Tuesday's catalysts: ZEW, US consumer data and Warsh may test the S&P 500 at record highs

Tuesday's calendar brings a concentrated run of market catalysts, from the ZEW survey and US retail sales to Kevin Warsh's Senate appearance. With the DAX close to resistance and the S&P 500 at record highs, markets may face a meaningful test of confidence and breadth.

Market Analyst

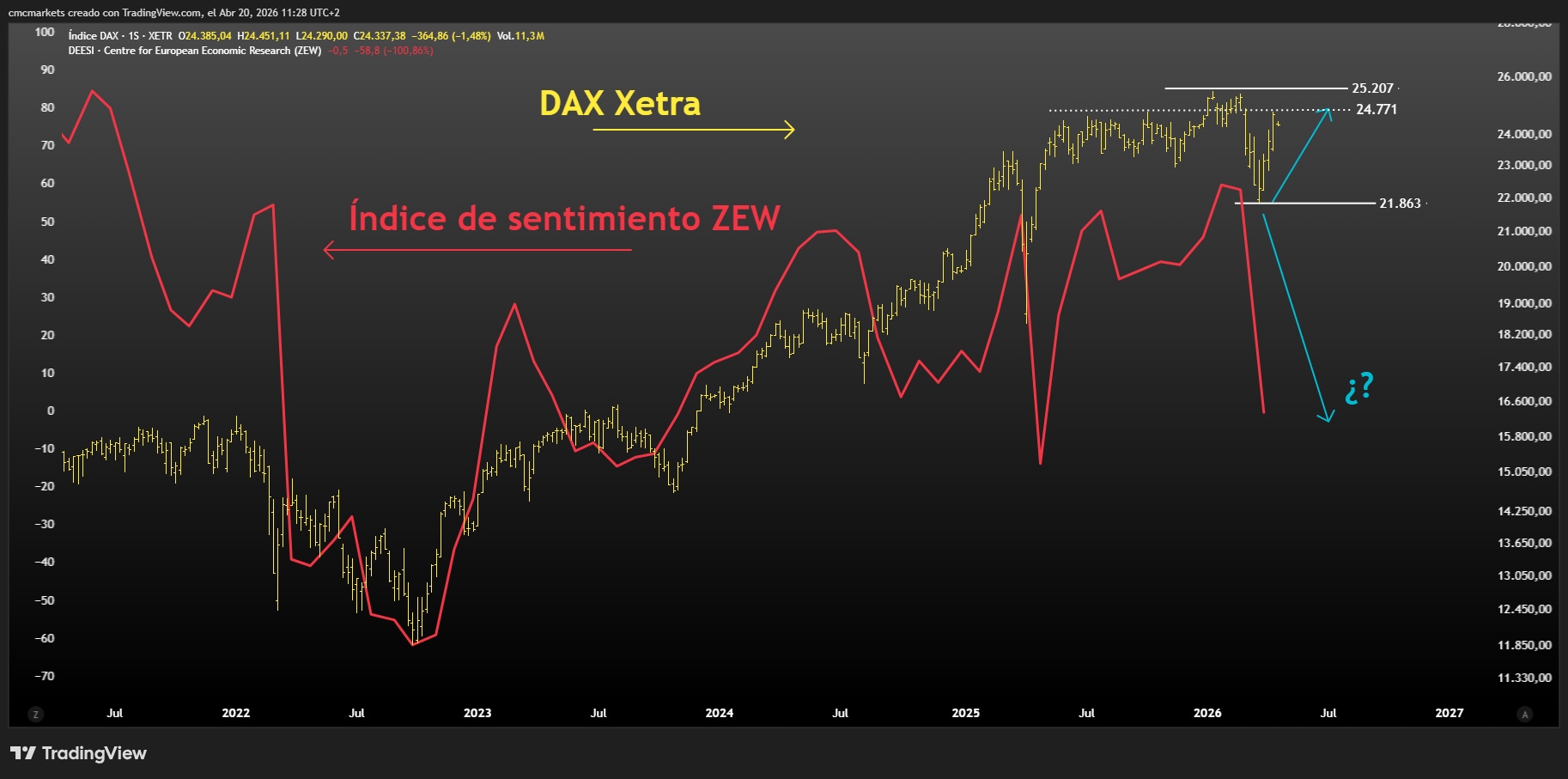

ZEW may deepen the gap between soft data and the DAX

In the second month of the Middle East conflict, the focus is on whether soft data continues to deteriorate. The Sentix survey already pointed to a broad weakening in sentiment, and consensus expects the ZEW survey to fall further to -10.3 in the eurozone and -10 in Germany, levels last seen during the peak of trade-war tension in April last year. If that deterioration is confirmed, it would widen the gap with a DAX that remains close to record highs and key resistance around 24,771 to 25,207. A positive surprise could give the index some support ahead of Thursday's PMIs and Friday's ifo survey.

Source: TradingView, 20 April 2026

US retail sales may show a weaker consumer backdrop

Consensus expects US retail sales to rise by 0.4% month on month despite the war in Iran and the sharp fall in the University of Michigan consumer-confidence reading. On an annual basis, markets expect growth of 2.4%, one of the weakest readings in recent years and below the pace of CPI. That points to a consumer who is paying more but buying less, a sign that purchasing power is fading. Retail sales are the key gauge of consumer spending, which makes up 68% of GDP and feeds directly into next week's personal-consumption data. Both defensive and cyclical consumer sectors are already losing momentum and have underperformed on a relative basis over recent quarters.

Source: TradingView, 20 April 2026

Warsh's Senate appearance could reshape Fed expectations

At 16:00 CET, Kevin Warsh is due to appear before the Senate Banking Committee as a candidate to chair the Federal Reserve. He is expected to use his opening statement to set out his case for the role and his views on the Fed's core mandates, balance-sheet policy and institutional independence. Markets will then watch the questioning closely, especially comments from Republican senator Thom Tillis, who has threatened to block Warsh's nomination until the Department of Justice concludes its investigation into Jerome Powell's 2025 testimony. That procedural risk adds another layer of political uncertainty at a time when committee vote margins are already very tight. Investors will also want to hear how firmly Warsh defends his preference for a lower-profile, less interventionist Fed. He argues that long-run inflation should trend lower as productivity gains from technologies such as AI reduce costs, allowing structurally lower interest rates. At the same time, he supports an aggressive reduction in the Fed's balance sheet through quantitative tightening.

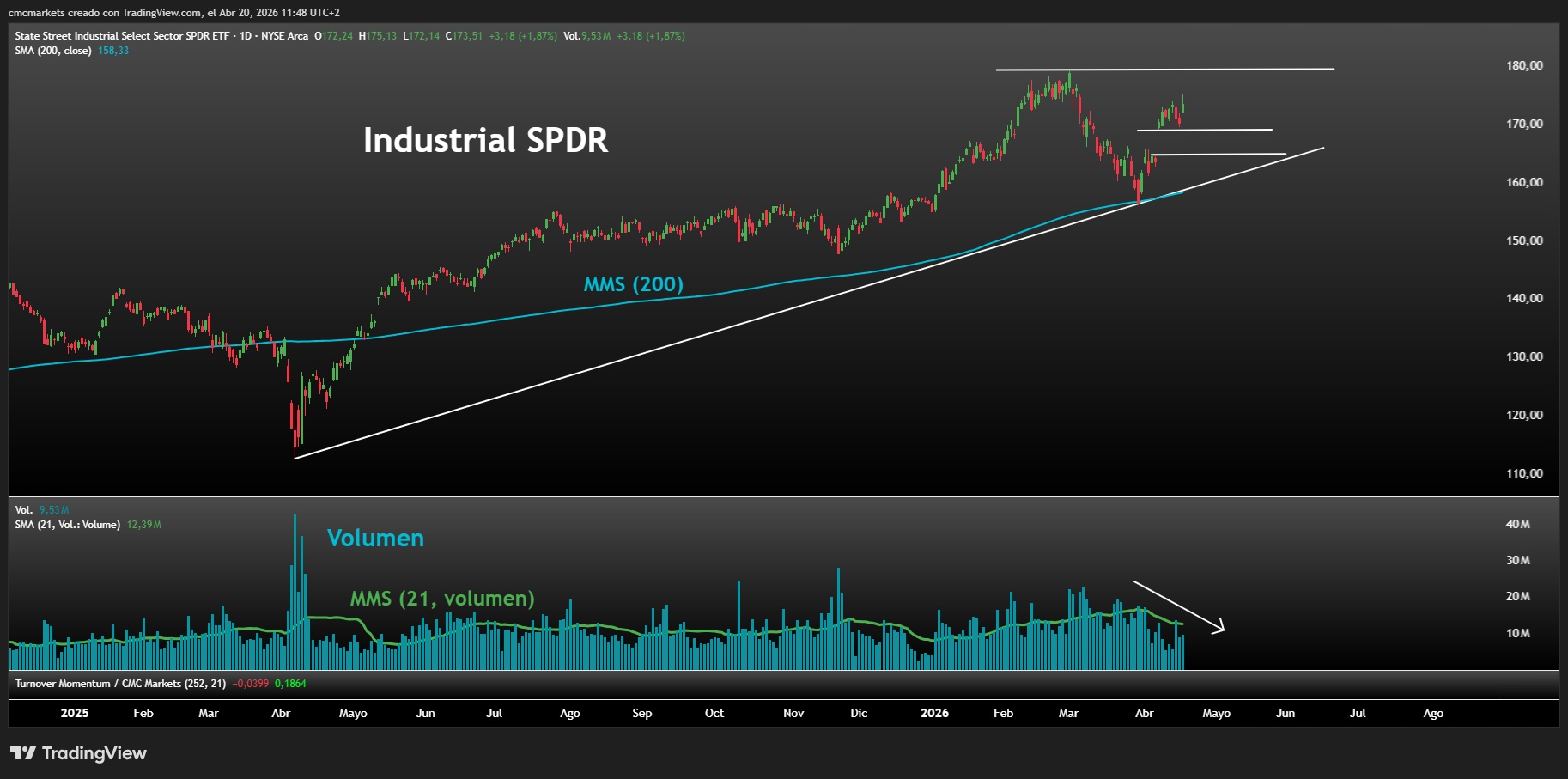

Defence and industrials face an earnings test

The industrial sector has regained traction on the back of geopolitics and the push for strategic autonomy, with the ISM manufacturing index settling back into expansion territory after years of contraction. Defence has led that move, and two major names, RTX and GE Aerospace, report tomorrow. Valuations remain demanding, with price/earnings multiples close to 40 times, while the recovery in the sector from its 200-day moving average is showing a pronounced divergence with volume. That leaves the sector vulnerable if results fail to justify the optimism.

Source: TradingView, 20 April 2026

S&P 500 Q1 results season starts with optimism, rich valuations and asymmetric risk

The Q1 earnings season is starting with high expectations for the S&P 500, led by financials and closely watched semiconductor names such as ASML and TSMC. With valuations still demanding and macro momentum slowing, the risk to equities may be more skewed to disappointment than upside surprise.

S&P 500 hits a record high, but this was no ordinary rally

S&P 500 closed at a fresh record on 15 April after an 11-session 10.7% surge that ranks among the strongest such runs since 1957. The rally appears to have drawn support from easing geopolitical risk, short-covering and CTA buying, with better earnings expectations helping the breakout hold.