Warsh's hawkish debut weighs on Bitcoin, gold and risk appetite

Kevin Warsh's first policy message has strengthened the dollar and pushed short-term rate expectations higher. The reaction is weighing on gold and Bitcoin while leaving equity markets more cautious near record highs.

Market Analyst

Warsh is trying to rebuild a more orthodox Fed

Kevin Warsh's first message as Fed chair has been read by markets as clearly hawkish. He wants to modernise the Federal Reserve through five workstreams covering monetary-policy frameworks, communication, regulation, balance-sheet operations and data modernisation.

The bigger signal is philosophical. Warsh is arguing for a more orthodox and less interventionist Fed, with a smaller balance sheet and less focus on cushioning market volatility. If that approach sticks, investors may need to price a weaker "Fed put" and a closer link between asset prices, economic data and real monetary conditions.

Inflation risk keeps policy tighter for longer

Warsh's starting point is that inflation is mainly determined by monetary policy and that returning it to the 2.0% target remains the priority. He also described the economy as resilient, supported by productivity and capital investment, while the labour market remains stable enough to avoid forcing a quick policy retreat.

That combination gives the Fed room to sound restrictive. If growth is holding up and inflation is still viewed as the main risk, markets have less reason to expect near-term relief from lower rates. That is why the speech has mattered beyond the Fed itself: it changes the policy tone across the dollar, Treasuries and rate-sensitive assets.

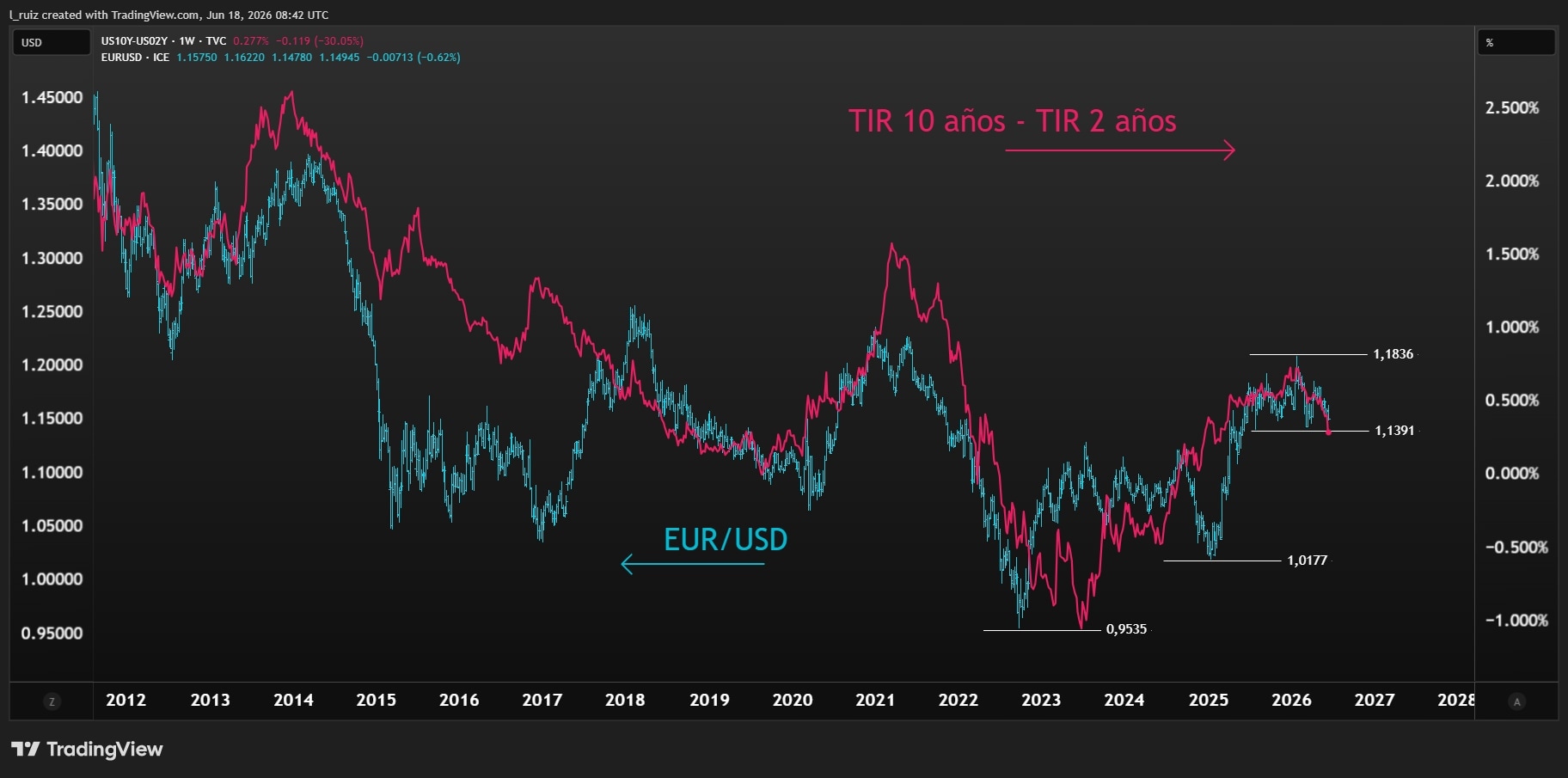

A stronger dollar and flatter curve are the first market signals

The immediate reaction has come through the front end of the US rates market. The source says short maturities moved sharply higher, while longer maturities barely moved, creating a strong flattening of the yield curve. Fed funds pricing is now described as discounting two 25-basis-point hikes, the first in September 2026 and the second in January 2027.

The US dollar has strengthened as well. Warsh's firm stance against political pressure for rate cuts has been interpreted as a signal of Fed independence, and that has added to the currency's rate support. For EUR/USD, the combination of a stronger dollar and flatter US curve is now one of the clearest ways to track how markets are processing the new Fed tone.

EUR/USD and US yield spread, weekly

Sources: TradingView, Luis Francisco Ruiz.

Bitcoin, gold and equities are losing momentum

Higher rates and a stronger dollar are a difficult mix for assets that often benefit from lower real yields. The source says gold and Bitcoin have both stalled after rebounding from key support zones, with Bitcoin near $59,275 and gold near $4,098 an ounce highlighted as important reference points.

Equities are also hesitating near record territory. The Spanish article points to the S&P 500 around 7,620 points and the Nasdaq 100 around 30,762 points, with both indices giving back some of their recent momentum despite a better geopolitical backdrop. For traders, the message is that Warsh's Fed debut has made financial conditions feel tighter, even before any additional rate increase is delivered.

Warsh's Fed debut puts the dot plot and independence in focus

The Federal Reserve is expected to leave rates unchanged today, but Kevin Warsh's first Fed press conference and the new dot plot may matter more than the decision itself. Markets are watching whether he reinforces an independent, restrictive policy stance or opens the door to a softer message.

EUR/USD may weaken further as key support breaks

EUR/USD has slipped below support around 1.166, increasing the risk that a double-top pattern is now taking shape. If the break holds, the pair could come under further pressure in the days ahead, although a quick recovery back above the neckline would still leave room for a false-break rebound.

S&P 500 hits a record high, but this was no ordinary rally

S&P 500 closed at a fresh record on 15 April after an 11-session 10.7% surge that ranks among the strongest such runs since 1957. The rally appears to have drawn support from easing geopolitical risk, short-covering and CTA buying, with better earnings expectations helping the breakout hold.