US tech shares were on fire and led Nasdaq to enter a bull market, up more than 20% year-to-date. Well-known tech companies are all rushing into the AI race to attract investors and seek new growth. At the same time, the Fed is expected to pause its rate hike campaign in June, adding to the optimism. This again makes an argument between market “bulls” and “bears,” as the rally does not reflect the recent economic woes over the bank’s rout. The rebound in the US dollar and rates complicates asset allocations, where only those AI-related tech companies are leading the market gains.

On the political front, though the US debt ceiling talk is still in a stalemate, history proved that lawmakers would eventually reach an agreement to avoid a sovereign default, and markets seemed not bothered by the government’s drama so far. In the meantime, the G-7 meeting was another distraction to market players, which tended to intensify geopolitical tensions between the US and China.

Nonetheless, investors will still focus on the economic front, including the FOMC meeting minute, the US GDP, and the chipmaker’s leader Nvidia’s earnings. And the Reserve Bank of New Zealand is also due to decide on its policy rate, which is expected to carry on its hawkish stance.

What are we watching?

- The king dollar returns: The US dollar regained ground in the last two weeks as bond yields started climbing again, suggesting markets were not expecting the Fed to start a rate-cut cycle any time soon unless something bad happens.

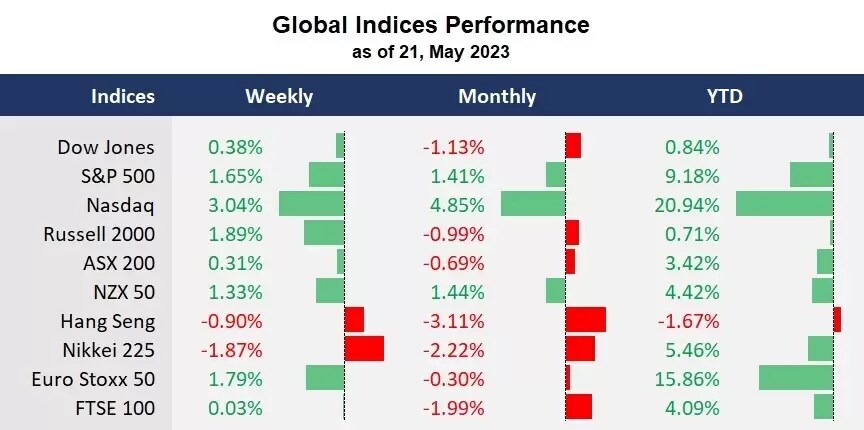

- Japanese stock markets hit record highs: The most notable market action is that the Japanese benchmark indices, such as Topix and Nikkei 225, hit record highs last week as foreign investment funds may be returning to the policy-supported country.

- Gold slides: A combination of factors has recently pressed on gold price: a strengthened US dollar, AI-powered risk-on sentiment, and the need for a technical correction. Gold lost shines in May, but this could be just a temporary retreat.

- Oil traders are indecisive: Crude oil went sideways in the last two weeks due to unclear signals in supply and demand. While risk-on heated up in tech shares, growth-sensitive commodities were pressed by the gloomy economic outlook. But the G-7 meeting could impose more sanctions on Russia’s export, which may provide a bullish factor in oil.

Australian markets

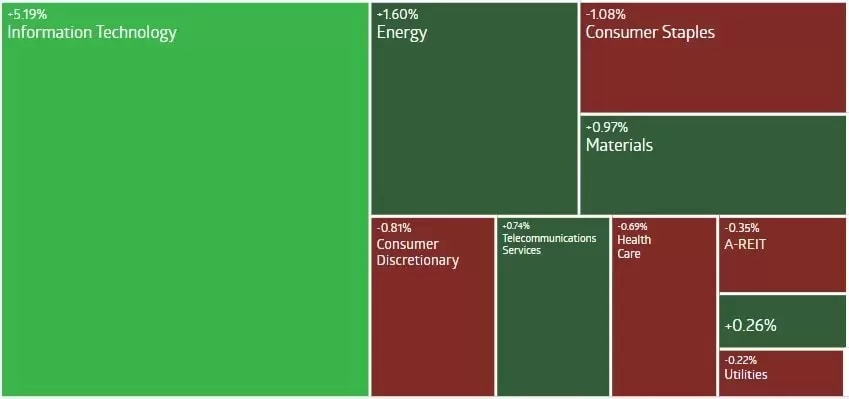

The ASX 200 finished slightly higher for the week, led by the information technology sector, up 5.19%, but most of the other sectors ended in the red, especially in the defensive sectors, such as consumer staples, health care, and utilities. The moves followed Wall Street, but the miner and bank-heavily weighted market underperformed its US peers this year due to a lack of tech components. The Australian dollar was also flat against the US dollar, continuing a range-bound movement between 0.6570 and 0.68 in the last few months due to sluggish price actions in resources and energy. The upcoming retail sales data will provide more clues to the economic trajectory.

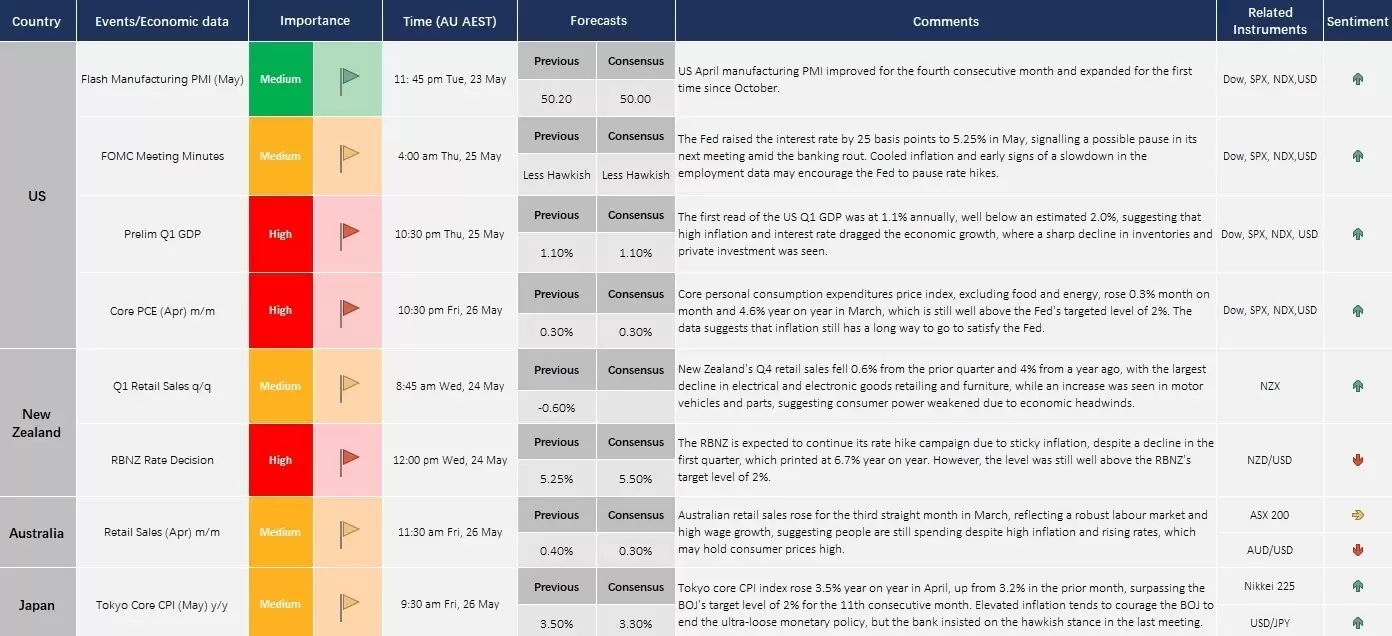

Economic Calendar (22 May – 26 May)