Out of the money options explained: what UK traders need to know

What are out of the money options?

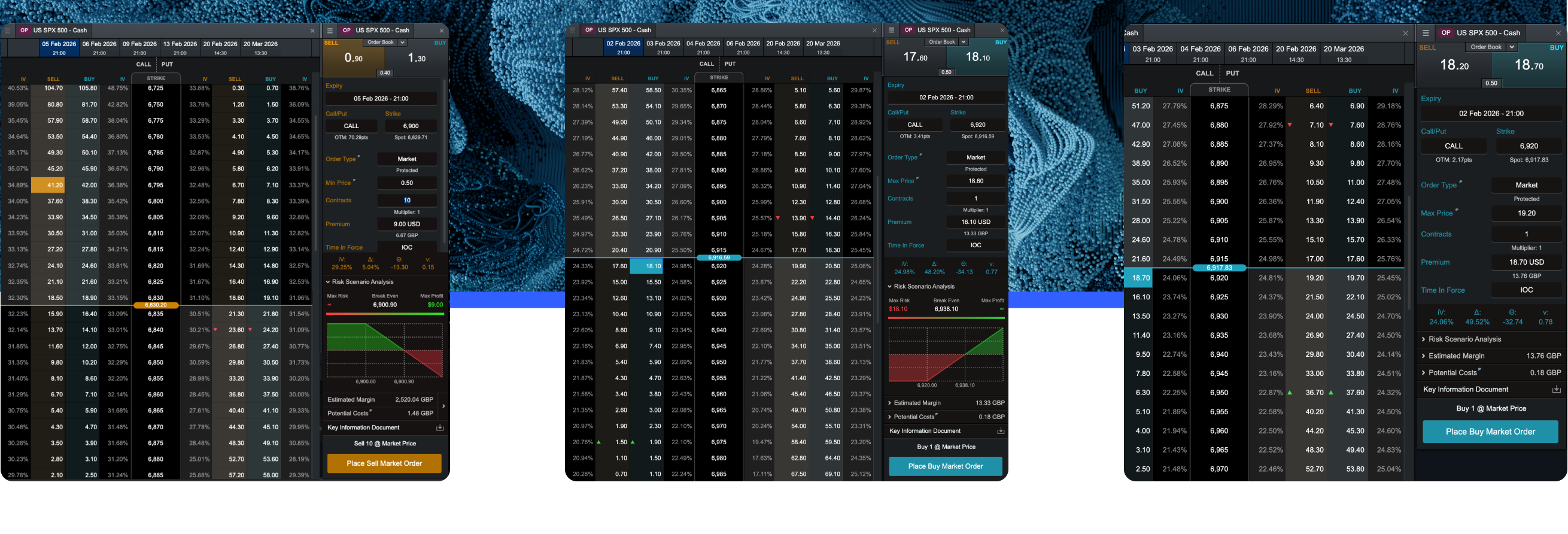

An out of the money option is one that would have no value if exercised immediately. It lacks what traders call intrinsic value. The option still has a price in the market, but that price reflects only the possibility that the underlying asset might move favourably before expiration.

For a call option, being out of the money means the current market price of the underlying asset sits below the strike price. You would not exercise your right to buy at a higher price than you could obtain in the open market.

For a put option, being out of the money means the current market price sits above the strike price. Exercising your right to sell at a lower price than the market offers makes no economic sense.

The price you pay for an out of the money option is called the premium. This premium consists entirely of time value, sometimes called extrinsic value. Time value reflects the probability that the option could become profitable before it expires.

Understanding option moneyness

Moneyness describes the relationship between an option’s strike price and the current price of the underlying asset. The moneyness of options falls into three categories.

This framework of moneyness options helps traders assess potential outcomes. An option’s moneyness changes constantly as the underlying asset price moves. An out of the money option can become in the money if the price moves sufficiently, and vice versa.

In the money vs out of the money: key differences

The distinction between in-the-money and out-of-the-money options shapes how traders approach pricing, risk and strategy selection.

The table below summarises the core differences.

In-the-money options cost more because they already hold intrinsic value. If you own an ITM call and the underlying price stays flat, you still have something of value at expiration.

Out of the money stock options, by contrast, need the underlying to move in your favour before they gain intrinsic value. The lower price reflects this additional hurdle. Many OTM options expire worthless because the required move never happens.

This trade-off between cost and probability sits at the heart of options trading. Neither state is inherently better. Each suits different objectives and risk tolerances.

How out of the money call options work

An out of the money call option gives you the right, but not the obligation, to buy the underlying asset at the strike price. When the strike exceeds the current market price, exercising immediately would mean paying more than you could on the open market.

Consider a hypothetical stock trading at £95. A call option with a strike price of £100 is out of the money. The strike sits £5 above where you could simply buy shares directly.

The option still has value because time remains until expiration. If the stock rises to £105 before the option expires, that call becomes in the money. The intrinsic value would be £5, representing the difference between market price and strike.

For the call buyer to profit, the stock must rise enough to cover the premium paid. If you paid £2 for the call, you need the stock above £102 at expiration to make money.

Key points about out of the money call options:

You pay a lower premium than ITM or ATM calls.

The underlying must rise above the strike before intrinsic value appears.

Time decay works against you more aggressively.

The entire premium can be lost if the option expires worthless.

How out of the money put options work

An out of the money put option gives you the right to sell the underlying asset at the strike price. When the strike sits below the current market price, exercising would mean selling for less than you could obtain in the open market.

Imagine a share trading at £100. A put option with a strike price of £95 is out of the money. Selling at £95 when the market offers £100 makes no sense.

However, if the share price falls to £90, the put becomes in the money with £5 of intrinsic value. You could exercise your right to sell at £95, which is £5 better than the market price.

For the put buyer to profit overall, the underlying must fall enough that the intrinsic value exceeds the premium paid. If you paid £1.50 for the put, you need the stock below £93.50 at expiration.

OTM puts are sometimes purchased as a form of portfolio insurance, though this use carries its own costs and limitations.

Why do traders use OTM options?

Despite the higher probability of total loss, out of the money options attract traders for several reasons. Understanding these motivations helps clarify both the appeal and the dangers.

Potential benefits of OTM options

Lower capital outlay represents the primary attraction. OTM options cost less than their in-the-money equivalents. A trader with a strong directional view might prefer paying £1 for an OTM option rather than £5 for an ITM option.

This lower cost also means limited maximum loss. You cannot lose more than the premium paid when buying options. This applies to buying options only; selling (writing) options can expose you to losses greater than the premium, potentially unlimited.

Some traders also use OTM options as part of multi-leg strategies. These combinations involve buying and selling different options simultaneously. The lower cost of OTM options can reduce the overall outlay for certain spread positions.

Risks and limitations of OTM options

The risks of OTM options deserve equal attention. Many traders lose money on these instruments, and the challenges are structural rather than merely incidental.

High failure rate stands as the primary concern. OTM options frequently expire worthless. The underlying must move in the correct direction by a sufficient amount within a limited timeframe. All three conditions must align for profit.

Time decay accelerates as expiration approaches. An OTM option loses time value every day. This erosion is not linear. The final weeks and days before expiration see the sharpest declines in premium, all else being equal.

The leverage effect cuts both ways. While gains can be substantial in percentage terms when an OTM option moves into the money, the probability of this happening is lower than with ITM options.

Key risks to consider:

Complete loss of premium is common.

Time works against the option buyer.

Volatility must be sufficient to move the underlying.

Liquidity can be poor for deep OTM strikes.

Examples of out of the money options

These examples illustrate how OTM options work in practice. The figures are hypothetical and for educational purposes only. Examples are simplified and exclude transaction costs, spreads and taxes.

Example 1: OTM Call Option

A UK trader believes Company X shares, currently trading at £80, will rise over the next month. They purchase a call option with a strike price of £85, expiring in 30 days, for a premium of £1.20 per share.

Scenario A: The shares rise to £90 before expiration. The option is now £5 in the money. Subtracting the £1.20 premium, the net gain is £3.80 per share.

Scenario B: The shares remain at £80. The option expires worthless. The trader loses the entire £1.20 premium per share.

Scenario C: The shares rise to £85 exactly. The option is at the money. The intrinsic value is zero, and the trader loses the full premium.

Example 2: OTM Put Option

A trader holds shares in Company Y, currently at £50, and worries about a short-term decline. They buy a put option with a strike of £45, paying £0.80 per share.

If the shares fall to £40, the put is £5 in the money. After deducting the £0.80 premium, the net value is £4.20 per share.

If the shares stay above £45, the put expires worthless. The £0.80 premium is lost entirely.

Key considerations before trading OTM options

Before trading OTM options, several practical factors warrant attention.

Understand time decay thoroughly. Every day that passes reduces the value of your option, assuming the underlying price stays flat. This effect intensifies near expiration.

Assess probability realistically. The lower price of OTM options reflects lower probability of success. Markets are not offering cheap options by mistake. The pricing reflects collective expectations about likely outcomes.

Consider liquidity. Deep OTM options may have wide bid-ask spreads, increasing trading costs. Getting in and out of positions can be more expensive than headline premiums suggest.

Never commit more than you can afford to lose entirely. OTM options should represent a small portion of any portfolio, if used at all. The speculative nature of these instruments makes sizing decisions critical.

Important questions to ask yourself:

Do I understand how much the underlying needs to move for profit?

Can I afford to lose the entire premium?

How will time decay affect my position?

Is there sufficient liquidity at my chosen strike?

Have I considered alternative approaches with different risk profiles?

Summary

Out of the money options are options that would have no value if exercised immediately. Calls are OTM when the market price sits below the strike. Puts are OTM when the market price sits above the strike.

The appeal of OTM options lies in their lower cost and limited maximum loss for buyers. The danger lies in their high probability of expiring worthless. Time decay erodes value daily, and the underlying must move favourably by a meaningful amount within a set timeframe.

Understanding moneyness helps you evaluate options accurately. In-the-money and out-of-the-money options suit different purposes and carry different risk profiles. Neither is inherently superior.

Options trading requires careful study and realistic expectations. Before trading any options, ensure you understand the mechanics, the risks and how they fit within your overall financial situation. Consider seeking guidance from a qualified financial adviser if you are unsure whether options are appropriate for you.

Options are complex financial instruments that carry significant risk. Many traders lose money when trading options, and you should not trade with money you cannot afford to lose.

Ready to get started?