The Week Ahead: Nike earnings, ISM manufacturing, US jobs report

Welcome to Michael Kramer’s pick of the key market events to look out for in the week beginning Monday 29 June.

Founder, Mott Capital Management

Published: Friday, 26 June 2026 at 11.30pm (UK)

It will be a holiday-shortened trading week in the US, with markets closed on Friday 3 July, in observance of Independence Day. However, the week still features several key economic releases, including the US jobs report, UK GDP figures and Eurozone inflation data. Finally, on the earnings front, Nike will be the highlight of the week. A fresh earnings season is due to begin in mid-July.

Nike Q4 earnings

Tuesday 30 June

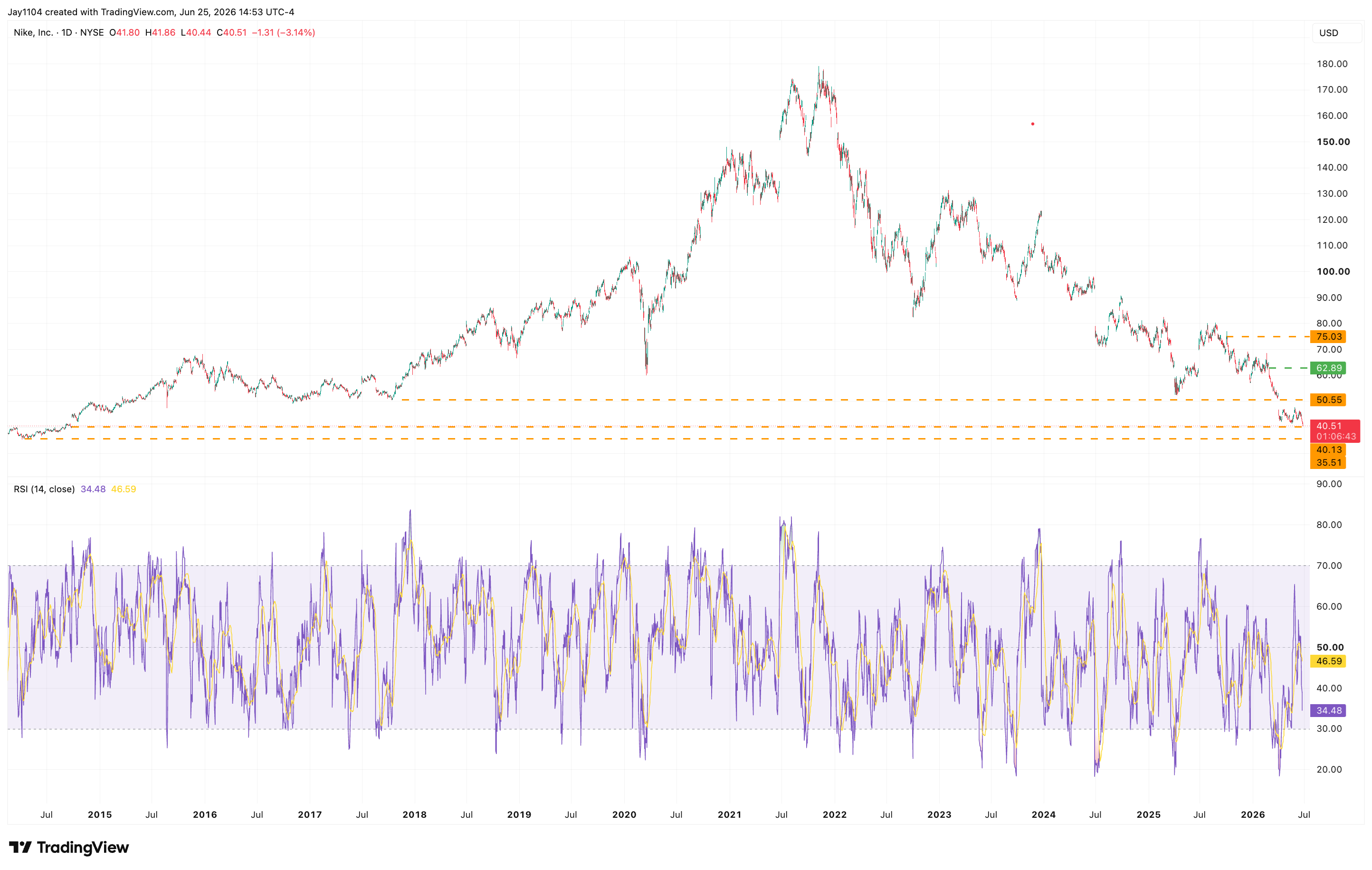

Analysts expect the New York Stock Exchange-listed athletic apparel manufacturer to report fiscal fourth-quarter 2026 earnings of $0.13 a share, a decline of 6% year-on-year. They also forecast revenue to fall 2% to $10.8bn, with gross margins contracting to 40%, down from 42% in the the previous quarter. The company is set to provide first-quarter fiscal 2027 guidance, with analysts expecting earnings to decline 6.8% to $0.46 a share and revenue to fall 1.7% to $11.5bn. However, they forecast gross profit margins to expand to 41.9%. The options market implies that Nike's share price – down roughly 35% this year at $40.90, as of Thursday's close – could move 7.9% in either direction after the results are released.

Nike shares have fallen sharply over the past year, and, unsurprisingly, options positioning is bearish. From an options gamma perspective, $40 is the key level of options support, while $50 is the primary resistance level.

Options markets are pricing implied volatility at around 80% for options expiring this week and it is likely to continue to climb as we approach the 30 June earnings report. Once the company reports results and implied volatility falls, hedging flows could become more positive. Despite the bearish options positioning, that could provide a bullish tailwind after earnings.

From a technical perspective, Nike is trading at its lowest level since September 2014 and has filled a gap near $40 that was formed in July 2017. If the stock breaks below the $40 support, the next likely downside support is around $35. However, if the shares bounce, resistance is around $52. A move to that level could fill the gap created in March 2026.

Nike share price, July 2014 – present

Sources: TradingView, Michael Kramer

ISM June manufacturing PMI

Wednesday 1 July

The ISM Manufacturing purchasing managers' index (PMI) is expected to fall to 53.7 in June from 54.0 in May. However, investors are likely to focus on the prices paid index, which has recently surged above 80, indicating that inflationary pressures in the manufacturing sector remain elevated. The employment index will be closely scrutinised as investors prepare for the June jobs report due in the following trading session.

The dollar has strengthened meaningfully against currencies such as the euro over the past couple of trading sessions, with the euro falling below support around $1.14. This is important because, if incoming data suggests the Federal Reserve is falling behind the inflation curve, the dollar could strengthen further.

With the euro now below key support, it could weaken further, with the next major support level around $1.1220. In the short term, the euro could bounce first, particularly if the data comes in weaker than expected, suggesting the Fed can afford to be patient or ease market concerns about rate hikes. Current positioning also suggests the euro may be oversold, as it is trading below its lower Bollinger Band and has an relative strength index (RSI) below 30.

EUR/USD, April 2025 – present

Sources: TradingView, Michael Kramer

US June jobs report

Thursday 2 July

Economists expect the June jobs report to show payrolls increased by 135,000, down from 172,000 in May. They also expect the unemployment rate to remain unchanged at 4.3%, while average hourly earnings are forecast to rise by 3.5% year-on-year, up from 3.4%. This will be the headline report of the week and potentially the most important economic release ahead of the July Fed meeting.

A strong report would further strengthen the case for the Fed to focus less on the labour market and more on persistent price pressures as it continues efforts to bring inflation back to target. That could prove very negative for risk assets, particularly the S&P 500, which has struggled since peaking on 2 June. The index continues to trade below its 10-day exponential moving average, which has recently served as resistance.

If the S&P 500 were to break below 7,300, it could open the door to a move towards the 7,150–7,200 range. That would likely heighten concerns that the index has further to fall, especially if it becomes more apparent that the Fed may be forced to raise rates before the end of the year. A move above the 10-day EMA could propel the index back to 7,520.

S&P 500, October 2025 – present

Sources: TradingView, Michael Kramer

Economic and company events calendar

Major scheduled data releases and UK- or US-listed company results include:

Monday 29 June

• Japan: May retail sale

• Eurozone: June consumer confidence

• Results: No major scheduled earnings announcements

Tuesday 30 June

• China: June manufacturing and non-manufacturing purchasing managers' indices (PMIs)

• Eurozone: June inflation data

• Japan: May unemployment rate

• UK: Q1 gross domestic product (GDP)

• US: May Job Openings and Labor Turnover Survey (JOLTS) job openings; June consumer confidence

• Results: Nike (Q4), Constellation (Q1), Sainsbury’s (Q1)

Wednesday 1 July

• Eurozone: June flash consumer price index (CPI)

• Japan: Q2 Tankan survey

• US: June ADP employment change; June Institute for Supply Management (ISM) manufacturing PMI

• Results: General Mills (Q4), Associated British Foods (Q3)

Thursday 2 July

• Eurozone: May unemployment rate

• US: June non-farm payrolls, unemployment rate and average hourly earnings; initial jobless claims

• Results: Lindsay (Q3), Currys (FY)

Friday 3 July

• Eurozone: Composite PMI

• US: Independence Day holiday

• Results: No major scheduled earnings announcements

The Week Ahead: UK CPI, US PCE, Walmart earnings

Welcome to Michael Kramer’s pick of the key market events to look out for in the week beginning Monday 16 February.