There is no doubt anymore that the US equity markets are now falling into a bear market, with the S&P 500 briefly declining beyond the 20%-mark year to date last Friday. Let us hope the “bad news” can make some “good news” as people’s wealth in their stockpiles has shrunk in such a scary manner, which will be translated into weakening demands and help cool down inflation, thanks to the speeding up rate hikes, plunging risk asset prices, and no-solution in the war-induced supply chain disruptions. The Fed’s policy approach may start taking effect, which is to fight inflation at a cost of slowing growth, or worse, an economic recession.

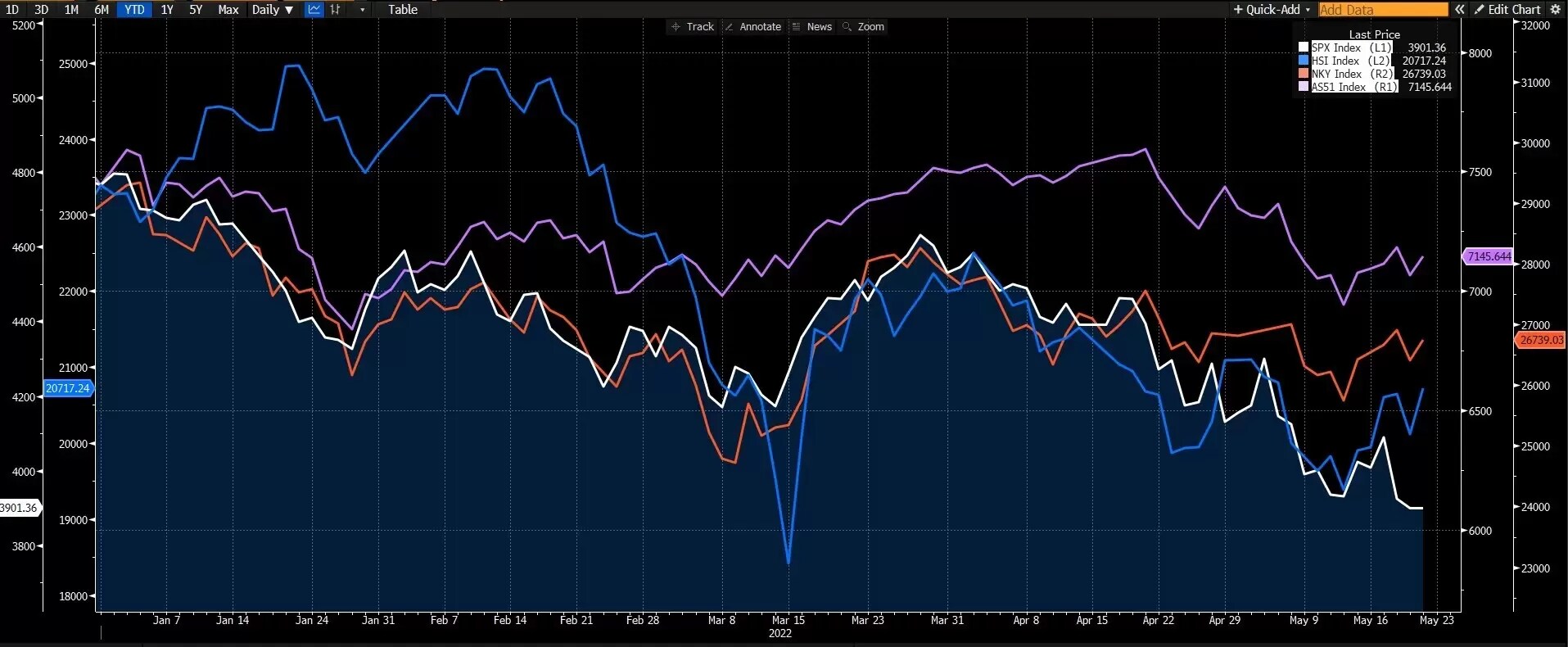

Despite the US stock rout, broad Asian equity markets are more resilient. Notably, Australian equities outperformed all the other major stock markets, with a 7% drop year to date (See the below chart), amid strong commodity prices. With the labor party winning the election, it will be ingesting to see how the stock markets will react on Monday. At the same time, the Chinese stocks took a ride of the policy tailwind last Friday, with CSI 300 jumping 2% after the PBOC cut the 5-year loan prime rate (LPR) by 15 basis points, the biggest reduction since the mechanism revamping in 2019.

Key Points

- Are there any rebounding opportunities in the US stocks after the S&P 500 briefly fell into a bear market? Can the tech-heavy index, Nasdaq, start establishing some upside momentum after falling 23% from its April high?

- Will Chinese equity markets take off at the back of easing Covid-lockdowns, coupled with the government’s dedicated stimulus measures?

- Did we see a near-term top of USD/JPY since US bond yields rapidly retreated from May highs? The US dollar index’s weakness starts creeping in after hitting a fresh 20-year high.

- In addition, the falling bond yields and softening USD may have helped gold to establish a bottom reversal opportunity, with a bullish break-out at the descending trendline. See the latest markets movements

Key economic data and events

US GDP, good orders, PCE, and FOMC meeting minutes

A slew of upcoming US data will be the key gauges to see if Fed’s front-loading rate hikes start pressing the economic growth. The US April PCE data is a focus, should it indicate an ongoing high cost of living, which may lead to deterioration in risk sentiment. The second read of the US first-quarter GDP will be released on Thursday, which will provide further evidence if the macroeconomic landscape has worsened after the first release of negative growth of 1.4%. In addition, the US flash manufacturing and services PMIs of May will provide projections of the current month's economic activities on Wednesday. The FOMC meeting minutes is certainly a spotlight to find more clues about the Fed’s policy roadmap, in which a 50-basis points rate hike has been priced in for each of its next two meetings.

RBNZ policy meeting

The Reserve Bank of New Zealand is expected to raise the Official Cash Rate (OCR) by 50 basis points, to 2% next week to curb 30-year high inflation, which printed at 6.9% in the first quarter. The Reserve bank expects more 50 bps rate hikes to come for each of the meetings for the rest of the year. As New Zealand Treasury has forecasted a dampened economic outlook from the second half of the year, any toning down in rate hike of the RBNZ may crash the local currency again.

Australia flash PMIs, retail sales, construction output, and capital expenditure

Australia has reported another strong employment data last week, coupled with better-than-expected wage growth. The strong economic data may promote more aggressive moves by the RBA, making a bullish factor to both local currency and equity markets. The upcoming Australian economic data, including the flash manufacturing and service PMIs in May, construction output, and private capital expenditure for the first quarter, will offer more clues about the economic health, with expectations that the first quarter business spending may have strongly recovered from the omicron disruptions.

Europe Week Ahead

Marks & Spencer full-year results - Wednesday

Germany, France flash PMIs (May) - Tuesday

Disclaimer: CMC Markets is an order execution-only service. The material (whether or not it states any opinions) is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.

{kind=link}