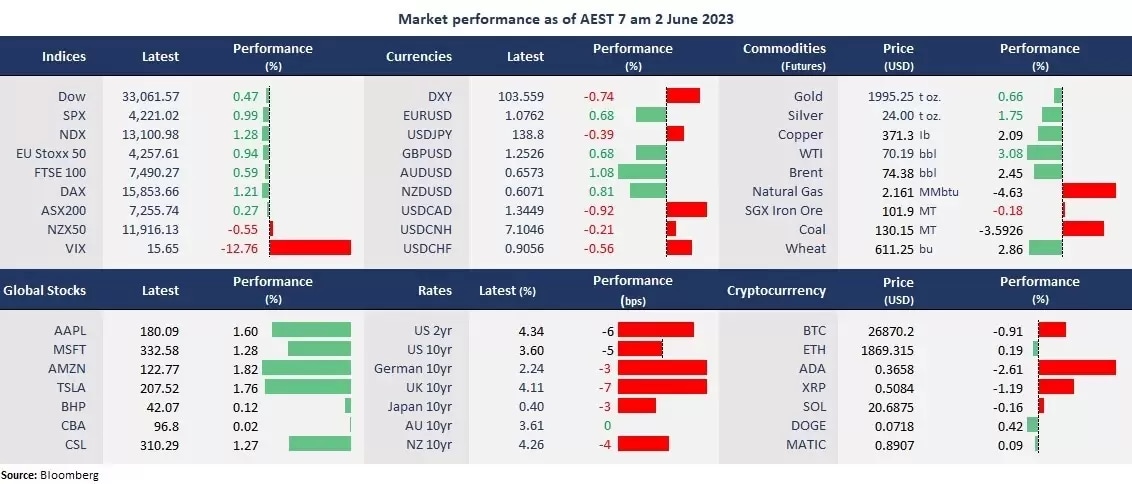

Wall Street finished higher on a broad-based rally as rates slid for the third straight trading day amid positive progress on the US debt deal progress, while Fed officials signalled a rate hike pause in the June meeting. The tech rally returned, with all the mega-cap companies’ shares up between 1-5% and Nasdaq jumped 1.3%, closing at the highest level since April 2022. The US non-farm payroll will be in the spotlight tonight when markets expect a slowdown in hiring.

On the economic front, the US ISM manufacturing PMI for May contracted for the seventh consecutive month, and is also the longest contraction stretch since Great Recession. The factory gate price index decreased to 44.2, the lowest since January, suggesting inflation may extend its decline. The data pressed on the US dollar and sent all the other major currencies higher, lifting commodity prices, particularly crude prices. WTI futures reversed losses from a day earlier and finished above US$70 per barrel ahead of a key OPEC+ meeting at the weekend, as the recent steep slump in oil prices may lead the cartel to cut output further.

In Asia, the US-listed Chinese tech shares sharply rebounded, with Alibaba up 4.3% and Baidu up 6.5%. Futures point to a higher open across the APAC, with ASX 200 futures up 0.63%, the Hang Seng Index futures up 1.8%, and Nikkei 225 advancing 0.80%.

Price movers:

- 9 out of 11 sectors in the S&P 500 finished higher, with technology leading gains, up 1.33%. Consumer staples and utilities are the only two sectors that ended in the red, suggesting that funds again flew into riskier sectors, typically in the growth stocks.

- Lululemon’s shares soared 13% amid a beat on the first quarter’s earnings expectations and positive outlooks. The retailer reported earnings per share at US$2.28, higher than an expected US$1.98. The revenue was US$2 billion, up 24% from a year ago, topping a US$1.93 billion estimated. The company upgraded the full-year revenue guidance to between US$9.44 billion and US$9.51 billion from between US$9.31 billion and US$9.41 billion.

- Apple is expected to announce its first mixed-reality headset at the software-focused developer conference on Monday. The announcement may mark a development of a new series of major product lines concentrating on AR/VR technology. The new product is to compete with Meta’s Quest series VR headsets and Microsoft’s HoloLens.

- Microsoft agreed to invest billions of dollars in cloud computing infrastructure from CoreWeave, a startup that sells simplified access to Nvidia’s GPUs, according to CNBC. The company’s shares rose 1.3% on Thursday.

- Tesla CEO Elon was encouraged by Chinese officials to boost investment in Shanghai during his trip to China. The statement also said Tesla hoped to strengthen collaboration with Shanghai and better serve both the Chinese and global markets, according to Bloomberg.

- Crude oil swung back on traders’ bets for a further production cut by OPEC+. The organization announced a voluntary cut of 1.15 million bpd in April, on top of a 2 million bps reduction from November last year to stabilize oil markets. as

- Gold rose for the third straight trading day as the USD slid further and bond yields fell. The metal’s price faces potential resistance of the 50-day moving average in the near term. A breakout of this level may take it to head off an all-time high of above 2,070 again.

ASX and NZX announcements/news:

- No major announcement.

Today’s agenda:

- US non-farm payroll for May.

Disclaimer: CMC Markets is an order execution-only service. The material (whether or not it states any opinions) is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.