Day trading tax UK: complete guide to HMRC rules & rates

Do You Pay Tax on Day Trading in the UK?

Yes, you typically pay tax on day trading profits in the UK. HMRC treats day trading gains as either capital gains or income, depending on your trading frequency, intent and whether trading constitutes your primary source of income. According to HMRC’s Business Income Manual (BIM56800, updated July 2025), the distinction between investing and trading hinges on several factors including the frequency of transactions, the sophistication of trading activity and whether you’re conducting a “trade” in the legal sense.

The tax treatment varies significantly based on your classification. Occasional traders face capital gains tax (CGT) on profits above the annual exemption (up to £3,000 for 2024/25), while those deemed professional traders pay income tax and national insurance on all profits.

Your specific circumstances determine your tax obligations. Trading through ISAs provides tax-free gains up to annual contribution limits (£20,000 for 2024/25), while spread betting remains tax-free for non-professional traders under current regulations. However, these tax advantages come with significant risks, including potential total loss of invested capital.

Capital Gains Tax vs Income Tax for Day Trading

The distinction between CGT and income tax fundamentally shapes your day trading tax liability. CGT applies when HMRC classifies your activity as investing rather than trading as a business. Under CGT rules, you pay tax only on gains exceeding your annual allowance, with rates of 18% for basic-rate taxpayers and 24% for higher-rate taxpayers on financial assets.

Income tax applies when HMRC determines you’re conducting a trade. This classification triggers several tax implications.

HMRC applies the “badges of trade” test, established through case law and codified in BIM20205 (revised February 2024). The nine badges include the frequency of transactions, the period of ownership and whether you’re seeking to profit from asset appreciation or conducting systematic trading operations. Highly active traders may face increased scrutiny regarding their tax classification.

The High Court’s decision in Marson vs Morton (1986) remains the cornerstone for distinguishing investment from trading. The judgment established that while a single transaction rarely constitutes trading, repeated buying and selling with short holding periods indicates trading activity. Modern algorithmic and high-frequency trading strategies almost invariably fall within the trading category due to their systematic nature and transaction volume.

HMRC Day Trading Tax Rules and Classification

HMRC’s approach to classifying day traders follows established legal precedents and detailed guidance in their manuals. The fundamental question revolves around whether your activities constitute a “trade” within the meaning of the Income Tax Act 2007. HMRC doesn’t provide a statutory definition of trading, instead relying on case law principles developed over decades.

The badges of trade serve as HMRC’s primary assessment tool. According to HMRC’s Capital Gains Manual (CG15145, updated September 2025), key indicators of trading include:

Subject matter of the transaction - Securities purchased for resale rather than investment income

Length of ownership period - Positions held for hours or days rather than months

Frequency of transactions - Daily or weekly trading patterns

Supplementary work - Using analysis tools, developing trading systems or modifying positions

Circumstances leading to realisation - Selling based on price targets rather than life events

Motive - Seeking profits from price movements rather than dividends or interest

HMRC examines your entire pattern of behaviour rather than isolated transactions. Their Compliance Handbook (CH231100, March 2024) indicates that day traders using sophisticated strategies, maintaining detailed trading plans or deriving their primary income from trading face presumption of conducting a trade. The burden of proof shifts to the taxpayer to demonstrate investment intent.

Professional qualification doesn’t automatically determine tax status, but HMRC considers relevant expertise. Former investment bankers or fund managers face heightened scrutiny when claiming investor status. Conversely, maintaining separate investment portfolios alongside day trading activities can support arguments for mixed tax treatment, though each account requires individual assessment.

UK Day Trading Tax Rates and Allowances

The 2024/25 tax year brings specific rates and allowances affecting day traders. Your tax liability depends on your classification and total income across all sources.

Current income tax rates for trading income are as follows:

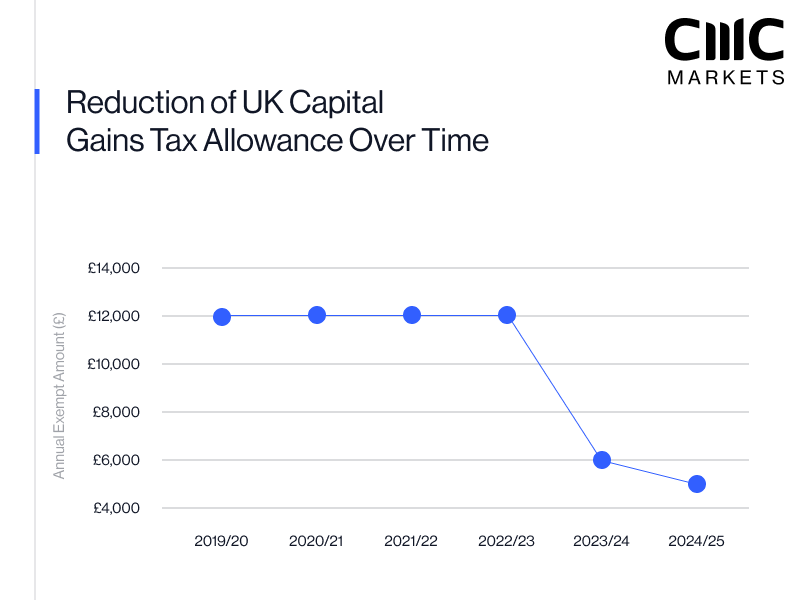

Capital gains rates remain lower, offering significant savings for those maintaining investor status. The CGT annual exempt amount decreased from £6,000 to £3,000 in April 2024 and remains at this level for 2024/25.

A trading allowance of £1,000 applies to miscellaneous income, potentially covering small-scale trading profits without formal reporting requirements. However, day traders rarely qualify given typical transaction volumes and profit levels.

Pension contributions provide tax relief at your marginal rate, effectively reducing taxable trading profits. Annual allowance stands at £60,000 for 2024/25, with potential carry-forward of unused allowances from previous three years. High-earning traders face tapered annual allowance above £260,000 adjusted income.

Day Trading Tax Calculator and Examples

Calculating your day trading tax requires understanding your classification and applying appropriate rates. Let’s examine realistic scenarios based on HMRC’s published examples and current tax rates.

Example 1: Part-time trader with capital gains treatment. Sarah executes 150 trades annually while maintaining full-time employment. Her trading profits for 2024/25:

Total gains: £28,000

Allowable losses: £4,000

Net gain: £24,000

Less CGT allowance: £3,000

Taxable gain: £21,000

Tax due (20% higher rate): £4,200

Example 2: Full-time day trader taxed as trading income. Marcus left employment to trade full-time, executing 50+ trades weekly:

Gross trading profit: £65,000

Allowable expenses: £3,500 (platform fees, data subscriptions, home office)

Net profit: £61,500

Income tax calculation:

Personal allowance: £12,570 @ 0% = £0

Basic rate: £37,700 @ 20% = £7,540

Higher rate: £11,230 @ 40% = £4,492

National Insurance Class 4:

£48,930 @ 6% = £2,936

£11,230 @ 2% = £225

Total tax due: £15,193

The contrast demonstrates why classification matters. Sarah’s effective tax rate equals 15%, while Marcus pays 24.7% despite similar gross profits. These calculations exclude potential pension contributions or other allowable deductions that could reduce liability.

HMRC’s Self Assessment tool includes specific sections for trading income. Box 15 on SA103F captures self-employment profits from financial trading, whilst SA108 addresses capital gains. Misclassification triggers penalties plus interest on underpaid tax.

CFD Day Trading Tax Implications

Contract for difference (CFD) trading carries distinct tax implications under UK law. HMRC treats CFD profits as capital gains for non-professional traders, but the leveraged nature and typical trading patterns often trigger reclassification as trading income. The Financial Conduct Authority has highlighted that 75–80% of CFD accounts lose money, highlighting the risk inherent in these instruments.

CFD trades don’t qualify for stamp duty exemption benefits since no underlying asset transfer occurs. However, this saving pales against potential tax liabilities. Professional CFD traders face income tax on all profits, with no ability to offset losses against capital gains from other investments. HMRC’s guidance (CFM13000, updated July 2025) specifically addresses derivative taxation.

Key CFD tax considerations include:

Losses can only offset against future CFD gains when treated as capital.

Financing charges aren’t deductible unless trading as a business.

Foreign currency CFDs may trigger additional reporting requirements.

Corporate traders face different rules under loan relationship regulations.

The complexity increases with international CFDs. UK residents trading US index CFDs through foreign brokers must navigate both UK tax obligations and potential US withholding tax on certain instruments. Double taxation treaties provide relief, but proper documentation is essential. HMRC’s International Manual (INTM167140, updated September 2025) details treaty benefits and claiming procedures.

Spread Betting Day Trading Tax Rules

Spread betting occupies a unique position in UK tax law. For non-professional gamblers, profits remain tax-free under current legislation. This exemption stems from spread betting’s classification as gambling rather than investing. However, HMRC scrutinises claims carefully, particularly for high-volume traders.

The tax-free status applies only when spread betting doesn’t constitute your trade. HMRC’s position, clarified in BIM22020 (updated July 2025), states that systematic spread betting as a primary income source becomes taxable. The leading case, Down v Compston (1937), established that professional gambling constitutes a trade when conducted systematically for profit.

Warning signs that might trigger professional classification:

Spread betting provides your main income source.

You market spread betting services or education.

Your employer connects to financial markets.

You use sophisticated analysis resembling professional trading.

Transaction volumes exceed typical recreational levels.

Tax-free status comes with disadvantages. Losses cannot offset against other income or capital gains. No tax relief applies to trading-related expenses. ISA and pension contribution benefits don’t extend to spread betting accounts.

Despite tax advantages, spread betting carries substantial risks. Leverage magnifies losses beyond initial deposits. Tax savings prove meaningless when facing net losses. Consider overall profitability and risk tolerance rather than focusing solely on tax benefits.

Record Keeping Requirements for Day Trading

Meticulous record-keeping forms the foundation of compliant day trading taxation. HMRC requires records supporting your tax position for at least five years after the submission deadline (six years for trading income). Digital records satisfy requirements provided they’re complete, accurate and accessible. According to HMRC’s record-keeping guidance, inadequate records can trigger penalties up to £3,000 per tax year.

Essential records for day traders include:

Contract notes for every transaction

Bank statements showing deposits and withdrawals

Trading account statements from all brokers

Dividend and interest statements

Spreadsheets or software tracking profit/loss calculations

Documentation supporting expense claims

Correspondence regarding corporate actions

Modern trading platforms provide downloadable transaction histories, but these rarely include all necessary information. Brokers’ tax statements often reflect their jurisdiction’s requirements rather than UK obligations. You must reconcile platform data with UK tax rules, adjusting for corporate actions, currency conversions and timing differences.

HMRC’s Connect system cross-references data from multiple sources, including common reporting standard information from overseas brokers. Discrepancies trigger compliance checks. The Requirement to Correct legislation imposes strict liability for offshore non-compliance, with penalties up to 200% of tax due. Maintaining contemporaneous records proves crucial when responding to HMRC enquiries, potentially years after trading occurred.

How to Report Day Trading Income to HMRC

Reporting requirements depend on your classification and income levels. Trading income requires registration for Self Assessment if you exceed £1,000 profit or need to claim allowable expenses. For 2024/25, the capital gains reporting proceeds threshold is £50,000, and the annual exempt amount is £3,000.

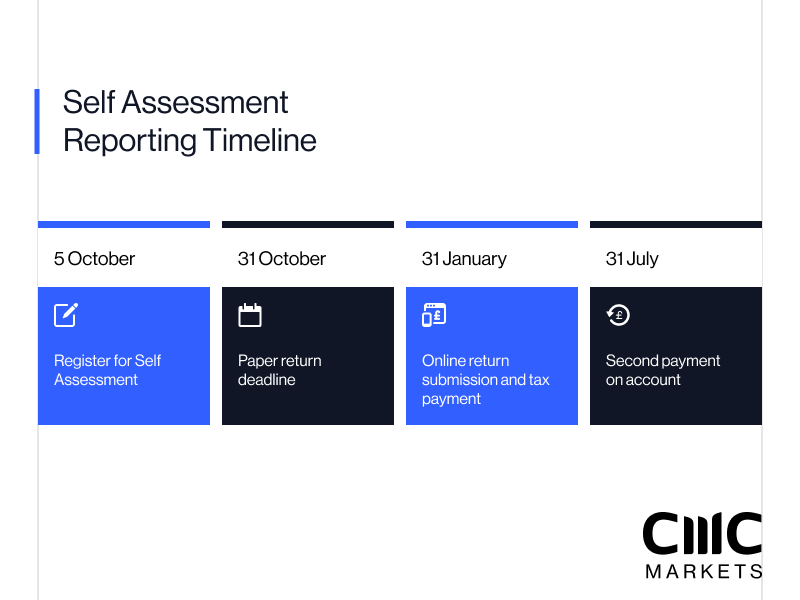

The Self Assessment process follows established deadlines:

5 October: Register for Self Assessment if newly required

31 October: Paper return deadline

31 January: Online submission and payment deadline

31 July: Second payment on account due

Trading income appears on supplementary pages SA103F (self-employment) or SA102 (employment pages for employee share schemes). Include gross receipts, allowable expenses and net profit. HMRC’s guidance notes (SA103F Notes) provide specific instructions for financial trading businesses.

Capital gains reporting uses form SA108, with summary figures on page CG1 and detailed computations on supplementary sheets. Recent simplification allows real-time reporting through HMRC’s online service, potentially beneficial for active traders managing numerous transactions. The service calculates gains automatically when provided with acquisition costs and disposal proceeds.

Payment on account requirements affect traders with tax bills exceeding £1,000. You’ll pay advance payments towards next year’s liability, based on previous year’s tax. This creates cash flow challenges for traders experiencing volatile profits. Time payment negotiations prove difficult given HMRC’s view that traders should anticipate tax obligations.

Professional Day Trading Tax Implications

Professional trader status fundamentally alters your tax position. Beyond higher tax rates, professional classification triggers national insurance obligations, different loss relief rules and potential VAT considerations. HMRC’s Business Income Manual (BIM56860, updated July 2025) outlines factors indicating professional status.

Professional traders can claim extensive business expenses:

Home office costs (proportional to business use)

Professional subscriptions and training

Data feeds and analytical software

Computer equipment and technology

Professional indemnity insurance

Accountancy and tax advice fees

These deductions offset trading profits but require careful documentation. HMRC challenges aggressive expense claims, particularly for dual-purpose items. The wholly and exclusively rule prevents claiming personal expenses, even with partial business use. Recent First-tier Tribunal decisions emphasise the need for clear business purpose.

Trading through a limited company offers potential tax advantages but introduces complexity. Corporation tax at 25% may beat personal tax rates. However, extracting profits triggers additional tax through dividends or salary. The dividend tax rates for 2024/25 are 8.75% (basic), 33.75% (higher) and 39.35% (additional rate), eroding corporate tax benefits.

National insurance planning becomes crucial for professional traders. Class 2 contributions (£3.50 weekly for 2025/26) are mandatory above the small profits threshold. Class 4 contributions apply to profits exceeding £12,570. Consider incorporation when combined tax and national insurance exceeds potential corporate tax plus extraction costs. Individual circumstances determine optimal structure.

Day Trading Losses and Tax Relief

Trading losses offer valuable tax relief when properly utilised. The treatment depends on your classification and the type of loss incurred. Capital losses carry forward indefinitely against future capital gains but cannot offset income. Trading losses provide more flexible relief options, potentially generating tax refunds.

Capital loss relief follows statutory rules:

Current year losses must offset current year gains

Excess losses carry forward automatically

No ability to carry back losses (except on death)

Losses on qualifying trading company shares may qualify for income relief

Trading loss relief under Section 64 Income Tax Act 2007 permits offsetting against:

Other income in the same tax year

Other income in the preceding tax year

Future profits from the same trade

Trading loss relief remains an important mechanism in UK tax law for reducing taxable income. However, loss relief caps at £50,000 or 25% of adjusted total income (whichever is higher), preventing excessive claims. Anti-avoidance provisions restrict relief for non-commercial trades or tax-motivated arrangements.

Documentation requirements for loss claims exceed profit reporting. HMRC scrutinises loss-making trades, questioning commercial viability and profit motives. The “reasonable expectation of profit” test examines whether competent traders would anticipate profits given market conditions and strategy employed. Consistent losses over multiple years trigger enhanced scrutiny.

Terminal loss relief allows carrying back losses from the final year of trading against profits from previous three years. This proves valuable when ceasing unprofitable trading activities. Claims must be made within four years of the tax year when trading ceased. Professional advice often proves worthwhile given the complexity and value of terminal relief claims.

Common Day Trading Tax Mistakes to Avoid

Day traders frequently make costly tax errors that trigger penalties and interest charges. The table below includes several common mistakes that can lead to enquiries and additional assessments. Understanding these pitfalls helps maintain compliance and minimise tax risk.

Misunderstanding tax classification tops the list. Traders assume occasional profitability maintains investor status despite executing hundreds of trades annually. HMRC examines substance over form — calling yourself an investor while operating like a professional trader won’t prevent reclassification. The tax difference often exceeds tens of thousands of pounds annually.

Inadequate record-keeping creates problems years later:

Failing to register for Self Assessment represents a fundamental error. Trading profits require registration even below tax thresholds if expenses need claiming. Late registration penalties start at £100, rising to £1,600 for delays exceeding 12 months. HMRC charges interest on late tax payments from the due date, currently at 7.75% annually as of September 2025.

Offshore broker complications catch many traders unprepared. Using non-UK platforms doesn’t eliminate UK tax obligations. The Common Reporting Standard ensures HMRC receives information about overseas accounts. Failing to declare offshore income triggers Failure to Correct penalties up to 200% of tax due. Claiming foreign tax credits requires understanding relevant double taxation agreements and completion of appropriate relief claims.

For informational purposes only. Not investment advice. Investments involve risk.

Ready to get started?

Disclaimer: CMC Markets is an execution-only service provider. The material (whether or not it states any opinions) is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.