Global markets all finished in the green last week on peak rate bets after both the US Fed and the Bank of England halted rate hikes for the second consecutive time. The war-intensified geopolitical tensions also added to central banks’ consideration of economic risks. Wall Street experienced a sharp relief rally on Friday night as risk-off abated following weaker-than-expected non-farm payroll data. Dip-buys were particularly seen in technology stocks, given they were the hardest beaten sector in the past three months. Nasdaq jumped about 6.6% for the week.

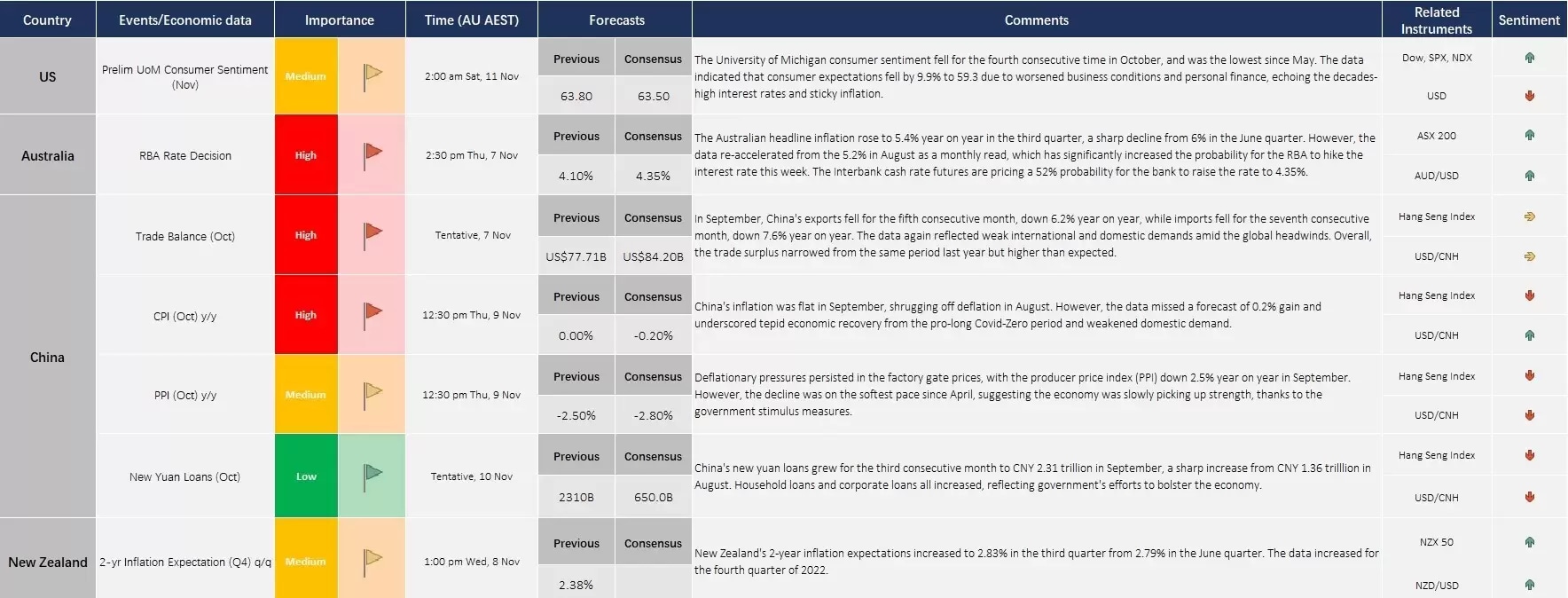

This week, the Reserve Bank of Australia’s rate decision is a focus in Asia, particularly impacting the Australian dollar and the ASX movement. Markets were pricing in more than 50% probability for the bank to raise the interest rate by 25 basis points to 4.35%. This is due to an escalation in September inflation. However, the global impact can also be a factor weighing on its decision.

In addition, China will be a key focus as the country will release a slew of economic data that potentially impacts global markets. We focus on China’s CPI, PPI, trade balance, and new yuan loans to gauge its economic trajectory. China has been experiencing a tepid economic recovery from its pro-longed Covid-Zero curbs. And the property woes became a major issue that could have rippling effects on the global markets.

What are we watching?

- VIX falls: The fear gauge of investment sentiment, the CBOE volatility index, sharply pulled back to just under 15 from above 22 last week. It usually indicates the global risk-on returns, which signalls potential bottoming reversal opportunities in risk assets, such as equities, industrial metal prices, and commodity currencies.

- US dollar retreats: The US dollar index posted the deepest weekly drop since the first week of July, as Friday’s US job data strongly reduced the impetus for the Fed to continue raising the interest rates.

- Mega-cap techs rebound: The mega-cap US tech stocks experienced a sharp rebound amid risk-on sentiment. Nvidia’s shares surged 11% in the last week, suggesting the AI frenzy returned.

- Gold eases: The precious metal finished lower for the week as haven demands weakened. However, a softened US dollar and the retreat in bond yields may continue to shape the uptrend.

Economic Calendar (6 Nov – 11 Nov )

Disclaimer: CMC Markets is an order execution-only service. The material (whether or not it states any opinions) is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.