Spread bets and CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage.

68%

of retail investor accounts lose money when spread betting and/or trading CFDs with this provider.

You should consider whether you understand how spread bets, CFDs, OTC options or any of our other products work and whether you can afford to take the high risk of losing your money.

Ways to trade

Retail Trading

Equities trading

Spread betting

CFD trading

Options trading

Alpha

Price+

FX Active

Account comparison

Trading costs

Professional trading

CMC Pro

CMC Spectre

Institutional

Markets

Indices

Forex

Commodities

Shares

ETFs

Bonds

Share baskets

See all markets

Platforms

Web platform

CMC mobile app

MetaTrader 4

TradingView

See all platforms

Learn

Learn hub

News & analysis

About us

About us

Group

CMC careers

Support

Contact us

Log in

Start trading

Log in

Start trading

Market news & analysis

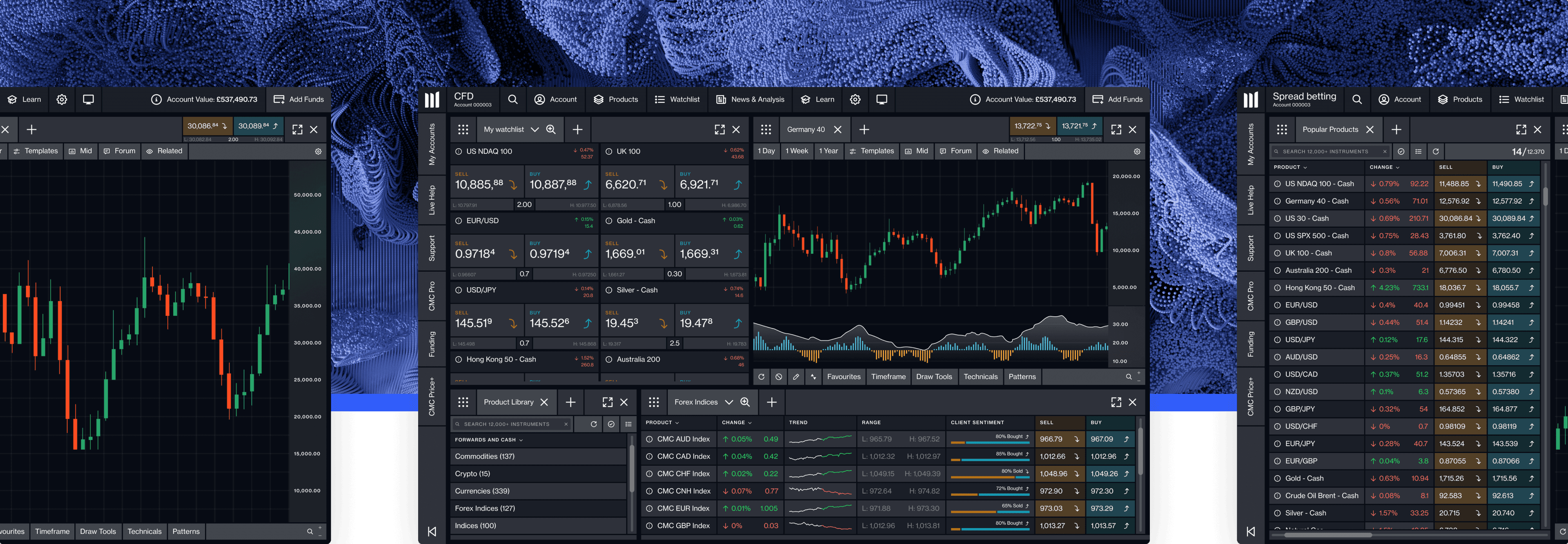

Spread Betting & CFD Trading

Ready to get started?

Open a demo account with

£10,000

of virtual funds, or open a live account.

Open a demo account

Create account

Loading...

Loading...