strengthened USD and risk-on sentiment in May, and a double-top pattern was still in play. The precious metal may still face further downside pressure in the near term.

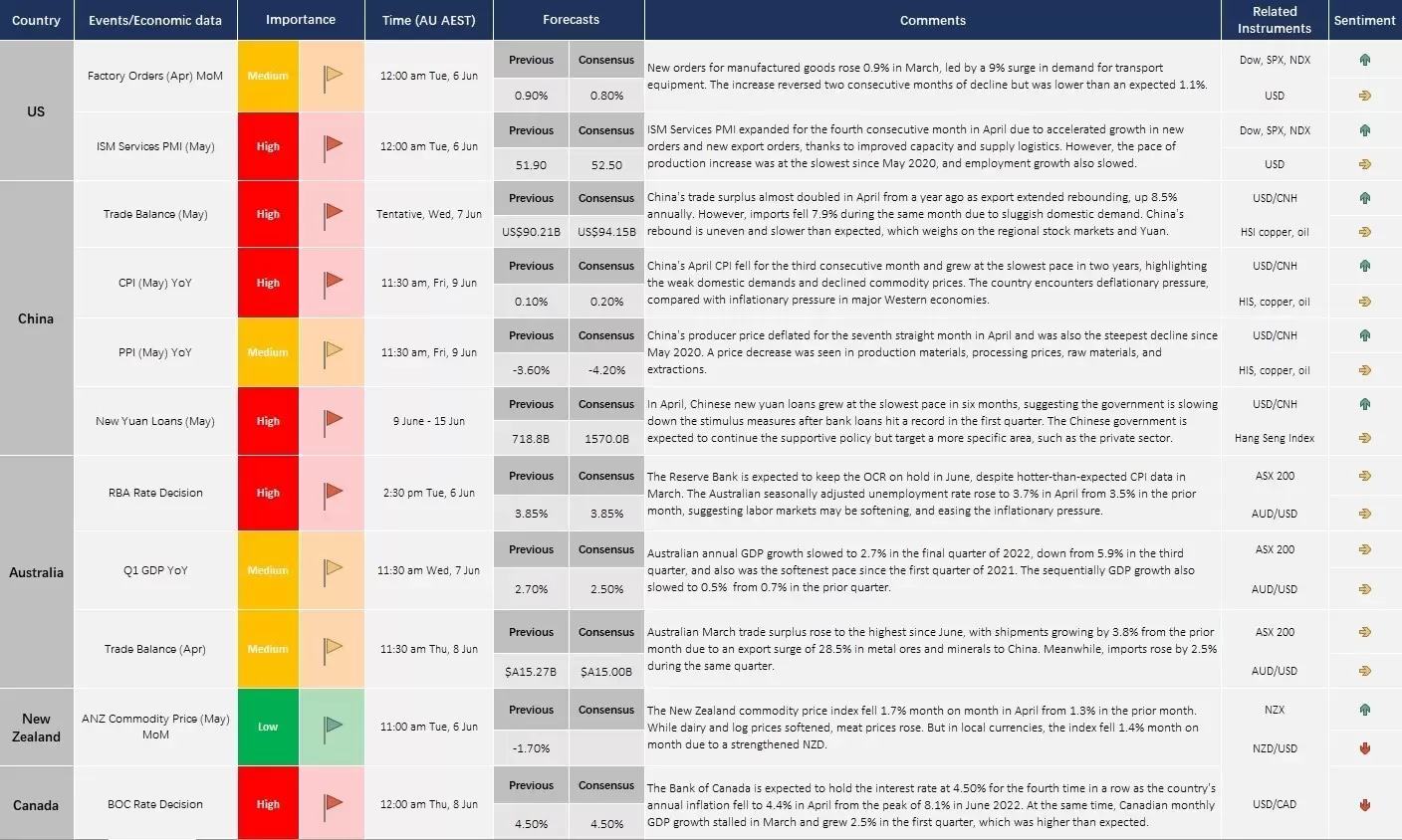

Economic Calendar (5 June – 9 June)