BoJ, Fed, BoC, ECB and BoE week: how the energy shock could ripple through FX

A packed week of central bank meetings may not bring immediate rate changes, but the energy shock is reopening sharp divergences across FX as policymakers face very different inflation and growth trade-offs.

Market Analyst

A crowded central-bank week is likely to bring more caution than action

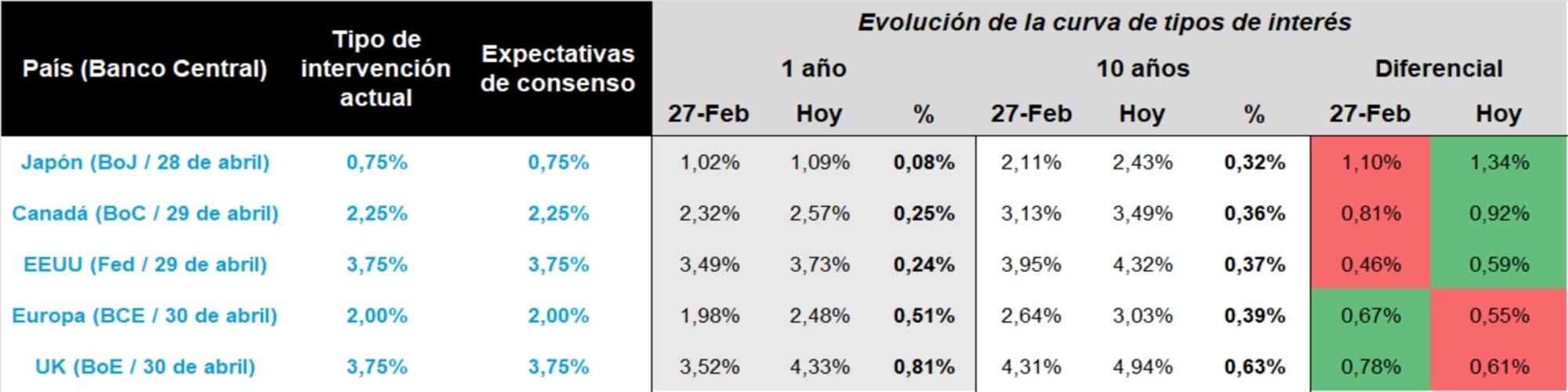

The Bank of Japan, the Bank of Canada, the Federal Reserve, the Bank of England and the European Central Bank are all due to meet this week. The broad expectation is unchanged policy across the board, with officials still in wait-and-see mode after the start of the conflict in the Middle East.

Even so, financial conditions are already tightening through the market rather than through official rates. Yield curves have shifted higher, credit spreads have widened and volatility has picked up, which means policymakers may feel less pressure to move immediately and more pressure to avoid damaging growth.

The energy shock is not hitting every economy in the same way

That is where the FX story starts to matter. The article argues that the latest energy shock is creating an asymmetric backdrop: energy exporters such as Canada and the United States have more room to absorb it, while Japan, the UK and the eurozone remain more vulnerable to a stagflation-style squeeze.

For markets, that puts the focus on guidance rather than on the policy rate itself. Traders will be listening for any hint about how each central bank sees inflation persistence, curve pressure and the balance between protecting growth and defending credibility.

Central bank yield curves, 27 February - 27 April 2026

Sources: CMC Markets, Luis Francisco Ruiz.

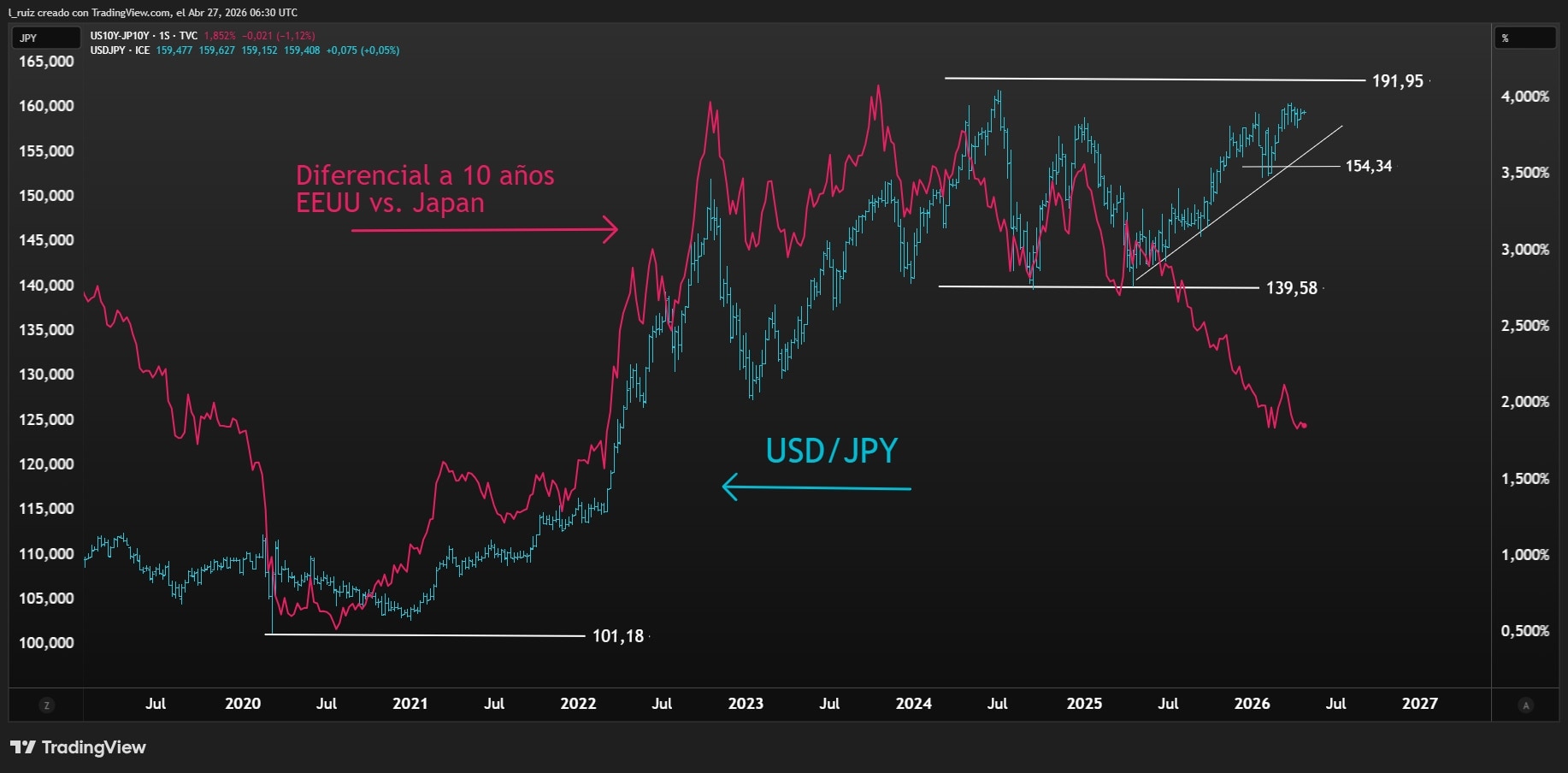

The yen still offers the most dramatic risk-reward setup

Japan remains the most fragile case in the pack. The source analysis argues that the Bank of Japan is still committed to a very gradual path, but longer-dated Japanese yields are rising anyway, which suggests the market is testing the central bank's grip on the curve.

At the same time, the yen remains under heavy selling pressure. The combination of rising yields and a weakening currency is an uncomfortable signal, and the article suggests the BoJ may still need to lean on Treasury sales to slow the move. That leaves the yen looking risky, but potentially attractive from a reward perspective as it trades near multi-decade extremes against many peers.

USD/JPY and US-Japan 10-year yield spread, 2020 - 2026

Sources: TradingView, Luis Francisco Ruiz.

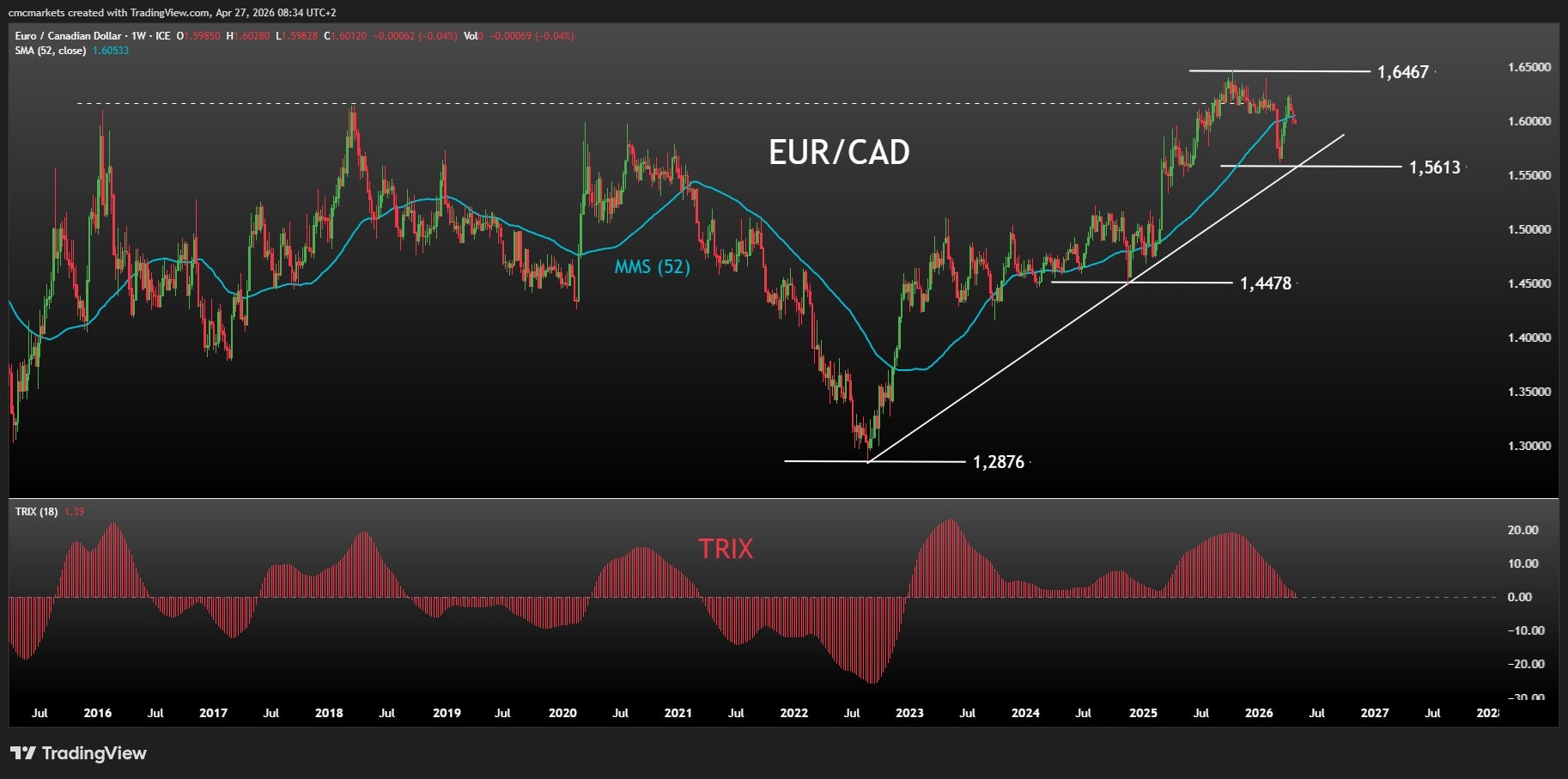

Canada and the US look better placed to absorb the shock

Canada looks more resilient because higher energy prices help cushion the economy. The source view is that the Bank of Canada may eventually need a technical 25 basis-point adjustment, but that would be more of a fine-tuning move than the start of a fresh aggressive hiking cycle. If oil stays firm, the macro gap with Europe could continue to support the Canadian dollar.

The Fed, meanwhile, still looks like the calmest of the major central banks. The article points to the US economy's energy-exporter status, its technology-led investment strength and a March core CPI reading that held near 2.6%. With markets still pricing the policy rate at 3.75% over the next year, the dollar may keep benefiting from relative cyclical strength and a still-wide rate differential.

EUR/CAD, 2015 - 2026

Sources: TradingView, Luis Francisco Ruiz.

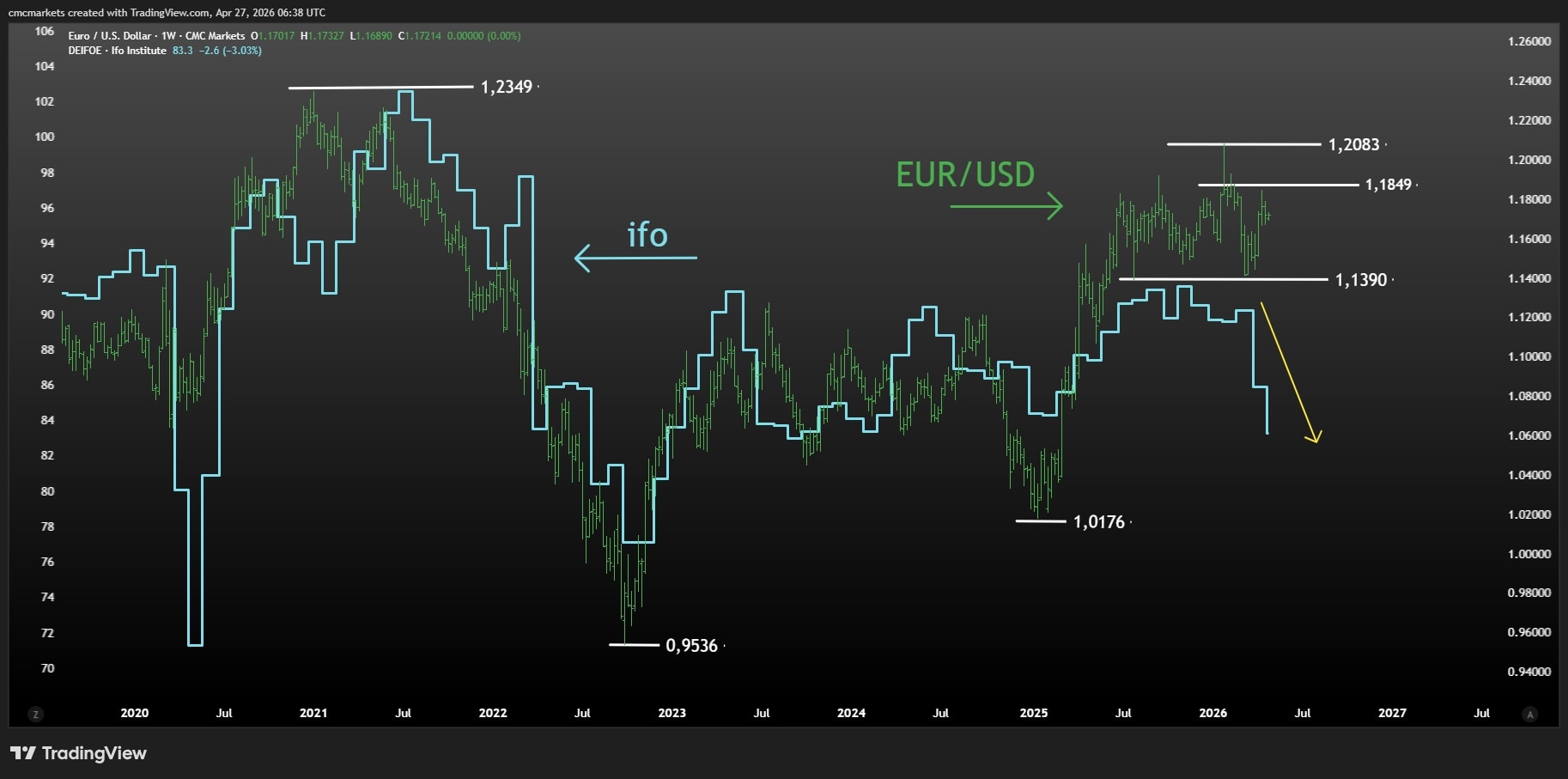

The Bank of England and the ECB remain more exposed

The Bank of England is dealing with the most obvious curve stress. The source analysis describes the UK gilt market as close to a red line, with 10-year yields pressing towards 5.00% as investors worry about the inflation and growth hit from higher energy prices. That may support sterling temporarily through higher rates, but it also increases the risk of a more disorderly move if systemic concerns build.

For the ECB, the challenge is different but no less uncomfortable. Recent business surveys suggest the eurozone is slipping deeper into stagflation territory, yet the market is already leaning towards a 25 basis-point increase at the next meeting. That could leave the euro struggling in an environment where policy tightening remains very gradual, growth stays weak and differentials only narrow slowly.

EUR/USD and German ifo index, 2020 - 2026

Sources: TradingView, Luis Francisco Ruiz.

FTSE 100 edges higher as UK retail sales lift sentiment

The FTSE 100 traded modestly higher around 10,671 late on Friday morning as stronger UK consumer confidence and retail sales data supported sentiment, while investors watched PMIs and Middle East risks ahead of the weekend.

DAX stabilises as SAP beats expectations while automakers disappoint

The DAX is set for a steadier start after yesterday's decline, with SAP's stronger cloud-driven results offsetting weakness in Porsche, Volkswagen and Mercedes-Benz as higher oil prices, PMIs and tariff risks keep investors cautious.