The Week Ahead: US CPI, PCE, GDP; Delta earnings

Welcome to Michael Kramer’s pick of the key market events to look out for in the week beginning Monday 6 April.

Founder, Mott Capital Management

Published: Thursday, 2 April 2026 at 1.00pm (UK time)

It will be a busy week for US trading. It also marks the final week before we fully enter earnings season for US companies, with many of the large US banks scheduled to report from 13 April. The key events this week are the US consumer price index (CPI) inflation report on Friday, and the February personal consumption expenditures (PCE) report a day earlier. Given the recent surge in oil prices, traders will be paying close attention to these releases. Additionally, the final US GDP reading for the fourth quarter is released on Thursday.

Delta earnings

Wednesday 8 April

For the first quarter of 2026, the NYSE-listed airline is expected to see earnings increase by approximately 37.3% to $0.63 per share, while revenue is forecast to grow by 7.8% to $14bn. In Q2, analysts predict earnings growth will slow to just 2%, reaching $2.14 per share, with revenue anticipated to rise by 10.5% to $17.1bn. Investors will also be closely monitoring the company’s guidance, and particularly the potential impact of higher oil prices on jet fuel costs.

On the technical chart, there has not been a significant price change despite the recent sharp sell-off in the broader market. As of 1 April, the stock was down about 10% from its intraday highs in mid-February. Currently, Delta’s share price is trading near resistance at $70 per share, while support is close to $63. Due to volatility driven by oil price movements, the outlook remains difficult to predict. That said, the current trend is downward, and the relative strength index (RSI) is also trending lower. If the shares can’t climb above $68, a double-top could form. A break below $63 would confirm this pattern, and could see the stock fall back towards the $57.5 level.

Delta share price, Oct 2025 – present

Sources: TradingView, Michael Kramer

US GDP and PCE

Thursday 9 April

Analysts forecast that the final reading of Q4 GDP will slow to 0.6%, down from the previous estimate of 0.7%. However, markets are likely to focus on the PCE reading. The headline number is expected to rise by 0.4% month-on-month in February, up from 0.3% in January, while core PCE is also forecast to remain at 0.4%. This is the Federal Reserve’s preferred measure of inflation, as it excludes much of the noise often seen in the CPI report.

This will be an important release, particularly for FX markets. The euro has been showing signs of strengthening against the dollar, although it seems to be stalling near resistance around $1.16. A hotter-than-expected inflation reading is likely to further decrease expectations for US rate cuts. In that scenario, the possibility of no rate cuts – or even a rate hike – could begin to re-emerge, which would be a bearish signal for the euro, and could push it back below the $1.1520 level seen just a few days ago.

EUR/USD, Aug 2025 – present

Sources: TradingView, Michael Kramer

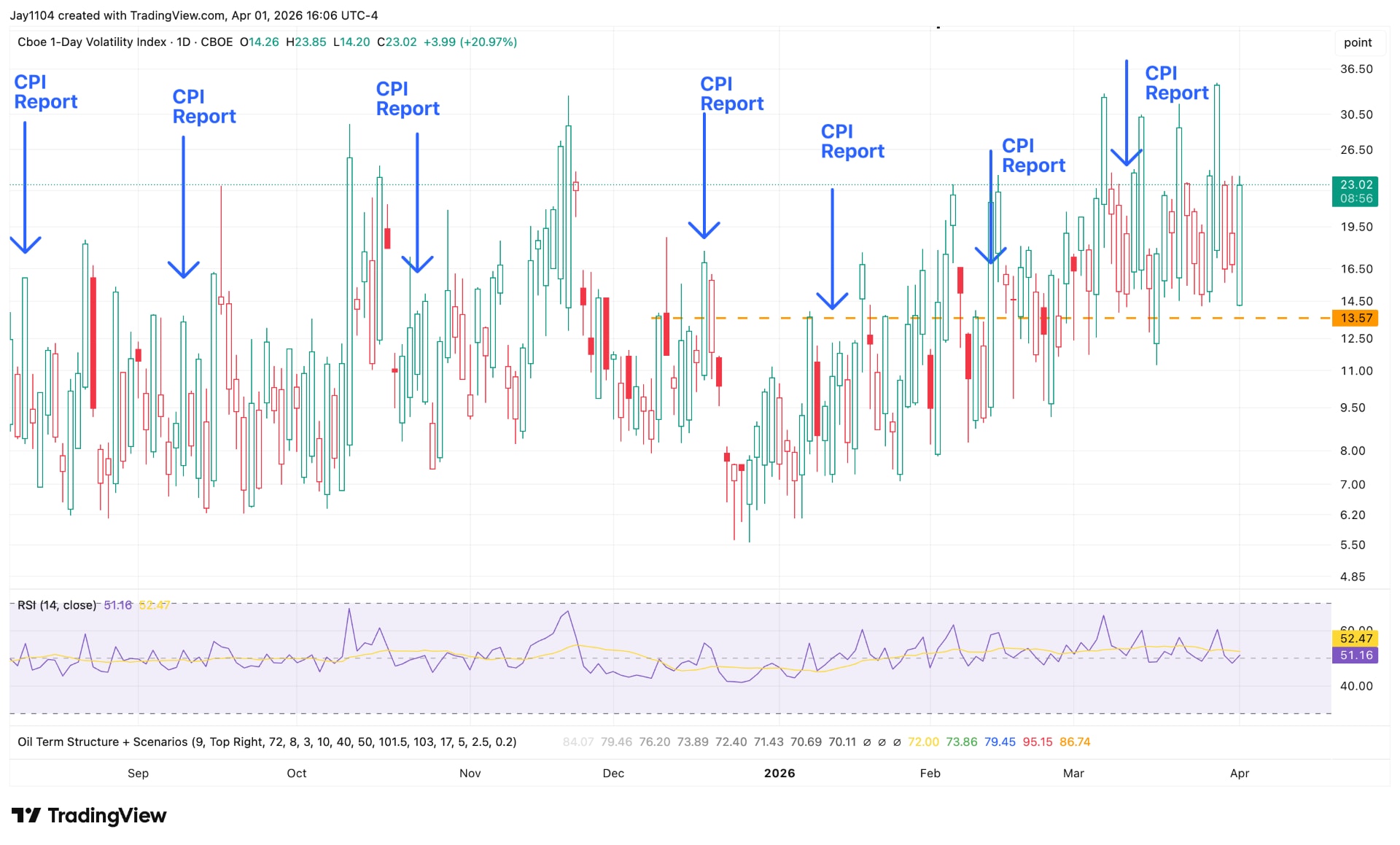

US CPI

Friday 10 April

The March US CPI report is set to be the key economic release of the week. Estimates indicate that headline CPI will rise by 0.9% in March, up from 0.3% previously, while core CPI is forecast to increase by 0.3%, up from 0.2%. This is likely to be a particularly tense period for equity markets, potentially driving up implied volatility as investors position themselves ahead of the release.

A key metric to watch will be the one-day VIX (volatility index), which has historically risen sharply ahead of major market-moving events, and then declined once the event has passed. This dynamic often creates a post-event rally in stock indices, as falling implied volatility prompts the unwinding of hedged positions, which in turn can push stock prices higher.

This will be especially important heading into the report. If implied volatility rises to elevated levels, as seen in recent periods, and the CPI reading does not surprise to the upside, a stabilisation in sentiment could trigger a relief rally in equity markets.

One-day volatility index, Sep 2025 – present

Sources: TradingView, Michael Kramer

Economic and company events calendar

Major upcoming economic announcements and scheduled US and UK company reports include:

Monday 6 April

• Eurozone: Consumer confidence (April)

• US: Services purchasing managers index (PMI) (March)

• Results: Gaming Realms (H1), Nano-X Imaging (Q1), OS Therapies (FY)

Tuesday 7 April

• Eurozone: Services PMI (March)

• New Zealand: Interest-rate decision

• UK: Services PMI (March)

• US: Durable goods (February)

• Results: Levi Strauss (Q1), JTC (FY)

Wednesday 8 April

• Eurozone: Producer price index (PPI) (February), Retail sales (February)

• Germany: Factory orders (February)

• US: FOMC minutes

• UK: Construction PMI (March), house price index (March)

• Results: Constellation Brands (Q4), Delta Air Lines (Q1)

Thursday 9 April

• US: PCE price index (February), personal income (February), personal spending (February)

• Results: Enwell Energy (Q4), Simply Good Foods (Q2), WD-40 (Q2)

Friday 10 April

• China: Consumer price index (CPI) (March), PPI (March)

• Eurozone: Consumer price index (March)

• US: CPI (March), factory orders (March), Michigan consumer sentiment index (April)

• Results: BlackRock (Q1)

The Week Ahead: US ISM, jobs report, Nike earnings

Welcome to Michael Kramer’s pick of the key market events to look out for in the week beginning Monday 30 March.