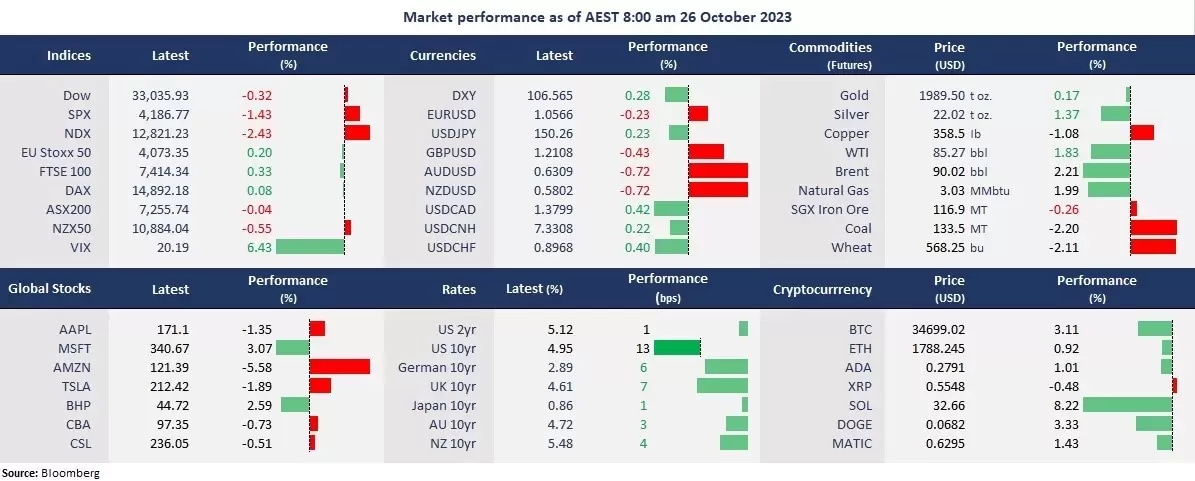

Wall Street slumped, with Nasdaq down more than 2% as risk-off again dominated the broad market’s movements, pressuring equities, particularly in growth stocks. The US bond yields spiked, lifting the US dollar, and sending commodity currencies down in particular. Gold, crude oil, and Bitcoin continued to rise as being seen as haven assets that hold value in uncertain times amid the Hamas-Israel war.

On the earnings front, Alphabet plummeted nearly 10%, the worst single-day performance since March 2020. Its Google Cloud revenue missed expectations. Microsoft was the only mega-cap company that finished higher due to an earning beat. Meta Platforms’ shares rose 2% in the after-hours trading after reporting the third-quarter earnings, topping both top and bottom lines, with revenue up 23%. Amazon is set to report earnings after the US markets close tomorrow.

Asian markets are set to open mixed. ASX 200 futures were down 0.37%, Hang Seng Index futures were up 0.34%, and Nikkei 200 futures fell 1.02%.

Price movers:

- 9 out of 11 sectors in the S&P 500 finished lower, with Communication Services, leading losses, down 5.89%. Defensive sectors, including Consumer Staples and Utilities, outperformed, up 0.33% and 0.48%, respectively.

- Meta Platforms’ shares rose nearly 3% following stronger-than-expected earnings results. The social media giant’s overall revenue jumped 23% year on year and expected the revenue for the fourth quarter to be between US$36.5 billion and US$40 billion.

- Gold futures were up US$5 dollar per ounce amid risk-off sentiment. A breakout of this level may take the precious metal to hit an all-time high of 2,080 again.

- WTI futures rebounded to test the 50-day moving average of about 85 on war-intensified geopolitical tensions. The US crude inventory increased by 1.4 million barrels by the week ending 20 October 2023, higher than an forecast of 0.5 million draw.

- Bitcoin topped 35,000 briefly before pulling back to about 34,600. However, the digital currency may have been overbought from a technical perspective. The potential near-term support can be found around 31,600.

Today’s agenda:

- ECB Rate Decision

- US Q3 GDP

Disclaimer: CMC Markets is an execution-only service provider. The material (whether or not it states any opinions) is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.