US stocks finished broadly higher following Arm IPO as the UK-based chip designer’s stocks soared more than 24% on its debut day, which makes its market valuation at about US$60 billion. Arm’s owner, SoftBank’s wealth swelled by about US$12 billion overnight. The debut is the biggest offering of the year so far, and its success may revive the drought IPO market if Arm’s shares sustain the upside momentum. Arm’s major investors, such as Apple, Alphabet, and Nivida, all finished higher on Thursday.

On the economic front, the US August Producer Price Index rose 0.7% month on month, higher than the expected 0.4% due to a jump in energy prices since July. The data shows that inflation has come back to town following higher-than-expected CPI on Wednesday. Jobless claims dropped to the lowest level since February last week, suggesting labour markets stayed robust, further strengthening the odds for higher for longer interest rates.

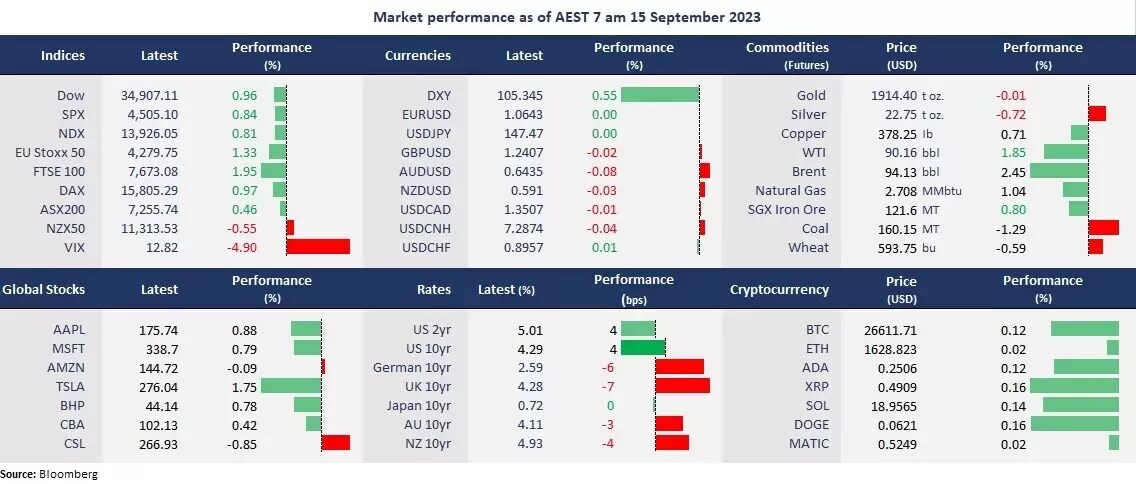

The US government bond yields climbed, with the 2-year Treasury yield rising 3 basis points to 5.01%, boosting the US dollar index to above 105, the highest level seen in March. A slump in the Eurodollar following the ECB’s rate hike also added to the strength of the king dollar as major European countries’ government bond yields fell sharply.

The Arm IPO optimism and China’s further stimulus measures boosted sentiment across Asian stock markets. The PBOC cut the Reserve Requirement Ratio for most banks by 25 basis points, with the weighted average RRR dropping to 7.4%, lifting commodity prices, with the WTI futures rising to above US$90 per barrel for the first time since November 2022. Asian markets are set to open higher, the Nikkei 225 futures are up 0.79%, the ASX 200 futures rose 1.28%, and the Hang Seng Index futures climbed 0.51%.

Price movers:

- All 11 sectors finished higher in the S&P 500, with Real Estate and Utilities leading gains, up 1.71% and 1.47%, respectively. Healthcare was the laggard, up 0.2%. Notably, the Energy sector index (XLE) rose to the highest level since November 2022 due to spiking crude oil prices.

- Adobe’s shares fell 1.8% in after-hours trading amid quarterly earnings report, despite a beat on expectations. The photo editing software company’s earnings per share were US$4.09 on revenue of US$4.89 billion, topping estimates of US$3.98 and US$4.87 billion. Adobe also integrated AI functionality into its products to appeal users.

- The Eurodollar slumped, and the European stock markets finished amid the ECB’s rate hike. The bank unexpectedly raised the main deposit rate by 25 basis points to 4%. Markets see no more rate hikes afterward, though ECB President Christine Lagarde did not see a peak just yet.

- Crude oil prices jumped amid China’s stimulus measures, boosting sentiment in the commodity markets. While China’s economic rebound remains hopes for market bulls, IEA forecasted fossil fuel demand may peak before 2030. But the oil producer cartel OPEC coitized it as an “ideologically driven” comment.

ASX and NZX announcements/news:

- No major announcement.

Today’s agenda:

- China’s Industrial Production, Retail Sales, Fixed Asset Investment, Unemployment Rate for August.

- US Empire State Manufacturing Index & Prelim UoM Consumer Sentiment for September

Maximize your potential gains! Take immediate action and seize the investment opportunities that await you. Login to the platform now!

Disclaimer: CMC Markets is an order execution-only service. The material (whether or not it states any opinions) is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.