Gold has faltered during the Middle East crisis, but is it still a safe haven?

Gold has disappointed during the latest Middle East shock, falling more sharply than the S&P 500 and reopening the debate over its role as a defensive asset. Even so, the longer-term picture still suggests the metal may matter as a hedge if the conflict becomes a more persistent stagflationary shock.

Market Analyst

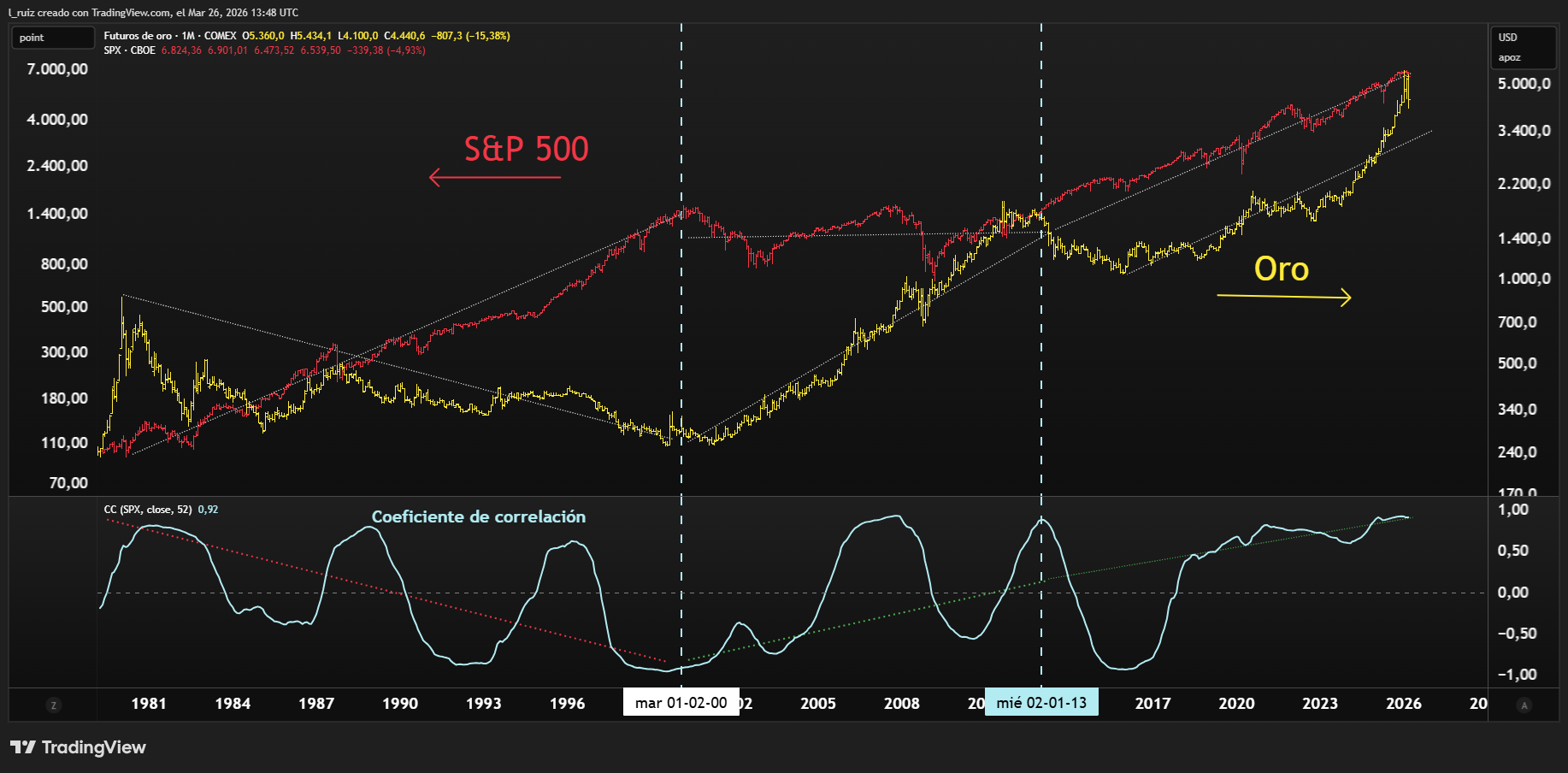

Gold has underperformed during the latest shock

Gold has shown greater relative weakness than the S&P 500 during the latest Middle East crisis. Since the conflict escalated, the metal has fallen by more than $1,000 an ounce, around 20%, while the S&P 500 has been more resilient with a drawdown closer to 5%.

That underperformance, combined with gold's recent positive correlation with equities, has reopened the debate over whether it is still behaving as a true hedge when geopolitical stress intensifies.

The longer-term record still supports gold's role

Despite the current noise, the longer-term picture from 1980 to 2026 still supports gold as a non-correlated and complementary asset. During the strong equity expansion of the 1980s and 1990s, gold remained in a structural downtrend, while in the crisis period from 2000 to 2012 it behaved much more like a defensive asset as the dotcom bust and the global financial crisis hit equities.

That history matters because it suggests the current episode may be distortion rather than proof that gold has permanently lost its defensive function.

Source: TradingView. 26 March 2026.

Gold and the S&P 500 have become more synchronised

The main anomaly has appeared over the past decade, when the correlation between gold and the S&P 500 has moved much closer to one. That points to a shift away from the traditional alternation between risk-on and risk-off assets.

The article argues that this has been driven by structural forces such as larger deficits, rising debt burdens, quantitative easing and abundant liquidity, all of which may have weakened confidence in the fiat system. In that environment, the S&P 500 and gold may have started to behave more like complementary assets responding to global monetary debasement rather than direct competitors for capital.

Gold may be acting as a tactical savings buffer

That structural backdrop is now colliding with a fresh geopolitical layer. As tensions rise between the western bloc and the BRICS economies, some countries may be using gold as a tactical reserve to absorb higher energy costs and defence spending.

In the short term, that may be creating selling pressure on the metal rather than supporting it. The same reserves that are accumulated strategically over time may also be mobilised temporarily when funding stress rises and transactions still need to be settled largely in US dollars.

Source: TradingView. 27 March 2026.

The Ukraine war offers a useful precedent

The current pattern has parallels with the 2022 invasion of Ukraine. At that time, countries such as Kazakhstan and Uzbekistan became net sellers of gold, while Russia may also have relied on gold reserves as a form of emergency funding under sanctions pressure.

A similar dynamic may now be developing in economies such as Jordan, Lebanon, India, Egypt or Turkey. That idea will need to be tested against later data from the World Gold Council, but it offers a plausible explanation for why gold may be weakening in the middle of a geopolitical shock.

Gold and equities may diverge again if the shock becomes structural

The key question is whether the conflict becomes a more durable macroeconomic shock. If it pushes major economies closer to a mix of weaker growth and persistent inflation, the probability of recession may rise materially.

In that kind of environment, gold and equities may begin to separate again, with the metal recovering its role as a hedge against systemic risk while the S&P 500 remains exposed to weaker earnings and tighter financial conditions.

Gold rebounds from the 200-day SMA after clearing excesses and acting as a source of liquidity during the war

Gold is rebounding from its 200-day simple moving average after a sharp pullback driven by deleveraging, exchange-traded fund outflows and liquidity demand during the Iran war. The move suggests the longer-term uptrend may still be intact, although positioning and macro stress remain important near-term drivers.

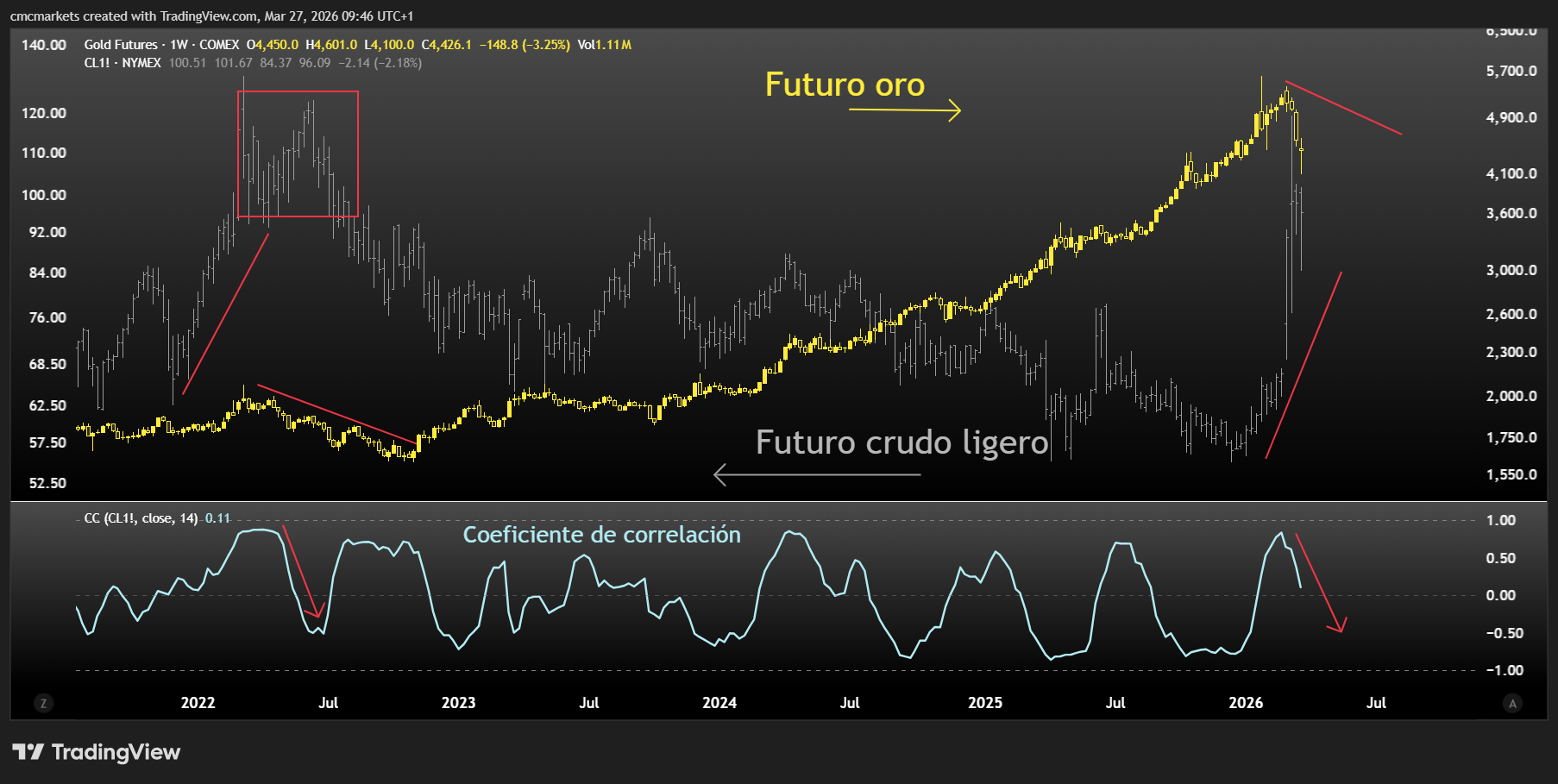

Gold may be heading below $4,000

Oil-price volatility, higher interest rates and a stronger dollar have left gold trading in a volatile range since mid-March. A bear flag, a weaker relative strength index and lower gold volatility may suggest the metal could move below $4,000.

S&P 500 Q1 results season starts with optimism, rich valuations and asymmetric risk

The Q1 earnings season is starting with high expectations for the S&P 500, led by financials and closely watched semiconductor names such as ASML and TSMC. With valuations still demanding and macro momentum slowing, the risk to equities may be more skewed to disappointment than upside surprise.