Monzo IPO: what investors need to know

UK digital bank Monzo is gearing up for what could be one of Britain’s most closely watched fintech IPOs in years. Discover the key details on Monzo’s potential listing, including the expected date, valuation, financials, risks, and how you could get involved.

What does Monzo do?

Monzo is a UK-based digital challenger bank that delivers current accounts, savings, lending and investment products through its mobile app. Founded in 2015 by former Starling Bank employees Tom Blomfield, Jonas Huckestein, Jason Bates, Paul Rippon and Gary Dolman, the company now serves over 12 million personal customers and 600,000 business customers, making it the seventh-largest bank in Britain by customer numbers (Monzo Annual Report, June 2025).

Monzo’s core products and services

Personal current accounts – fee-free everyday banking with instant spending notifications, budgeting pots, and salary sorting.

Business banking – accounts for sole traders, freelancers and limited companies with invoicing, tax pots, expense management and team cards.

Savings and investments – instant-access and fixed-term savings accounts, plus a stocks and shares product built in partnership with BlackRock.

Lending products – personal loans, overdrafts, and Monzo Flex, a buy-now-pay-later feature allowing purchases to be spread over instalments.

Premium plans – Monzo Extra, Perks and Max subscription tiers offering benefits such as virtual cards, cashback, credit insights and higher interest on savings.

How does Monzo make its money?

Monzo operates as a fully digital bank, delivering financial services through its smartphone app rather than physical branches. Unlike traditional high-street lenders, it relies on a mobile-first, technology-driven model to acquire and retain customers at scale.

Monzo’s revenue comes from several streams. Here is a breakdown of the main ones:

Net interest income

Interchange and transaction fees

Subscription plans

Lending products

Business accounts

Net interest income – the largest revenue driver. Monzo earns the spread between interest paid on customer deposits and the returns generated from lending those deposits and investing them. Interest income reached £861m in FY2025 (Monzo Annual Report, June 2025).

Interchange and transaction fees – Monzo collects a small fee from merchants each time a customer makes a card payment. As spending volumes grow, so does this income line.

Subscription plans – over one million customers now pay for Monzo Extra, Perks or Max, generating £75m in the latest financial year, up 50% year-on-year (Monzo Annual Report, June 2025). This provides predictable, recurring income.

Lending products – Monzo earns interest and fees on personal loans, overdrafts and Flex repayments. Its loan book expanded 35% in FY2025 (Sacra, June 2025).

Business accounts – with over 600,000 business customers, Monzo generates income from monthly fees, payment processing charges and business-focused tools such as tax filing and invoicing.

What is Monzo’s IPO date?

Monzo has not set an official IPO date. Earlier reports suggested a potential listing in the first half of 2026, with Morgan Stanley appointed to lead initial investor meetings (Sky News, May 2025). However, the timeline has become less certain following a leadership change in late 2025.

Former CEO TS Anil stepped down in February 2026 after reported disagreements with the board over listing timing (Financial Times, December 2025). Anil favoured an earlier IPO, while directors preferred more time to expand internationally and grow the company’s valuation. Incoming CEO Diana Layfield, a former Google and Standard Chartered executive, is expected to take the helm in February 2026, subject to regulatory approval. Monzo has signalled it will not rush into a listing and is prioritising sustained growth over meeting a fixed deadline. Investors should note that IPO timelines are inherently uncertain and can shift depending on market conditions, regulatory processes and internal strategy.

How can investors get exposure?

What could Monzo be worth at IPO?

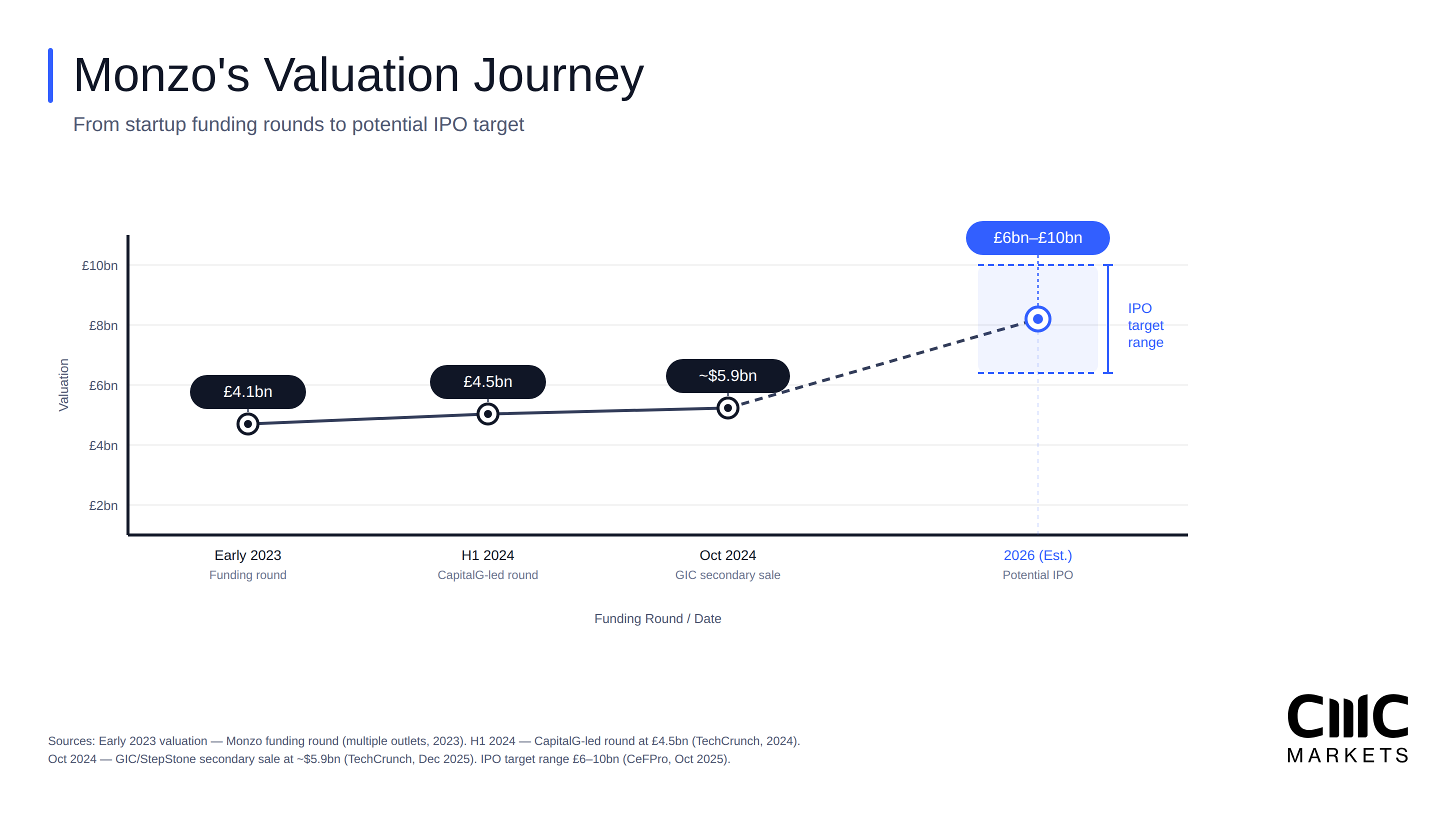

Monzo's valuation has climbed steadily through successive funding rounds, with banking sources suggesting a potential IPO valuation of between £6bn and £10bn.

Monzo’s valuation has climbed steadily. In early 2023, it raised funding at a £4.1bn valuation. A further round in H1 2024, led by CapitalG (Alphabet’s investment arm), set the figure at £4.5bn. Then in October 2024, a secondary share sale backed by Singapore’s GIC sovereign wealth fund and StepStone Group valued the business at roughly $5.9bn (TechCrunch, December 2025).

Banking sources suggest an IPO could value Monzo at between £6bn and £10bn, depending on market conditions and investor appetite (CeFPro, October 2025). Analysts typically arrive at these figures by comparing Monzo to listed fintech peers such as Brazil’s Nubank, factoring in customer growth and revenue multiples. Valuations can shift quickly, though. A downturn in public market sentiment, weaker-than-expected financials or competing listings from rivals like Revolut could all push the figure lower. Equally, strong demand could drive it higher.

How are Monzo’s financials?

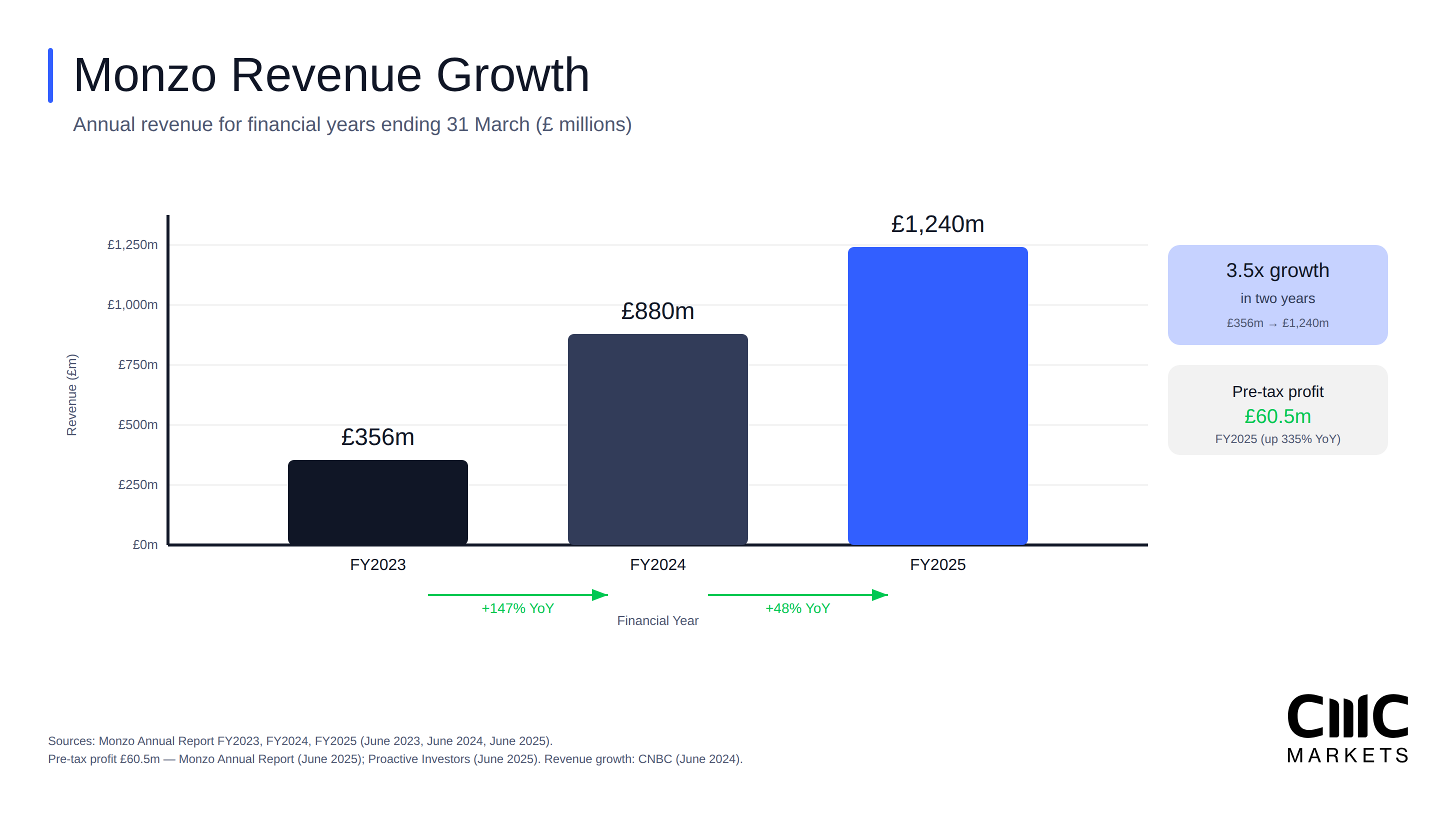

Monzo's revenue has grown 3.5x in two years, reaching £1.24bn in FY2025 alongside its first significant pre-tax profit of £60.5m.

Monzo’s revenue growth has been striking. For the year ending 31 March 2025, the bank reported revenue of £1.24bn, a 48% increase on the prior year. Customer deposits rose 48% to £16.6bn, and 2.2 million new personal customers joined during the period. Adjusted pre-tax profit surged 719% to £113.9m, while reported pre-tax profit reached £60.5m, up 335% year-on-year (Monzo Annual Report, June 2025; Proactive Investors, June 2025).

This followed Monzo’s first-ever full year of profit in FY2024, when it swung from a £116m loss to a £15.4m pre-tax profit on revenue of £880m (CNBC, June 2024). IPO investors will typically want to see consistent revenue growth, a clear path to sustained profitability, manageable cost-to-income ratios and a diversified revenue base. Monzo ticks several of those boxes, but it is worth noting that much of its recent profitability has been supported by a higher interest-rate environment. If rates fall, margins could come under pressure.

Why are investors interested in this IPO?

Monzo has grown from a prepaid-card startup to the UK’s seventh-largest bank by customer numbers in a decade. One in five British adults now holds a Monzo account, and the coral debit card has become one of the most recognised symbols in UK fintech. That kind of brand loyalty is difficult to replicate and gives Monzo a strong foundation for cross-selling savings, investments, pensions and insurance products.

The business has also attracted heavyweight institutional backing. Key investors include CapitalG (Alphabet), GIC (Singapore’s sovereign wealth fund), Tencent, Accel, General Catalyst and Hedosophia. The appointment of Diana Layfield, who brings experience from both Google and Standard Chartered, signals an ambition to scale beyond the UK into Europe and the US.

Beyond the company itself, a successful Monzo listing could revitalise the London IPO market, which has seen a decline in major tech flotations in recent years. That broader significance may attract institutional interest from funds looking to support UK-listed growth companies. However, investors should weigh this enthusiasm against the risks outlined below, as past growth does not guarantee future returns.

What are the risks and challenges?

Regulatory scrutiny remains a material concern. In July 2025, the FCA fined Monzo £21.1m for inadequate anti-money laundering controls between 2018 and 2020 (FCA, July 2025). While the bank has since completed a remediation programme and the FCA lifted its restrictions in February 2025, the fine highlights the challenge of scaling compliance alongside rapid customer growth. Further regulatory tightening across the fintech sector could increase costs.

Competition is fierce. Revolut, valued at up to $75bn, is preparing its own IPO and has secured a UK banking licence. Starling Bank is profitable and may also list. Traditional lenders such as Lloyds, Barclays and NatWest continue to invest heavily in their digital offerings. If several fintech IPOs launch at the same time, they could compete for the same pool of investor capital, potentially dampening demand.

Monzo’s profitability is also closely tied to the interest-rate cycle. A significant portion of its revenue comes from net interest income, which benefits from higher rates. If rates decline, lending margins may narrow. The recent CEO transition adds another layer of uncertainty. Leadership changes ahead of a major listing can unsettle investors, particularly when, as reported by the Financial Times (December 2025), the departure followed boardroom disagreements over strategy.

Who are Monzo’s competitors?

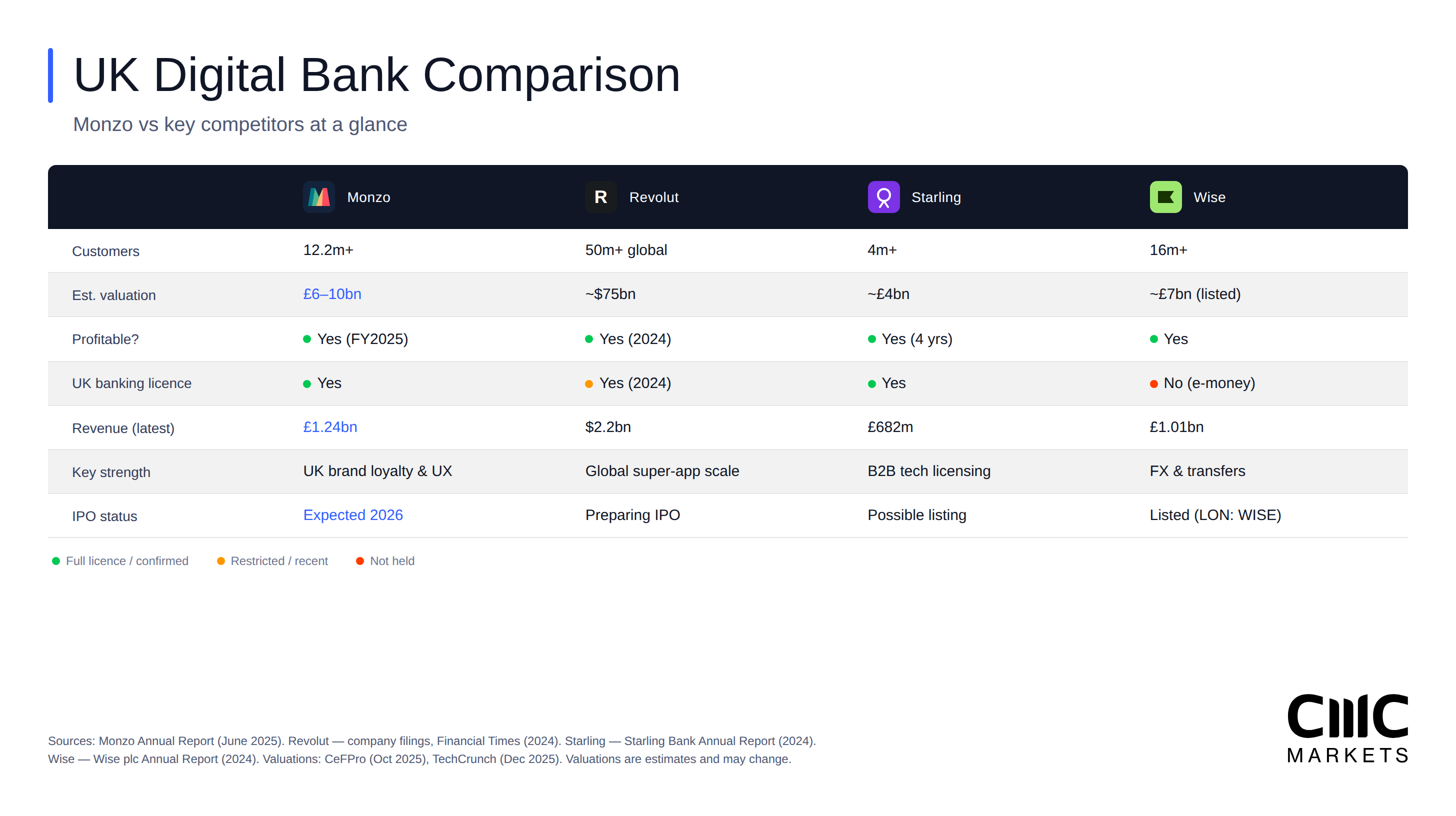

Monzo faces stiff competition from Revolut, Starling and Wise, but differentiates through UK brand loyalty and a broadening product range.

The UK digital banking market has become highly competitive. Monzo’s main rivals include:

Revolut – the largest UK-founded neobank by valuation, serving over 50 million global customers. Revolut offers a broader super-app model spanning crypto trading, stock investing and international transfers. It secured a UK banking licence (restricted with a mobilisation phase) in 2024 and is preparing its own IPO.

Starling Bank – a UK digital bank with over four million accounts and four consecutive years of profitability. Its Engine by Starling division licenses core banking technology to other institutions, creating an additional revenue stream.

Traditional banks – Lloyds [LLOY], Barclays [BARC], NatWest [NWG] and HSBC [HSBA] are all investing in mobile banking and digital-first products to retain customers attracted by challenger bank features.

Wise [WISE] – focused on international money transfers and multi-currency accounts, Wise competes with Monzo for customers who send money abroad.

Monzo differentiates itself through its user experience, community engagement and a product roadmap that has expanded from basic banking into savings, investments, pensions, insurance and tax tools. You can trade or invest in listed competitors such as Wise, Lloyds, Barclays, NatWest and HSBC with us while you wait for the Monzo IPO.

Risk warning: Spread bets and CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when spread betting and/or trading CFDs with this provider. You should consider whether you understand how spread bets, CFDs, OTC options or any of our other products work and whether you can afford to take the high risk of losing your money.

Disclaimer: CMC Markets is an execution-only service provider. The material (whether or not it states any opinions) is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.