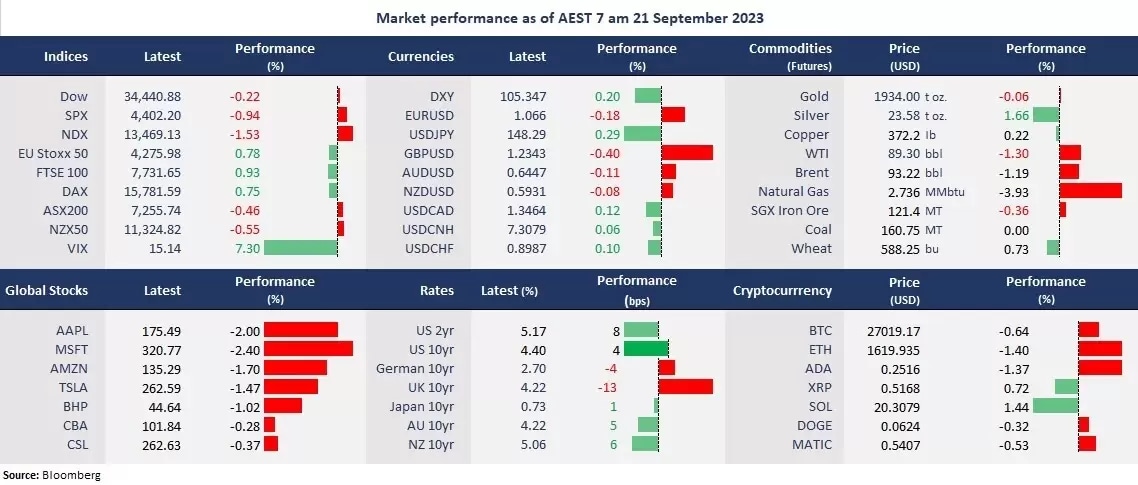

The US stock markets continued to slip after the Fed held the interest rate at 5.50% unchanged but signalled one more increase and brought the fund rate to 5.6% this year. The Fed’s rhetoric was more hawkish than expected as Chair Powell sees the neutral rate to be higher than previously projected. Fed officials forecasted the US economy to be stronger, growing 2.1% this year, up from 1.0% in June’s projection. Tech stocks led to broad losses as higher for longer rates expectations pressed on market valuations, while the Fed rate-sensitive 2-year bond yields rose to the highest level since 2006, lifting the US dollar. The SNB and BOE’s rate decisions tonight and the BOJ’s policy meeting tomorrow will be closely watched by investors.

Risk-off again prevailed in the broad markets, with the fear gauge, the VIX, jumping 7% to a nearly one-month high of 15.14. Gold futures grappled above the 50-day moving average of 1,950.

The IPO stocks were also hit by the broad selloffs, with Arm’s sharing falling for the fourth straight trading day to US$52.80. Instacart’s shares slid to just above the IPO price of $30. Klaviyo’s shares jumped 22% from the IPO price of US$30 at the open but pulled back to finish at $32.

Asian markets are set to open lower following Wall Street’s slump. New Zealand’s second-quarter GDP will be the focus of the regional markets. The Nikkei 225 futures fell 0.66%, the ASX 200 futures slid 0.46%, and the Hang Seng Index futures were down 0.62%.

Price movers:

- 7 out of 11 sectors in the S&P 500 finished lower, with Communication Services and Technology leading losses, down 1.89% and 1.77%, respectively. Defensive sectors, such as Consumer Staples, Healthcare, and Utilities, finished higher as investors sought for safety.

- FedEx’s shares jumped 5% amid a beat on market expectations due to effective cost cuts. The package delivery company reported earnings per share as US$4.55, topping an estimated US$3.7. The revenue came to US$21.68 billion, missing the expected US$21. 84 billion. FedEx upgraded its earnings per diluted share expectations to between US$17.00 and US$18.50 from between US$16.50 and US$18.50 for fiscal year 2024.

- GBP/USD fell to a four-month low of nearly 1.2350 following lighter-than-expected UK’s August CPI. The country’s inflation declined to 6.7% year on year from 6.8% the prior month, much lower than an expected 7.0%. The data sent the UK 10-year government bond yield down 13 basis points to 4.22%, compared with the US peers of 4.41%. But it may not change the expectation for a 25 basis point rate hike by the BOE tonight.

- The NYM WTI futures fell to under $90 per barrel following the Fed’s rate decision. Risk-off sentiment and a firmed US dollar are key factors pressing on commodity markets. Crude oil markets may have been overbought, and a technical correction can also be the reason for the price drop. The near-term potential key support could be at the 50-day moving average of 82.77.

ASX and NZX announcements/news:

- Fonterra (ASX: FSF, NZX: FCG) lowered its farm gate price for milk solid to between NZ$6.00 and NZ$7.50 per kilogram for 2024 from NZ$8.22 per kilogram in 2023 due to weakened demands. The full-year revenue rose 11% to NZ$26 billion, and the profit jumped 170% to NZ$1.6 billion. The company unveiled a dividend of NZ50 cents per share.

- New Zealand King Salmon Investment (ASX/NZX: NZK) reported a net profit of NZ$10.6 million in the first half of fiscal year 2024, up from a loss of NZ$24.5 million during the same period last year. Revenue increased from NZ$80.0 million in the first half of 2023 to NZ$91.6 million in the first half of 2024.

Today’s agenda:

- New Zealand second-quarter GDP

- SNB Rate Decision

- BOE Rate Decision

Maximize your potential gains! Take immediate action and seize the investment opportunities that await you. Login to the platform now!

Disclaimer: CMC Markets is an order execution-only service. The material (whether or not it states any opinions) is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.