US CPI at 14:30 may act as a near-term catalyst for the USD and S&P 500

US March CPI is due at 14:30 on Friday in an environment of elevated liquidity stress. The release may act as a near-term catalyst for the USD and S&P 500, with markets especially sensitive to core inflation.

Market Analyst

Headline inflation may rise more sharply than core

US March CPI is due at 14:30 on Friday. It is a high-impact release that may generate immediate volatility across the dollar, equities and bonds.

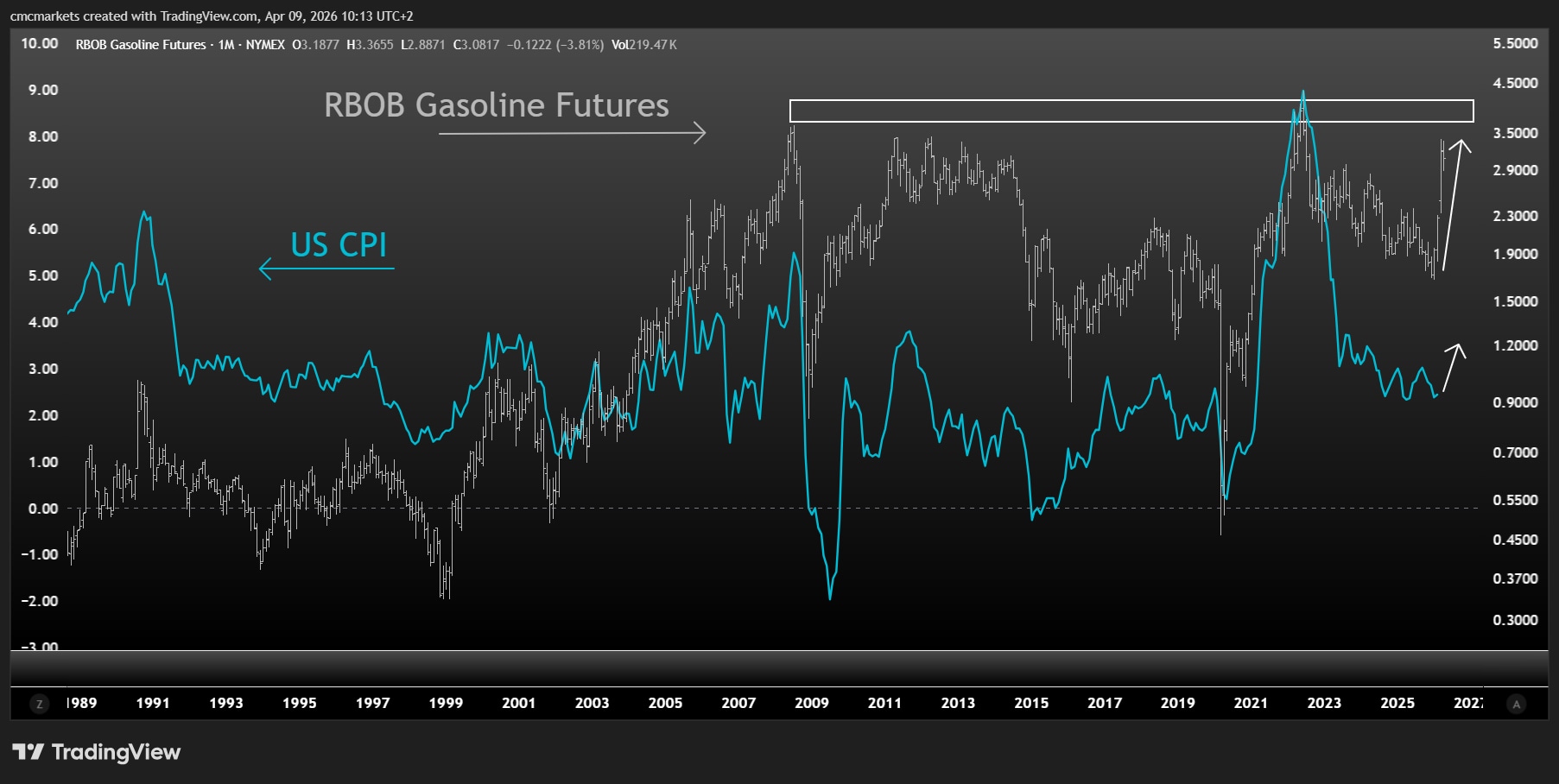

According to Trading Economics consensus data, inflation is expected to rise, with a larger move in the headline rate than in the core rate. Headline CPI is seen rising from 2.4% to 3.3% year on year, while core CPI is expected to increase from 2.5% to 2.7%. The rise in energy prices, led by RBOB gasoline futures, has fed through clearly into business surveys and inflation-expectation measures.

RBOB gasoline futures with US CPI, chart extracted from TradingView on 9 April 2026.

Fed funds still point to stability

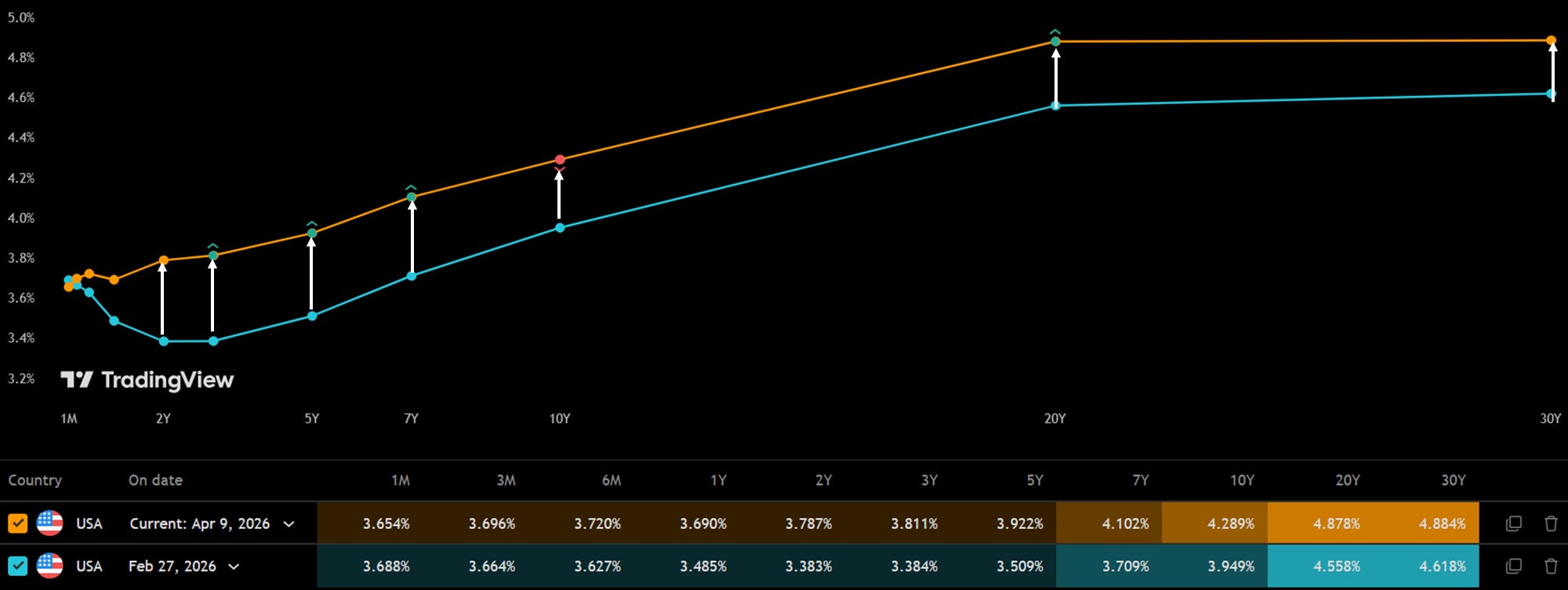

The key question is whether inflation may continue to rise and whether that move may spill over more meaningfully into core prices. On that front, the Cleveland Fed's real-time model suggests core inflation may remain broadly stuck around 2.6%, even if headline CPI continues to rise and may move above 3.5%.

If those estimates prove accurate, it would suggest second-round effects remain contained, which may be positive for the US Federal Reserve. Despite the recent steepening in the rates curve, Fed funds markets still imply no rate rise is needed, with the policy rate seen holding around 3.75% over the next year.

US interest-rate curve on 27 February versus 9 April, chart extracted from TradingView on 9 April 2026.

Liquidity stress is doing part of the Fed's job

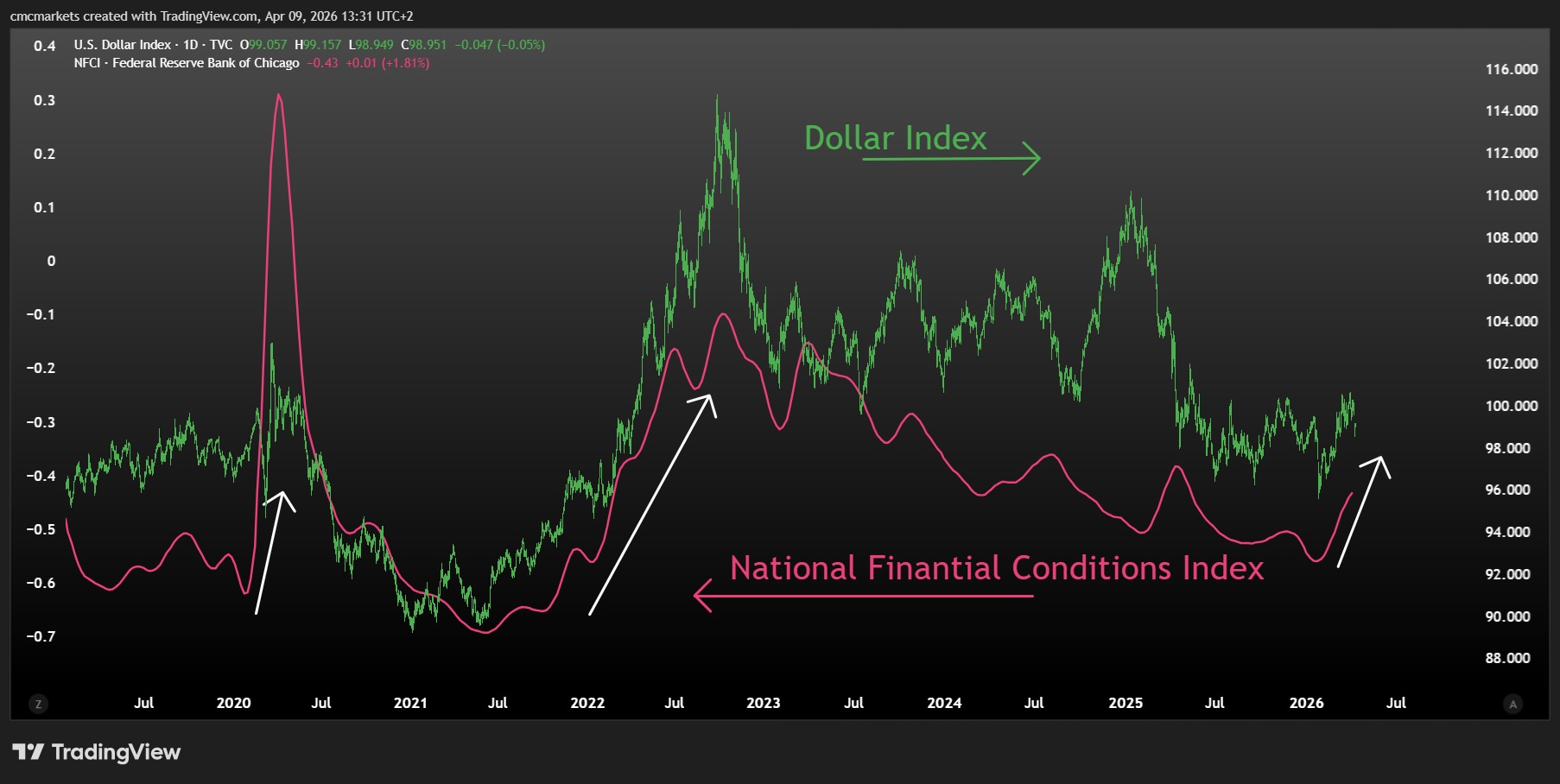

Even if the rise in inflation proves limited, yields remain elevated because of a higher risk premium linked to the fiscal deficit and geopolitical tension. That rise in yields has also come alongside wider credit spreads and higher credit default swaps.

At the same time, the search for liquidity to absorb the energy shock is pushing yields higher. The H.4.1 reports show declines in foreign custody holdings, while auction demand has weakened. The result is a larger accumulation of paper among primary dealers, especially in Treasury bills, and continued upward pressure on yields.

This backdrop is tightening financial conditions in a more passive way. The Chicago Fed National Financial Conditions Index, still around -0.43, already points to rising stress and leverage risk. In practice, the market is doing part of the Fed's job.

CPI may be the short-term catalyst

Liquidity stress is shifting flows away from equities and into debt. The S&P 500 faces that environment with demanding valuations and earnings season approaching, while the USD is regaining appeal as a defensive asset in a world of high yields and tighter financial conditions.

That leaves Friday's inflation report as the near-term catalyst. A headline and core reading above expectations may increase downside pressure on equities and upward pressure on yields and the USD. A high headline print with more contained core inflation may be less disruptive. A downside surprise, by contrast, may help ease financial conditions and support a more orderly liquidity backdrop.

US dollar index with the Chicago Fed National Financial Conditions Index, chart extracted from TradingView on 9 April 2026.

CPI (M-2:30 PM): Inflation ceiling, but no rate cuts until Powell leaves the Fed?

US CPI for DEC25 (M-14:30h) is high-impact data. Inflation might be forming a ceiling; however, the Fed may not spend ammunition or lower interest rates while the cycle and labor market hold up.

The S&P 500 relies on favorable CPI data: asymmetric risk with negative surprise

U.S. CPI (F-14:30 h) influences the Fed's next interest rate decision. The market is complacent and expects 3 consecutive rate cuts. A negative surprise would catch it off guard.

War pushes inflation, deficit and rates higher: CPI and 10-year note auction in focus

The war in Iran is affecting the interest rate curve and adding inflationary pressure through higher oil prices. Markets are now focused on the US Consumer Price Index (CPI) release, and the 10-year Treasury note auction as key indicators for interest rate expectations.