Spread bets and CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when spread betting and/or trading CFDs with this provider. You should consider whether you understand how spread bets, CFDs, OTC options or any of our other products work and whether you can afford to take the high risk of losing your money.

How we support our traders

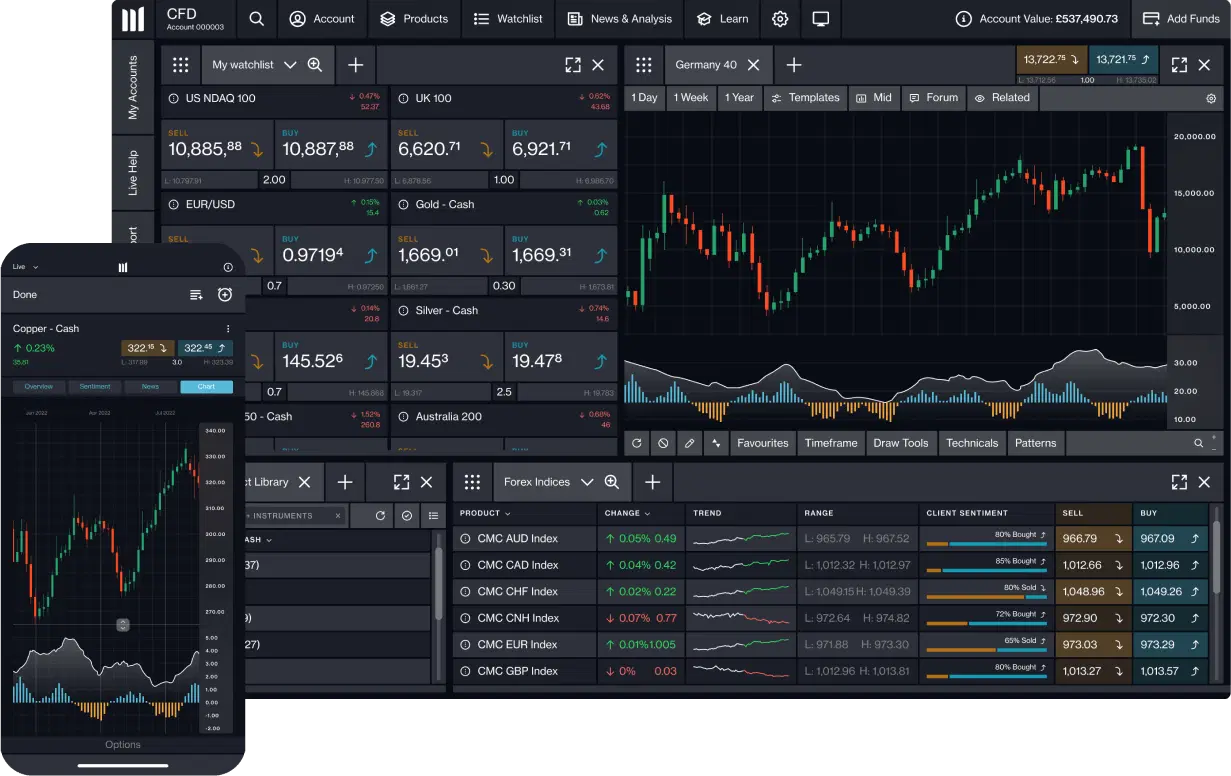

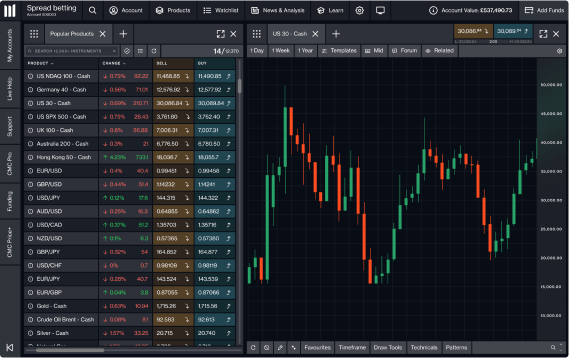

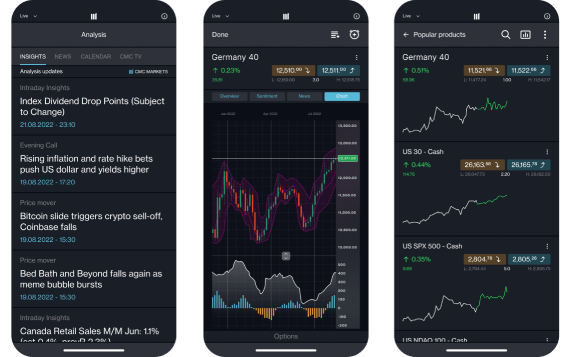

Our CFD trading platforms

Dive deeper

Spread Betting & CFD Trading

Ready to get started?

Open a demo account with £10,000 of virtual funds, or open a live account.

Any questions?

Email us atclientmanagement@cmcmarkets.co.uk

or call on +44 (0)20 7170 8200We're available whenever the markets are open, from Sunday night through to Friday night.

1 Recent awards include: Best Spread Betting Broker, Good Money Guide Awards 2026; No.1 Most Currency Pairs & Best-in-class for Overall Excellence, MetaTrader, Mobile Trading App, Professional Trading, Research & TradingView, ForexBrokers.com Awards 2026; Best Broker for Active Traders, Professional Trader Awards 2025; Best Mobile Trading Platform and Best Spread Betting & CFD Education Tools, ADVFN International Financial Awards 2025; No.1 for Commissions & Fees, ForexBrokers.com Awards 2025.

2 0.009 seconds spread bet and CFD median trade execution time on CMC Markets' web and mobile platforms, 1 April 2024-31 March 2025.

3FSCS is an independent body that offers protection to customers of financial services firms that have failed. The compensation amount may be up to £85,000 per eligible person, per firm. Eligibility conditions apply. Please contact the FSCS for more information.

4 Based on over 2 million unique user logins across CMC's trading and investing platforms, including partners, as at November 2025.

Loading...

Loading...