Wall Street was mixed last week as company earnings painted a mixed picture. Dow rose for the tenth consecutive trading day on Friday, the longest winning streak in nearly six years, while Nasdaq lost steam amid disappointing earnings from Netflix and Tesla as the challenging macro environment continued to bite their profits. At a sector level, three growth sectors, including consumer discretionary, communication services, and technology, were the laggards in the S&P 500 last week. At the same time, Energy, Healthcare, and Utilities were the top performers, suggesting funds may start rotating to cyclical and defensive stocks from tech-heavy sectors.

It will be a big week for the US markets, with the Fed to decide on the interest rates again. The reserve bank is widely expected to raise the rate by 25 basis points for the last time before ending the hiking cycle. In addition, the US second quarter GDP is also due for release this week, gauging the country’s economic health. On the earnings front, the tech giants, including Microsoft, Meta, and Alphabet, will report their earnings. Whether the AI heat can continue to push these stocks higher can be critical for broad sentiment.

Elsewhere, the Bank of Japan (BOJ) and the European Central Bank (ECB) will also hold the policy meeting. Despite mounting inflationary pressure, the BOJ is expected to keep the ultra-loose monetary policy to support economic growth. And the ECB may raise the interest rate by another 25 basis points.

At last, Australia’s second-quarter CPI will also be eyed as it will provide clues for the RBA’s policy path.

What are we watching?

- US regains ground: The US dollar index rebounded above 100 as the US bond yields climbed. However, the dollar may continue to decline if the Fed signalled the end of its hiking cycle this week. Conversely, a hawkish Fed could lift bond yields and bring the USD higher.

- Tech stocks lose steam: Most big tech stocks finished lower for the week following Netflix and Tesla’s earnings reports as investors may continue rebalancing their positions with earnings season rolling on.

- Crude oil extends gains: Oil prices post third straight weekly gain due to improved demand outlooks, while recession fear recedes following the recent resilient US economic data. According to the IEF, China and India’s demands may ramp up in the second half of the year.

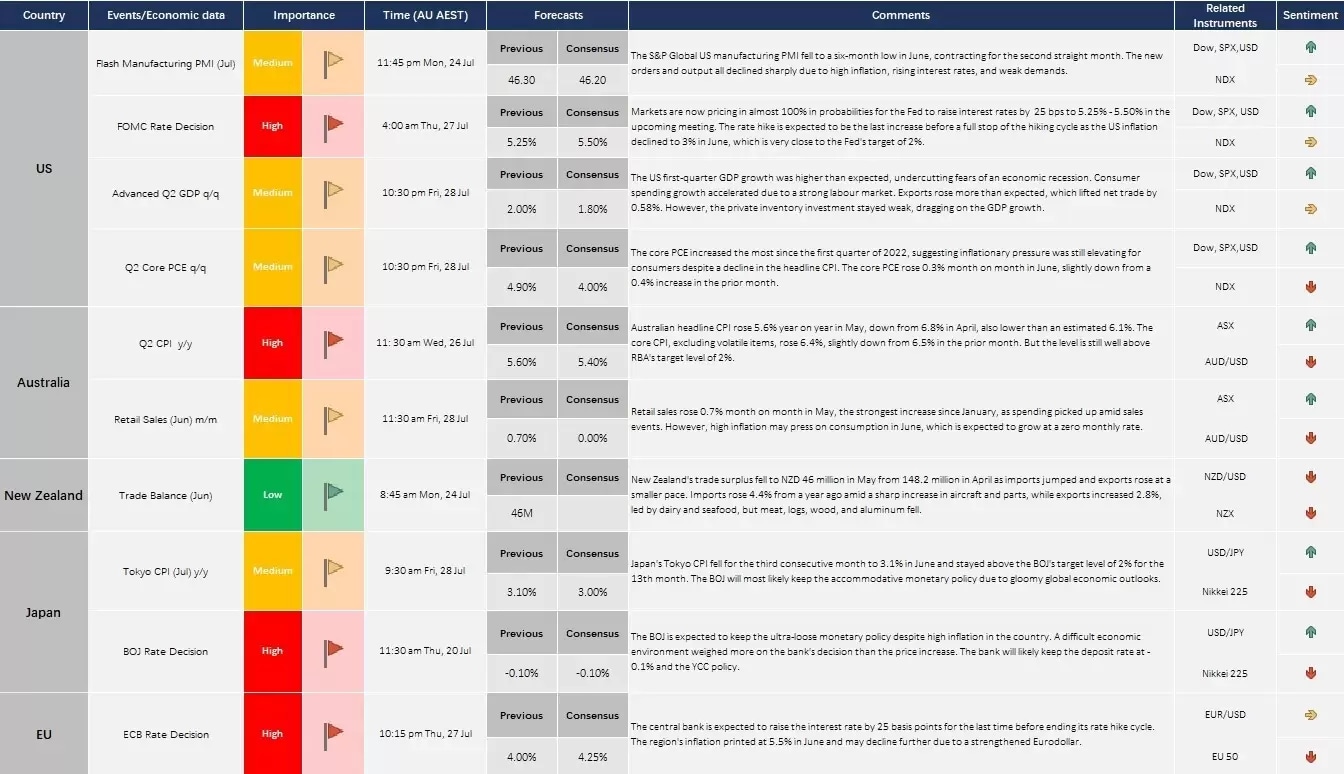

Economic Calendar (24 July – 28 July)

Disclaimer: CMC Markets is an execution-only service provider. The material (whether or not it states any opinions) is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.