Stocks on the brink of a correction. Could the “TACO trade” strategy fail this time?

Major indices such as the S&P 500, Dow Jones Industrial Average and Nasdaq Composite are recording a fourth consecutive week of losses, approaching a 10% decline from their recent peaks.

CMC Markets Poland

US markets approach correction territory

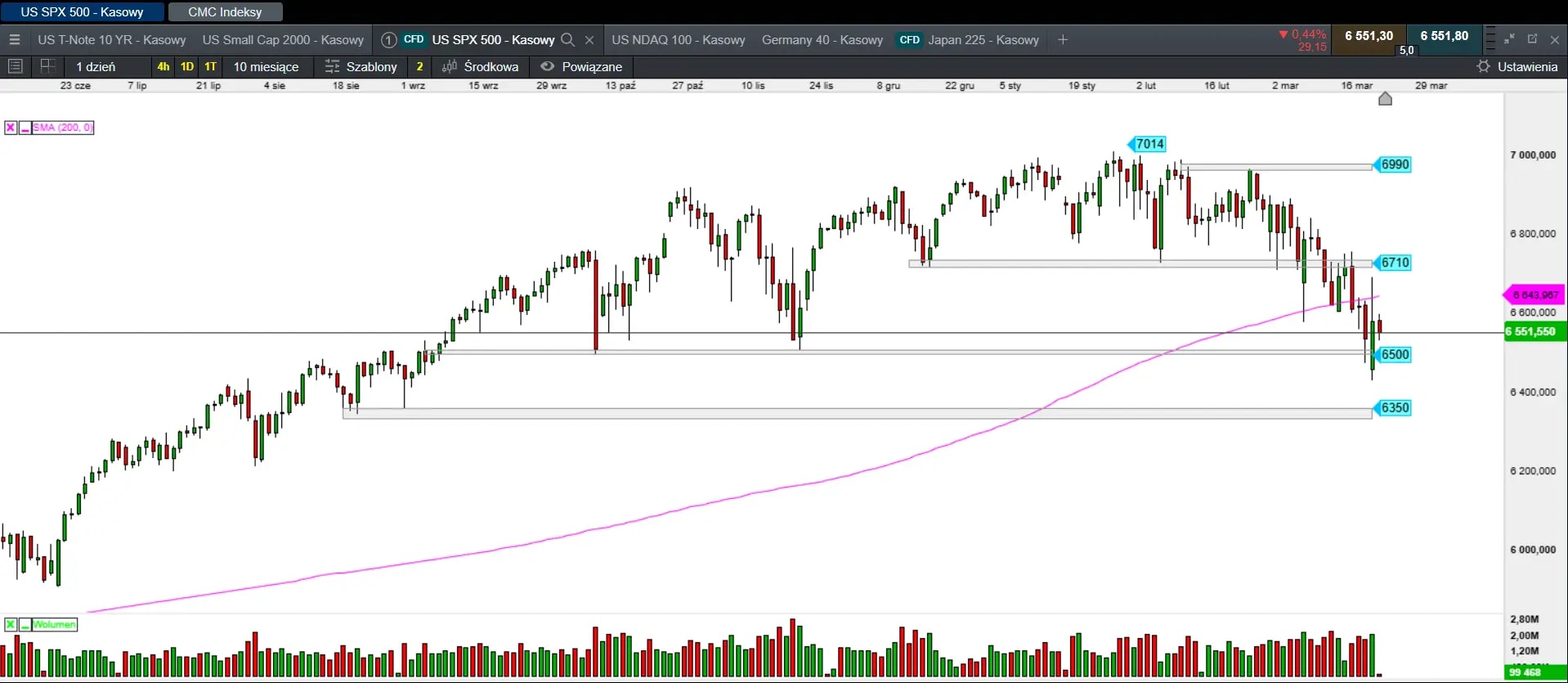

US equity markets are at a critical juncture, hovering on the edge of a correction after a series of sharp declines. Major indices such as the S&P 500, Dow Jones Industrial Average and Nasdaq Composite are posting a fourth consecutive week of losses, nearing the threshold of a 10 per cent drop from their recent highs. The small-cap Russell 2000 index has already crossed that line, which investors interpret as a warning signal for the broader market. This situation is directly linked to the escalation of the conflict with Iran and uncertainty over further actions by the White House administration, casting a shadow over sentiment on Wall Street.

What is the “TACO trade” strategy?

A key concept dominating current market discussions is the so-called “TACO trade”. The term derives from the acronym “Trump Always Chickens Out” and has become something of an article of faith for many investors. The strategy is based on the assumption that Donald Trump, known for placing significant importance on stock market performance as a measure of his policy success, will ultimately soften his stance or withdraw from the most radical decisions once markets begin to fall sharply. Historically, investors who bought equities during “panic” triggered by tariffs or military threats have fared relatively well, anticipating a swift rebound following an inevitable moderation in Washington’s rhetoric.

Why the strategy may fail this time

However, experts now warn that relying on the “TACO trade” pattern could prove to be a costly mistake. The situation in the Middle East, including attacks on energy infrastructure and the blockage of the Strait of Hormuz, has triggered a complex chain of events that the US president may not fully control. Analysts stress that the deeper and longer the conflict persists, the more difficult it becomes to resolve it through a simple policy reversal. Unlike trade disputes, where tensions can be eased with a single social media post or a delay in tariffs, actual military actions and their impact on commodity prices tend to be far more persistent.

Technical signals point to a trend reversal

The market is beginning to recognise that traditional technical support is weakening. The S&P 500 has closed below its 200-day moving average for the first time in over 200 sessions, technically confirming a shift to a downward trend. Investors who had previously been sceptical about the sell-off now fear that the current crisis is not merely a temporary disruption, but the beginning of a deeper and more painful decline. If optimism based on expectations of White House intervention fades, markets may face a harsh reality, realising that this time there may be no easy escape.

Source: own calculation, 24 March 2026.

Session summary in Europe and the US

The past week on European exchanges was marked by concerns over energy security and, consequently, fears of rising inflation and slowing economic growth. Bullish investors were encouraged by a post from Trump, prompting a rush into equities that pushed benchmarks into positive territory. The key question is whether investors have come to terms with the possibility of a deeper correction. Apart from the FTSE 100 (−0.24%), other leading indices gained between 0.61% (Stoxx 600) and 1.22% (DAX).

Wall Street is also experiencing heightened volatility. Yesterday’s session, following a series of declines, ended in positive territory. The Dow Jones rose by 1.38%, the S&P 500 increased by 1.15%, and the Nasdaq 100 closed up 1.38%.

Asia session – a return to gains, but for how long?

Asian markets are posting gains today, following yesterday’s session on Wall Street. However, this appears to be largely a rebound after the previous sell-off. The prospect of rising inflation and the end of the low-interest rate environment continues to weigh on investor sentiment. The Nikkei 225 is up 0.61%. Australia’s S&P/ASX 200 has risen by 0.41%, while South Korea’s KOSPI has gained 2.49%. Other markets: Hong Kong (1.39%), Shanghai (0.67%), Sensex (0.81%), Singapore (0.24%). The Asia Dow index is up 1.42%.

Session summary on the Warsaw stock exchange (GPW)

The previous week was dominated by selling pressure. The current week, however, began in a tense atmosphere, with gains driven largely by Trump’s comments on platform X. Globally, the situation in risk assets remains highly strained. Fear has spread not only in Warsaw but across global markets. When markets are under pressure, emerging markets tend to face heightened selling activity. Rising US bond yields have amplified concerns about inflation, which could lead to higher interest rates later in the year and, consequently, increased financing costs.

Market sentiment has shifted dramatically within just a few weeks. On the Warsaw exchange, conditions remain highly dynamic, with early signs of a correction emerging. Demand, which had previously driven the market, has given way to supply pressure. Deteriorating sentiment across major European exchanges and Wall Street has had a clear impact. The bearish camp, which argued that optimism on the GPW was gradually fading, appears to be correct, and profit-taking on long positions may further support a pullback.

The Polish market is not decoupled from global trends, and if scepticism persists globally, a correction becomes increasingly likely, especially after such a strong rally. However, only a sustained drop below the low of 4 December 2025 would constitute a serious risk and could trigger a deeper decline towards 2,378 points.

The WIG20 initially declined after a weak opening. Around midday, a post by Trump about postponing attacks on Iranian power plants boosted demand, quickly pushing the index into positive territory. From that point onwards, trading remained relatively uneventful, with the chart showing limited volatility.

Turnover on the broad market reached PLN 3.2bn. The WIG gained 0.53%. The blue-chip index rose by 0.62%. WIG20 futures increased by 0.8%, closing at 3,262 points. Mid-cap stocks also contributed positively, with the mWIG40 up 0.61%. The sWIG80 was the only index to close lower, falling by 1.33%.

Silver's next big move may be lower

Silver has continued to trade sideways as implied and realised volatility cool. A break below $54 could open the door to a move towards $49.50, while reclaiming $60 would be needed to revive upside momentum.