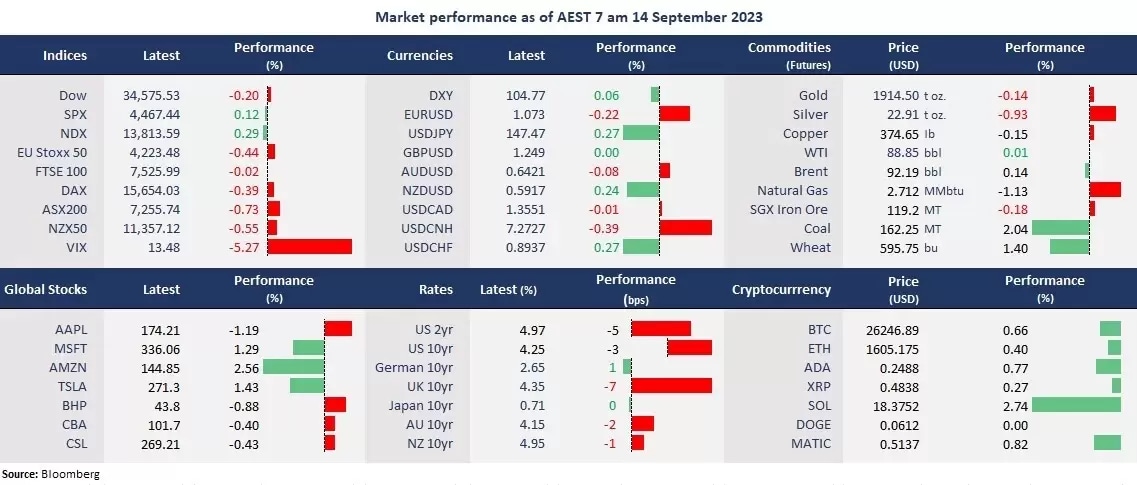

US stocks finished mixed, with the Dow in the red, while the S&P 500 and Nasdaq were higher following the slightly higher-than-expected August CPI data. The US headline inflation rose 3.7% from a year ago and 0.6% from last month, higher than the estimated 3.6% and 0.6%, respectively. The Core CPI excluding food and energy, was up 4.3% annually and 0.3% monthly, compared with expected 4.3% and 0.2%. The data may nail another rate hike by the Fed in November after a possible pause in September. Stock markets were relatively calm as inflation was mostly in line with expectations, and the US government bond yields fell slightly following the data.

The tech stocks were the winners again, while the energy sector lost steam. The UK-based, SoftBank-owned software company ARM is set to debut when the US markets open tonight, which will be the biggest IPO of the year. Investors will be awaiting more influential economic data from the US tonight, including the Producer Price Index, retail sales, and unemployment claims. The European Central Bank will also decide on its policy rate later today when a pause is widely expected.

Asian markets were mostly lower on Wednesday but are set to open higher. The Australian employment data will be in focus in the Asian session, with an expectation that the labour market remains robust to support more rate hikes by the RBA. The Nikkei 225 futures are up 0.53%, the ASX 200 futures are down 0.06%, and the Hang Seng Index futures rose 0.02%.

Price movers:

- 6 out of 11 sectors finished higher in the S&P 500, with Utilities and Consumer Discretionary leading gains, up 1.2% and 0.9%, respectively. Real Estate was the biggest laggard, down 1.03%, due to strengthened rate hike expectations by the Fed. Energy stocks also underperformed, sliding 0.76% on the sector rotation.

- Arm prices IPO at US$51 per share, higher than an expected price range of between US$47 and US$51, which makes its market valuation about US$55.5 billion. The debut is set to be the largest technology IPO on the US markets this year, joining the AI race globally to direct investment funds.

- Apple’s shares fell for the second straight trading day as China expanded a ban on iPhones in state-owned departments and companies. China is the largest market for Apple, accounting for more than 20% of its market shares. The restriction will potentially reduce iPhone’s market share significantly.

- Google plans to cut hundreds of jobs more in the next few quarters on a recruiting action. Staff involved in the headcount cuts will receive emails starting Wednesday. Google cut 12,000 jobs, or 6% of its workforce, in January.

- Bitcoin consolidated above 26,000 for the second straight day, the highest since 31 August. The rebound may have been caused by short covering after a broad selloff in cryptocurrencies amid fears of FTX liquidation on Monday.

ASX and NZX announcements/news:

- No major announcement.

Today’s agenda:

- Australian MI Inflation Expectations for August

- Employment Change for August

- ECB Rate Decision

- US PPI for August

Maximize your potential gains! Take immediate action and seize the investment opportunities that await you. Login to the platform now!

Disclaimer: CMC Markets is an order execution-only service. The material (whether or not it states any opinions) is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.