War pushes inflation, deficit and rates higher: CPI and 10-year note auction in focus

The war in Iran is affecting the interest rate curve and adding inflationary pressure through higher oil prices. Markets are now focused on the US Consumer Price Index (CPI) release, and the 10-year Treasury note auction as key indicators for interest rate expectations.

Market Analyst

US CPI (Wednesday 1:30pm): 2.4% could be a floor

On Wednesday at 1:30pm, the February 2026 US Consumer Price Index (CPI) will be released. Consensus forecasts expect inflation to match January’s levels, with headline CPI at 2.4% year-on-year and core CPI at 2.5%.

Although the disinflation trend has been positive in recent months, the recent rise in oil prices could reverse that progress. As a rule of thumb, a $10 increase in crude oil prices tends to raise CPI by around 0.2%.

PCE and CPI rising as rate cuts are delayed

The Cleveland Federal Reserve’s real-time inflation model, which incorporates daily petrol and crude oil prices, suggests CPI could rise to around 2.6% year-on-year in March.

Similarly, the model projects that the Personal Consumption Expenditures index (PCE), a key inflation gauge for the Federal Reserve (Fed), could increase by 0.2% to reach 2.8% year-on-year. The PCE data will be published on Friday at 1:30pm.

Higher inflation estimates have already affected Fed Funds futures markets. Traders now expect two additional rate cuts during this easing cycle, compared with three previously anticipated, and the timing of the next cut has shifted from June to July.

Rising risk premium and higher price expectations

Regardless of how the conflict in Iran evolves, whether the Strait of Hormuz reopens or strategic reserves are released, the underlying outlook appears to have shifted.

In its latest Short-Term Energy Outlook (STEO), the US Energy Information Administration (EIA) sharply revised its forecast for the average Brent crude price in 2026, raising it from $58 per barrel to $79 per barrel. The EIA expects Brent to remain above $95 per barrel over the next two months.

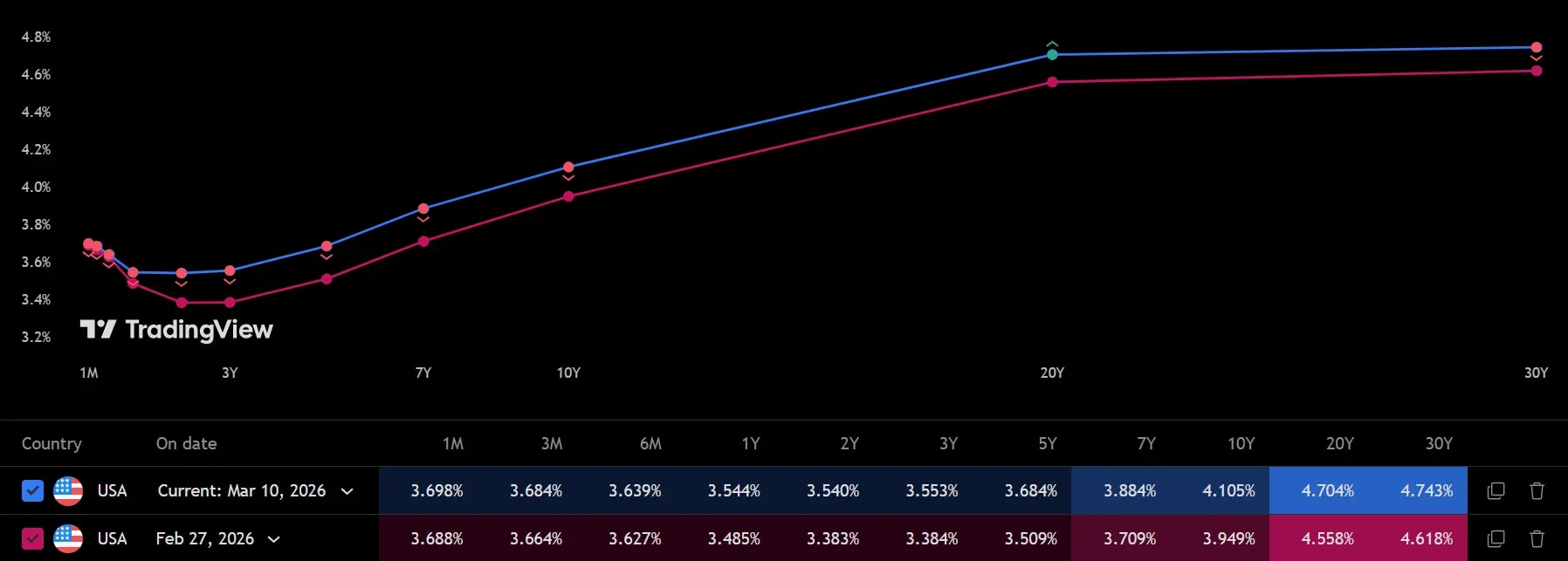

Risk premium also rising in government debt

Within the interest rate curve, the largest increase has been observed at the long end. Yields on 10-year Treasury notes have risen by 15 basis points since the start of the conflict.

The war could also worsen the already high US fiscal deficit. Kent Smetters, director of the Penn Wharton Budget Model, estimates that a two-month conflict could cost the United States between $40bn and $95bn, depending on the level of ammunition use and troop deployment.

Given these pressures, investors will be watching demand for US government debt closely. The US Treasury will auction 10-year notes on Wednesday and 30-year bonds on Thursday, both at 6pm.

Source: Interest rate curve movements since the start of the Iran conflict, from 27 February to 10 March 2026. Chart sourced from TradingView.

G7 weighs historic strategic oil reserve release

The G7 is considering an unprecedented release of strategic oil reserves as the risk of a prolonged Strait of Hormuz blockade intensifies. Markets are watching closely as volatility surges and key energy reports this week could shape expectations for prices and supply.