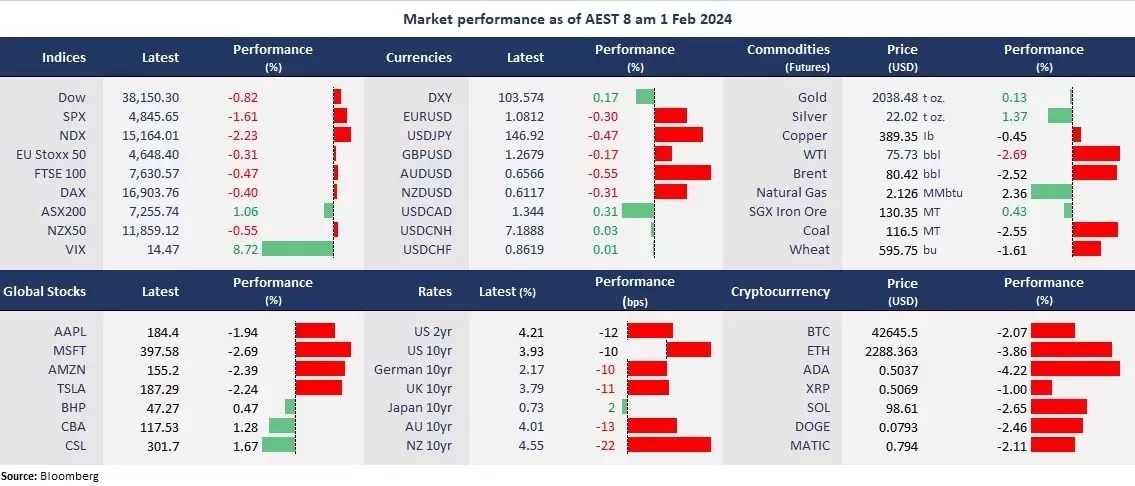

- Stocks retreated on tech wreck: Wall Street pulled back from their record high levels as tech shares fell sharply following Microsoft and Alphabet’s less-than-impressive earnings results. Alphabet tumbled more than 7% due to disappointing Google ad revenue, dragging the telecommunication sector down nearly 4%. Nonetheless, the three benchmark indices all finished higher at close to their respective record-high levels in January.

- Fed dims hopes for a March rate cut: As widely expected, the Fed kept the interest rate on hold for the third consecutive time at between 5.25% and 5.5% unchanged. However, Chairman Powell indicated that inflation was still too high, which makes it unlikely for the central bank to start cutting the interest rate in March. The relative hawkish stance further pressed the stock markets.

- Bond yields slid: The US Treasury yields fell following the Fed meeting as markets continued to price in rate cuts this year. The US 10-year bond yield fell below 4% for the first time in two weeks.

- US dollar strengthened: The dollar index moved higher due to the Fed’s more hawkish-than-expected rhetoric. The strong dollar also pressured commodity prices, including gold and crude oil.

- Crude oil fell: Oil prices fell after the US reported a much larger-than-forecasted inventory build overnight. The US commercial crude oil inventories increased by 1.2 million barrels by the week ending 26 January. In another report from Xeneta, the Red Sea-led shipping inflation might have reached a peak. But notably, both Brent and WTI futures finished the month higher for the first time in the past four months, thanks to the Red Sea riot.

- Bitcoin fell: Bitcoin finished lower, along with a drop in the US tech shares. Its upside momentum ran out of steam and finished flat in January after the SEC approved the spot ETFs. Profit taking might have been the cause after it hit a 9-month high of above 48,000 early in the month.

- Asian markets to open mixed: The Chinese stock markets continued its tepid movement amid the country’s economic turmoil. The merge of hundred rural banks is seen another measure for the government to avoid growing financial risks among small lenders. Despite the news, the Chinese stock markets are set to open higher, with the Hang Seng Index futures up 0.61%. However, other reginal stock markets are to fall following Wall Street’s pull back. ASX 200 futures fell 0.82%, and Nikkei 225 futures slid 1.12%.

Chart of the Day:

Nasdaq, daily – The tech-heavy index faced a technical resistance of around 17,600 at Fibonacci retracement of 112.80%. An overbought condition showing in the RSI may have caused the correction, with potential near-term support at near the 50-day moving average of between 16,600 and 16,700.

Company News:

- Qualcomm (NDX: QCOM) rose 2% amid an earnings beat, thanks to its handset chips sales, up 16% year on year. The semiconductor maker’s earnings per share came to US$2.75 on revenue of US$9.92 billion, largely topping estimates of US$2.37 and US$9.51 billion, respectively.

Today’s Agenda:

- Australian Building Approvals for January

- China’s Caixin Manufacturing PMI for January

- ECB President Lagarde Speaks

- Eurozone flash CPI

Disclaimer: CMC Markets is an order execution-only service. The material (whether or not it states any opinions) is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.