April may still matter for equities

April has traditionally been one of the friendliest months of the year for equity investors, but 2026 may prove less forgiving. Seasonal support remains in place, yet persistent inflation, uncertainty over interest rates and rising energy costs may make this year's pattern harder to trust.

CMC Markets Poland

Why April has tended to support equities

In financial markets, April has long been viewed as one of the more supportive months for equities. Historical data suggests the S&P 500 has often delivered stronger average gains in this period than in many other months, helped in part by tax-related capital flows and dividend reinvestment.

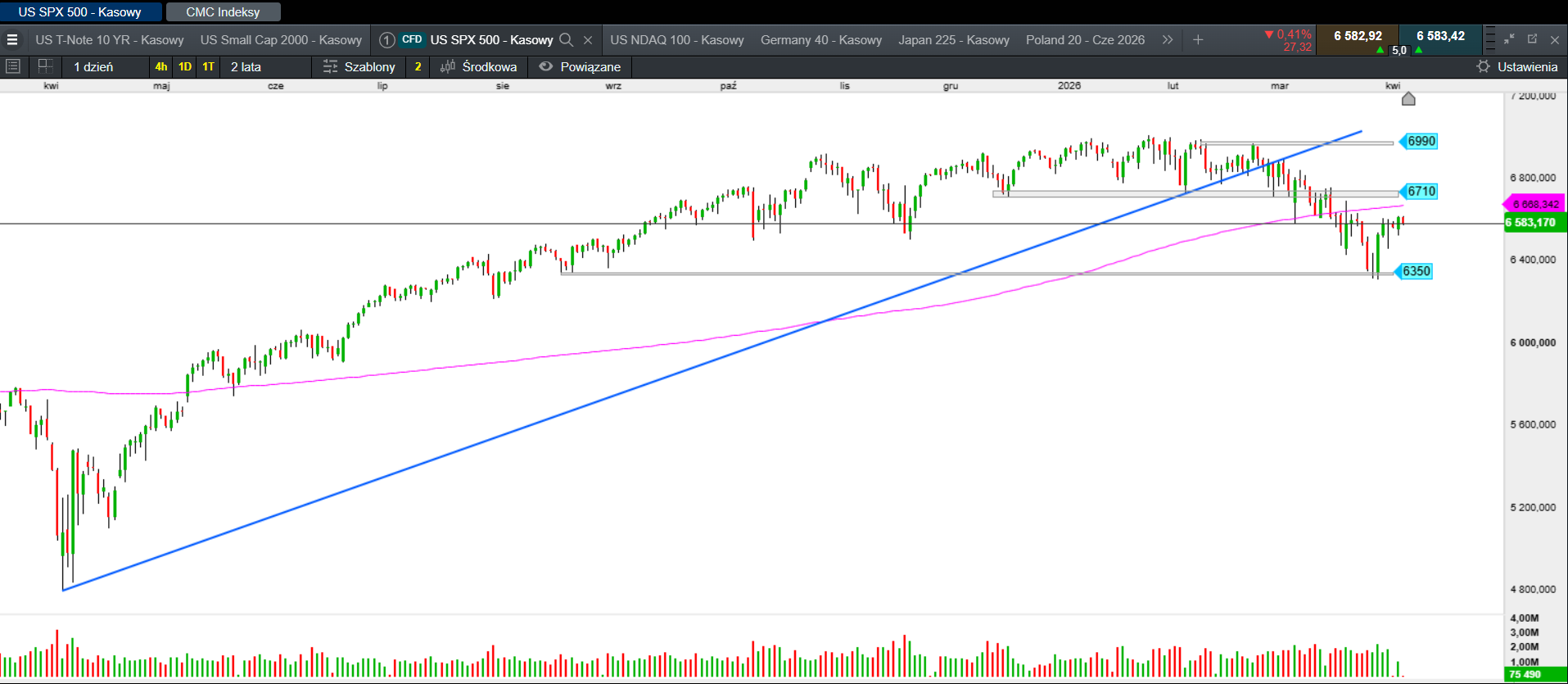

US SPX 500, daily

Sources: CMC Markets, Daniel Kostecki.

Why 2026 may be different

This year, that historical pattern may be tested more severely. Uncertainty around US Federal Reserve policy remains elevated, with policymakers still facing persistent inflation and limited room to ease monetary policy quickly.

A second risk is the approaching quarterly earnings season. Investors may become more cautious if high equity valuations are not matched by company results, which could increase the risk of a sharper correction.

Energy and geopolitics may still weigh on sentiment

A third source of pressure is the geopolitical backdrop and higher energy prices. Rising energy costs may keep inflation under pressure and make it harder for central banks to shift policy in a more supportive direction.

It is also worth noting that April marks the end of the period often associated with stronger seasonality for equities. That may encourage some investors to lock in gains early under the familiar 'sell in May and go away' approach.

Historical strength is not a guarantee

Analysts continue to stress that April's historical strength is not a guarantee of similar performance this year. With volatility still elevated and several macro risks overlapping, the month may prove to be a tougher test for equities than investors have become used to.

Dangerous pullback in S&P 500 and Nasdaq 100: will FOMO and TACO trade return?

S&P 500 and Nasdaq 100 perform a pullback to previous resistance levels. Divergences, overbought conditions, lack of breadth, and VIX approaching 20% may negate FOMO and the TACO trade. Read the analysis

Trump and Bessent under pressure as weak Treasury demand weighs on the S&P 500

Demand for US Treasuries is weakening despite higher yields, draining liquidity from equities and leaving Donald Trump and Scott Bessent with less room for manoeuvre. With 10-year yields near 4.50%, pressure on the S&P 500 may intensify if bond auctions fail to reassure the market.