CMC Markets is a multi-asset investment platform. The value of your investments may go up or down. When you invest, your capital is at risk.

Why invest with CMC Markets?

*Based on over 2 million unique user logins across CMC's trading and investing platforms, including partners, as at November 2025.

Straightforward price plans

Choose from one of our plans that suits what you need. No hidden fees, no nasty surprises, just straightforward and transparent pricing. FX fees and UK government charges may apply.

When you invest, your capital is at risk.

For the full list of platform benefits, compare our price plans.

See what our customers saying about CMC Invest?

Dive deeper

FAQs

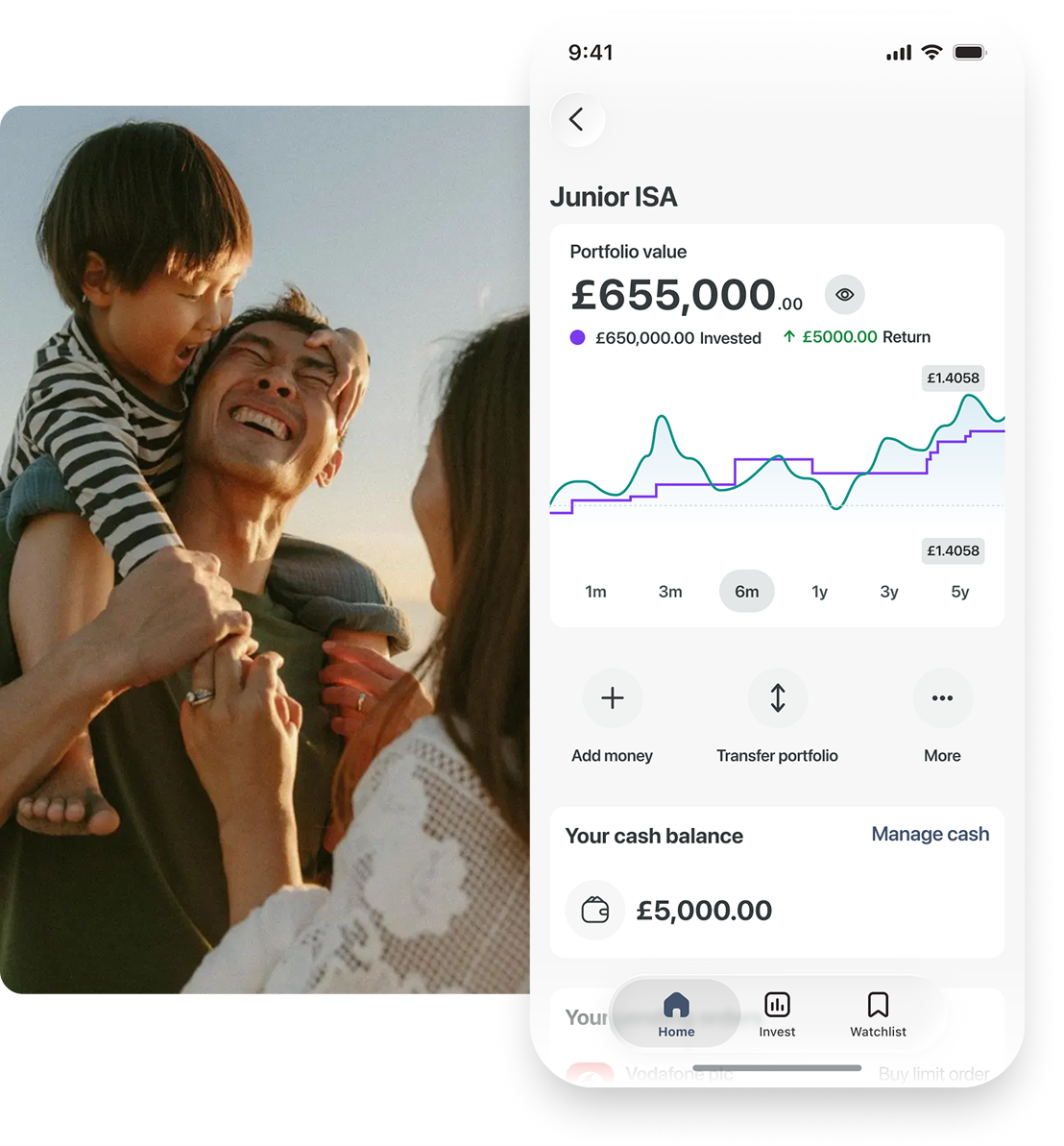

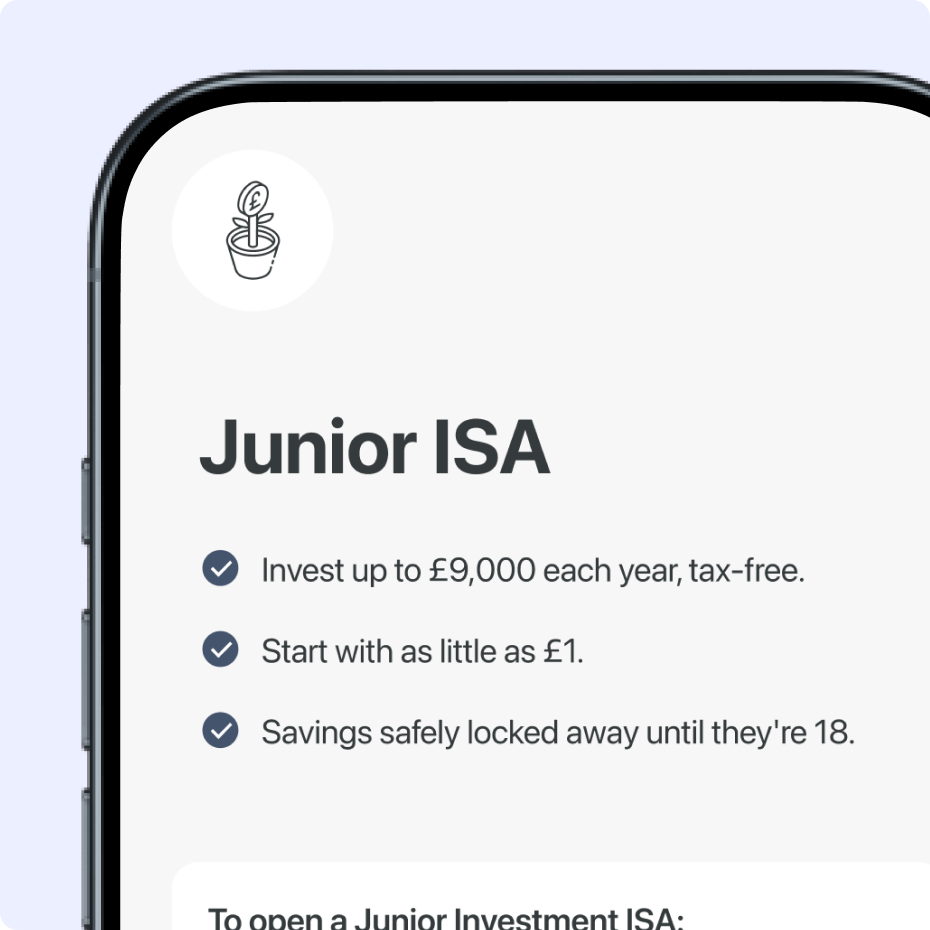

A Junior Cash ISA is a tax-free savings account for children under the age of 18 who are resident in the UK. Parents or legal guardians can save up to £9,000 per tax year, and the money belongs to the child. Funds are locked until they turn 18, helping build a financial foundation for their future.

Yes, CMC Invest is authorised and regulated by the Financial Conduct Authority (FCA) and we have regulatory permissions to hold and control client money.

Learn more about how your money is protected.

Yes, you can. A child can only have one Junior Cash ISA (JISA). If you want to open a new account, you’ll need to transfer your existing JISA to CMC Invest.

All you have to do is download the CMC Invest app, open a JISA, fill out our transfer form in the app, and we’ll work with your current provider to transfer your savings on your behalf. Learn more about our transfer process.

However, if you’re transferring a fixed-rate ISA before maturity (when the fixed-rate ISA ends), you may incur an early closure charge or penalty from your current provider.

Yes, you can. You can transfer a fixed-rate ISA before or after the maturity date (when the fixed-rate ISA ends). However, it's essential to be aware that transferring a fixed-rate ISA before its maturity may incur an early closure charge from your current provider.

If you're a parent or legal guardian, you can open and manage the account for a child under 18 years old who lives in the UK.

A Junior Cash ISA can be opened from as little as £1, and has a £9,000 annual contribution limit across all Junior ISAs – including a Junior Stocks & Shares ISA.

Transferring existing Junior Cash ISAs to CMC Invest can be initiated and managed all within the CMC Invest app. Learn more about our transfer process.

With CMC Invest, the minimum amount you can deposit is £1. You can use your debit card to add funds, but you can’t deposit more than £9,000 across multiple Junior ISAs in the same tax year.

No, you can't. Money can't be withdrawn from a Junior ISA until the child is 18. And any contributions to the Junior ISA can't be refunded and belong to the child.

You can cancel the account free of charge within 14 days of opening. For special circumstance closures, view our terms and conditions.

Currently, we only offer a junior ISA, a flexible Cash ISA and a flexible Stocks & Shares ISA. If you’re interested in us adding other types of ISAs, please let us know using the ‘Send us your feedback’ banner on the home screen in the app.

No, there are no fees to hold a Junior Cash ISA.

Yes, CMC Markets Investments Limited (registration number 948126) is fully authorised and regulated by the Financial Conduct Authority (FCA) in the UK. Retail client money is held in segregated client bank accounts, and money held on behalf of clients is distributed across a range of major banks, which are regularly assessed against our risk criteria.

Under the FCA's client money rules, we're required to segregate client money from our own funds (unless you agree with us otherwise). The money held in segregated bank accounts does not belong to us and will be held in a way that enables it to be identified as client money. Learn more about client money regulations.

In the UK, if you have a Stocks & Shares ISA or Self-invested Personal Pension (SIPP), you don’t need to pay capital gains tax on any profits you make from selling investments, or dividend tax on income you receive from companies.

Any profits and dividend income you make through a General Investment Account is taxable. This will be shown in your ‘consolidated tax certificate’, which you'll receive from us following the end of each tax year.

Tax treatment depends on your individual circumstances and may be subject to change in the future.

Visit our contact us page for details on how you can get in touch with us.

Ready to get started?

Open an account and start building wealth today.

When you invest, your capital is at risk.