It’s a busy week ahead for the financial world, with four major central banks holding policy meetings before the year-end. Wall Street’s rally has taken a breather last week as investors become cautious ahead of the US CPI and the last FOMC meeting before Christmas. Friday’s stronger-than-expected US PPI data flashed an alert that the upcoming inflation data may not be as positive as hoped. And the deeply inverted US bond yields keep signalling an economic recession ahead. While China’s reopening optimism still offers a bullish factor to risk assets, the inflation data from the US will have a major impact on the market’s trajectory for the rest of the year.

What are we watching?

- The US dollar pauses declining: The US dollar index finished flat last week, ending a two-week losing streak ahead of the key inflation data, while the US bond yields also paused a four-week decline, finishing higher for the week.

- Gold tests key resistance: Gold hovers around the near-term technical resistance of 1,800 at the 200-day moving average and finished flat for the week as the precious metal negatively correlated with the US dollar and bond yields this year.

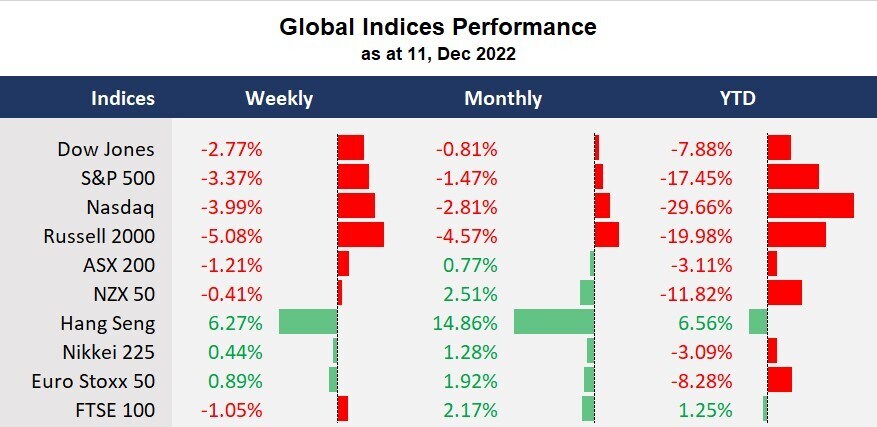

- Chinese stocks extend gains: The benchmark index for Chinese stocks, Hang Seng, gained for the fifth week in the last 6 weeks, amid Beijing’s rapid reopening progress and further stimulus measures. The optimism has also lifted commodity currencies and industrial metal prices, where both the Australian dollar and the New Zealand dollar are seen resilient moves against the US dollar.

- Crude oil on a decline: The oil markets were hit by recession fears in the last week as the demand look was downgraded amid weak Chinese economic data and concerns about the possible global recession. But from a technical perspective, oil prices may have an opportunity to bounce at their imminent support.

Economic Calendar (12 Dec – 16 Dec), all time is in Australian AEST

Disclaimer: CMC Markets is an order execution-only service. The material (whether or not it states any opinions) is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.