H2 outlook: US dollar may reassert itself amid hawkish shift

In part three of our four-part second-half outlook series, Michael Kramer looks at how renewed inflation pressure and hawkish central banks could support the US dollar.

Founder, Mott Capital Management

Faster inflation means higher rates

Monetary policy took a sharp U-turn in the first half of 2026, shifting from markets expecting interest-rate cuts from major central banks to pricing in further rate hikes from some central banks. At the same time, geopolitical tensions in the Middle East escalated, oil prices surged and inflation accelerated.

The European Central Bank and Bank of Japan (BoJ) have hiked rates once, while markets now expect the US Federal Reserve (Fed) to raise rates later this year. This has had a big impact on the foreign exchange market, with the US dollar reasserting itself as the dominant global currency. USD/JPY has climbed back to levels last seen in July 2024, while the euro and pound have given up many of the gains made at the start of the year.

Where monetary policy goes will largely be determined by whether inflation remains elevated and, if so, by how far above central banks' 2% price stability targets. Oil prices and pass-through effects will also play a key role.

Oil prices have fallen sharply, which could take some pressure off central banks to hike. However, with the Fed's latest dot plot and hawkish tilt, it may take some time for policymakers to abandon their hawkish bias, especially as core inflation remains elevated.

A stronger dollar

That said, the technical picture provides plenty of insight into where markets might be headed. With EUR/USD currently sitting at a multi-year support region that has acted as both support and resistance since January 2022, the dollar may continue to strengthen. In the past, the $1.14-1.15 region has been a critical dividing line for the FX market. If it breaks that support level, it may indicate further weakness, with the pair potentially falling towards $1.10.

EUR/USD, October 2024 - present

Sources: TradingView, Michael Kramer

Technical outlook for major currency pairs

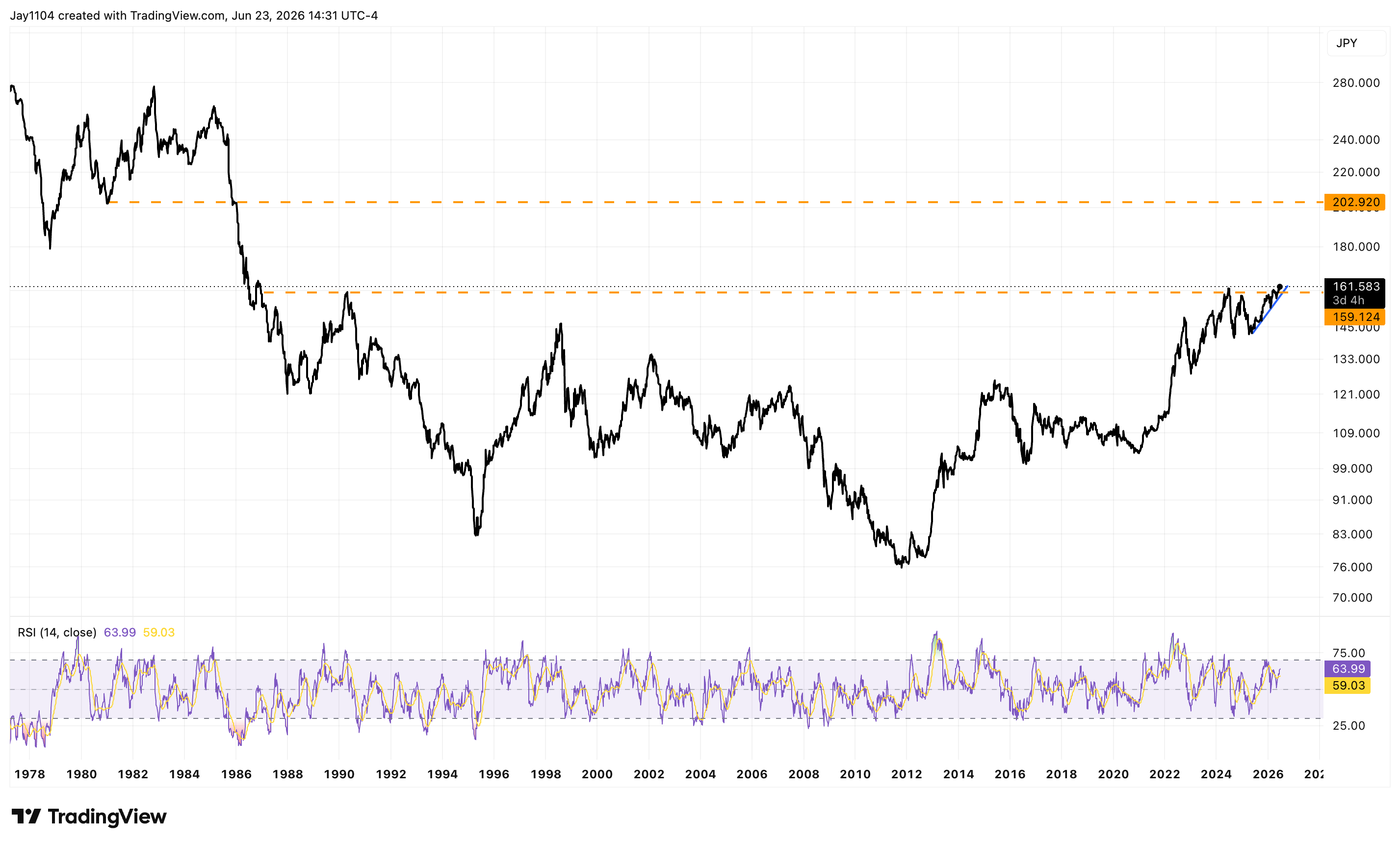

Even with the BoJ having raised rates in June and signalling further hikes later this year, USD/JPY has risen back to ¥161.90, a level last seen in July 2024. One would have to go back to December 1986 to find a weaker yen. While that may sound extreme, a sustained break above ¥162 could eventually put levels such as ¥200 into view over the longer term.

Technically, with so little resistance built up at higher levels, a big move higher becomes possible. Unless the BoJ accelerates the pace of rate hikes or the government scales back some of its spending plans, it seems that intervention may be the only tool left to prevent such a move.

USD/JPY, 1978 - present

Sources: TradingView, Michael Kramer

Could the pound follow the euro and yen lower?

Markets expect the Bank of England to leave rates unchanged throughout most of the year, with an 80% probability of a December hike priced in. That outlook could leave the pound in a similar position to the yen and euro against the dollar.

Meanwhile, GBP/USD has formed what could be a potential head-and-shoulders pattern. A break below the neckline at $1.32 could trigger a decline towards $1.30. Such a move would likely test the lower boundary of a rising wedge pattern, and a break below that support could signal even greater weakness for the pound ahead.

GBP/USD, 2019 - present

Sources: TradingView, Michael Kramer

The Fed may still need to finish the job

Currently, with markets pricing in further Fed rate hikes, the dollar may reassert its leadership, as it did in 2022. However, much is likely to be determined not only by where inflation currently stands, but also by the Fed's inability to return inflation to target over the past five years, after shifting its priorities in late 2024 from inflation to the labour market.

With the labour market now appearing to be in much better shape, the time for the Fed to finish the job on inflation may have arrived. If that proves to be the case, the dollar is likely to continue to strengthen in the second half of 2026.

The euro may weaken further versus the US dollar

EUR/USD has broken below a short-term support level at 1.159 and is now testing a more important support zone near 1.151. If that floor gives way, the pair could slide towards 1.14 as bearish momentum builds and the dollar stays firm after the stronger-than-expected US jobs report.

Yen weakness builds as USD/JPY nears key resistance

USD/JPY is pushing back towards 159.50, a level that acted as support and resistance before Japan's late-April intervention. If that barrier gives way, the pair could retest 160.50, while the Bank of Japan's delayed policy meeting and still-elevated oil prices continue to leave the yen exposed.

EUR/USD may weaken further as key support breaks

EUR/USD has slipped below support around 1.166, increasing the risk that a double-top pattern is now taking shape. If the break holds, the pair could come under further pressure in the days ahead, although a quick recovery back above the neckline would still leave room for a false-break rebound.