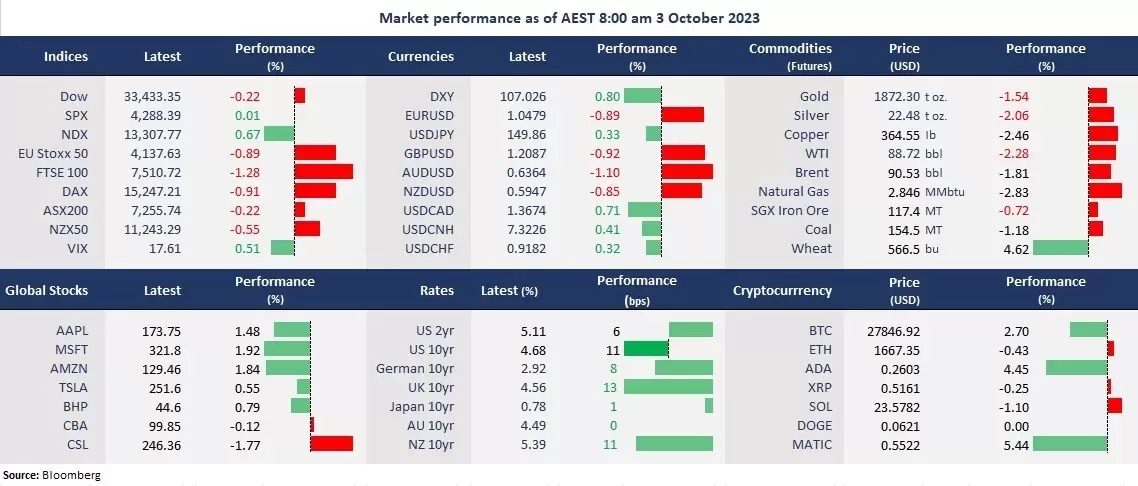

Wall Street erased the early gains and finished mixed as stock markets continued to suffer from soaring bond yields, despite the US averting a government shutdown. The 10-year US Treasury yield jumped 12 basis points, hitting the highest level since October 2007 following hawkish reiteration by the Fed officials at a roundtable discussion. Notably, the small-cap benchmark, Russel 2000, was badly impacted by the soaring bond yields, falling 1.58% to negative territory for the year. On the other hand, it seems that the big tech companies were seen as safety destinations to the jumping bond yields due to their healthier cash flow and better growth prospects. The AI frenzy has also helped the sector to hold up by directing funds into the sector. But it is worth noting that the fear gauge, the VIX, remained at a recent high of 17.61, suggesting risk aversion was still the prevailing market trend.

In FX, the US dollar index extended the eleventh straight weekly gain to above 107, the highest since November 2023, sinking all the other G-10 currencies as well as commodity prices. Gold futures plunged to the lowest since early March, and crude oil prices pulled back to under US$90 per barrel.

In Asia, China’s September manufacturing PMI expanded for the first time since March, which may lift its stock markets on the return from holiday. The RBA’s rate decision will be closed watched today when the bank is expected to hold the OCR for the fifth consecutive time. Futures point to a mixed open across the APAC. The Nikkei 225 futures fell 0.46%, and the ASX 200 futures slumped 1.36%, and Hang Seng Index futures were up 0.02%.

Price movers:

- 8 out of 11 sectors in the S&P 500 finished lower, with Utilities and Energy, leading losses, down 4.72% and 1.33%, respectively. The three growth sectors, including Consumer Discretionary, Technology, and Communication Services, outperformed as mega-cap tech companies were mostly higher.

- Utility stocks were hurt the most, down 4.7% by the rampant bond yields, as these companies usually have high debt levels and are more vulnerable to rising interest rates. The sector is down 20% year-to-date to a three-year low. The renewable energy asset owner NextEra Energy Partners’ shares slumped 9% following a downgrade last week.

- Tesla’s shares were steady, despite a disappointing electric car delivery number in the third quarter. The EV maker delivered 435,059 electric vehicles, lower than an estimated 461,640 by Wall Street, and was down from 466,140 in the previous quarter. But the number still represents a 26.5% increase from the same period last year. According to the company’s statement: “A sequential decline in volumes was caused by planned downtimes for factory upgrades, as discussed on the most recent earnings call,” and the 2023 target volume remains at 1.8 million cars.

- Gold futures were slashed further by the rising bond yields and a nearly one-year high USD The precious metal may continue the downtrend, heading off potential support of around 1,800.

- Crude oil extended a three-day losing streak to under 90 amid risk-off trade, ahead of the OPEC meeting. A strong US dollar and the jumping US bond yields pressed on oil markets, while OPEC+ is expected to maintain production. Oil may have been overbought in the past two months, and a technical correction may also have been the cause of the drop.

- Bitcoin briefly popped above 28,000. Cryptocurrencies may have initially been boosted by optimism as the US avoided a government shutdown temporarily. However, the rampant bond yields pressured risk assets and caused Bitcoin to retreat from the intraday high of 28,500.

ASX and NZX announcements/news:

- No major announcement.

Today’s agenda:

- Australia’s building approvals for August

- RBA Rate Decision

Maximize your potential gains! Take immediate action and seize the investment opportunities that await you. Login to the platform now!