Micron earnings could test the AI memory boom

Micron reports fiscal third-quarter results after the US close on Wednesday 24 June, with analysts expecting another explosive quarter as AI data-centre demand strains memory supply. Guidance may matter more than the headline numbers, because the share-price rally has already priced in a powerful HBM cycle and leaves little room for disappointment.

Market Analyst

Micron has become a market-wide AI test

Micron Technology is due to report fiscal third-quarter results after the US close on Wednesday 24 June, with the official earnings call scheduled for 4:30pm New York time. The timing matters because the stock is no longer being treated as a normal memory-cycle story. It has become one of the clearest market tests of whether AI infrastructure spending is still accelerating.

The Spanish source frames Micron as a new thermometer for the artificial-intelligence investment cycle. Investors have spent much of 2026 moving beyond the obvious hyperscaler winners and into the suppliers of critical components for data centres. That shift has pushed memory companies into the spotlight, because high-bandwidth memory, or HBM, has become essential for advanced AI systems.

Expectations leave little room for a routine beat

The bar is unusually high. The source cites consensus expectations for revenue of $35.75bn, up 284% year on year, and earnings per share of $20.76, up 986%. Recent market coverage points to a similar setup, with analysts focused on whether Micron can keep margins near the exceptional levels created by tight supply and strong AI demand.

That is why a simple beat may not be enough. Micron has already made a huge valuation jump this year, with the stock trading around the $1.2tn market-cap area even after an intraday pullback on 23 June. The source also notes that Morningstar's valuation work points to stretched pricing, so the debate is not whether the company is growing, but whether the growth can keep justifying the price already paid by investors.

Guidance may matter more than the quarter

The most important part of the release is likely to be guidance. The source says the market is looking for next-quarter revenue of about $43.14bn, which means investors will be watching closely for signs that HBM demand remains strong enough to absorb more capacity and support high selling prices.

This is where Micron's results can spill into the wider semiconductor trade. If management confirms that AI customers are still competing for memory supply, the report could reinforce momentum across the US Semiconductors basket and the Nasdaq 100. If guidance suggests the supply squeeze is beginning to ease, investors may question whether the best part of the margin cycle has already been priced in.

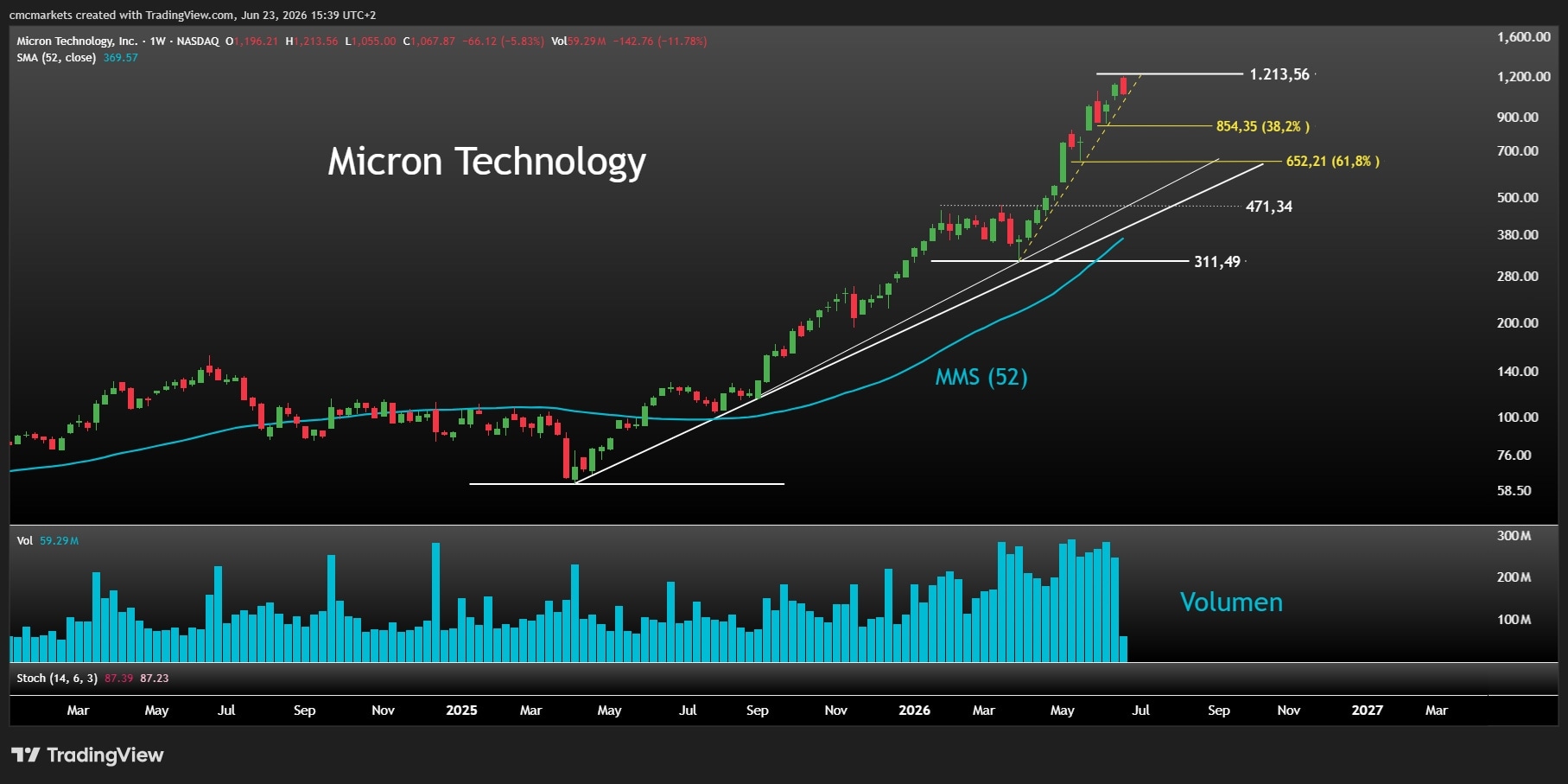

The chart is still strong, but volatility is rising

The source's technical read is constructive on the long-term trend, but more cautious in the short term. Micron remains in a powerful uptrend, with volume having supported the move over recent months. But the approach of earnings has increased volatility, and the stock has started to lose the short-term rising trendline that had guided the rally since March.

The Spanish source highlights the 38.2% Fibonacci retracement near $854.35 as the first major support level from the March-to-record-high advance. That does not imply the rally is over, but it does show how far the stock could correct while still preserving a wider bullish structure.

Micron Technology, March 2024 - present

Sources: TradingView, Luis Francisco Ruiz.

What could keep the rally alive

For the bull case to stay intact, Micron probably needs more than strong backward-looking numbers. Investors will want evidence that HBM shipments, long-term customer commitments and pricing power can remain strong through the next few quarters. Commentary on margins will be especially important, because the market is trying to work out whether current profitability is cyclical peak behaviour or a more durable change in the economics of memory.

The opposite risk is that the company reports excellent numbers but fails to raise expectations further. In a stock that has already moved so far, that could be enough to trigger profit-taking. A weaker guide would matter beyond Micron itself, because it would test the same AI-capex story that has been supporting Nvidia, Broadcom, Marvell and the wider S&P 500 growth trade.

The Week Ahead: Global PMI data, Micron earnings, US PCE

Welcome to Michael Kramer's pick of the key market events to look out for in the week beginning Monday 22 June.

Broadcom could test how far AI euphoria can stretch

Broadcom reports with its shares near record highs, valuation multiples stretched and investors still demanding proof that the AI spending cycle is accelerating rather than peaking. Strong growth may not be enough on its own if the company cannot also convince markets that custom AI chips and hyperscaler demand can keep justifying extreme expectations.