CFD tax UK: how HMRC taxes CFD trading profits and losses

Key points at a glance

How are CFDs taxed in the UK?

For the majority of retail traders, profits from CFD trading fall under the Capital Gains Tax rather than Income Tax. HMRC treats CFDs as chargeable assets, meaning any gain you make when closing a position is potentially taxable.

This classification matters because CGT has different rates and allowances compared to Income Tax. The distinction depends largely on how HMRC views your trading activity, which we cover in more detail later.

Capital gains tax on CFD profits

When you close a CFD position at a profit, that gain becomes part of your total chargeable gains for the tax year. HMRC aggregates all your capital gains from various sources, including shares, property (excluding your main home) and derivatives like CFDs.

The key word is “net” gains. You calculate your total gains, subtract your total allowable losses and then apply your annual allowance before working out what you owe.

The annual CGT allowance

Every individual in the UK receives an annual CGT allowance, sometimes called the Annual Exempt Amount. For the 2024/25 tax year, this allowance stands at £3,000. Only gains exceeding this threshold attract CGT.

This represents a significant reduction from previous years. The allowance was £12,300 as recently as 2022/23, then dropped to £6,000 in 2023/24, before reaching the current £3,000 level. This lower threshold means more traders now find themselves with reportable gains.

CGT rates for CFD traders

If your taxable income plus gains straddles the basic rate threshold, you may pay both rates on different portions of your gains. The mechanics can get complicated, which is one reason many traders seek professional guidance.

One advantage CFDs hold over traditional share dealing is the absence of stamp duty. When you buy physical shares in UK companies, you typically pay 0.5% stamp duty reserve tax. Since CFDs are derivative contracts rather than actual share ownership, this charge does not apply.

CFD trading vs spread betting: tax differences

The question of the difference between spread betting and CFD taxation comes up frequently among UK traders. The two products share many characteristics but receive different tax treatment.

Why spread betting is treated differently

Spread betting profits are generally free from Capital Gains Tax for retail traders. HMRC classifies spread betting as gambling rather than investing, which places winnings outside the CGT regime. However, tax treatment isn’t guaranteed and depends on individual circumstances and HMRC’s view.

This distinction exists because spread betting originated in the bookmaking industry. You are technically betting on price movements rather than entering a contract for the difference in an asset’s value.

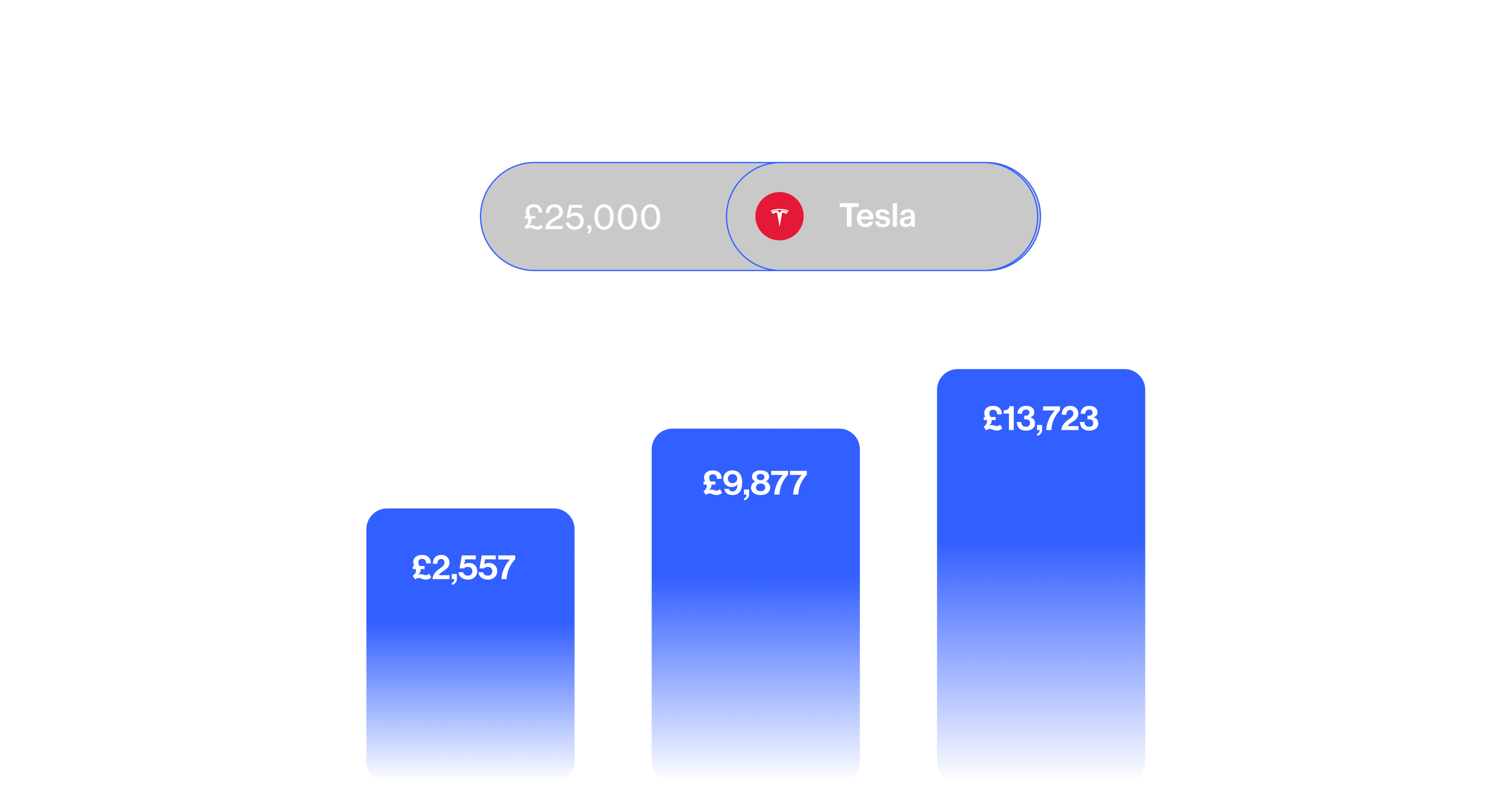

However, the tax treatment cuts both ways. Because spread betting losses are not considered capital losses, you cannot offset them against other gains. If you make £10,000 profit on share sales but lose £8,000 spread betting, you still owe CGT on the full £10,000 gain (less your allowance). With CFDs, that loss could potentially reduce your taxable gain.

Which approach is more appropriate?

Neither product is inherently superior. Your circumstances determine which might work better for you.

Traders who consistently generate profits may prefer spread betting’s tax treatment. Those who experience mixed results, with gains in some areas and losses in others, might benefit from the loss-offsetting available with CFDs.

That said, tax considerations should not be the primary driver of your product choice. The underlying economics, trading costs, available markets and your own risk tolerance matter more than tax efficiency. A tax-free loss is still a loss.

*Tax treatment depends on individual circumstances. Professional clients only. Capital at risk.

Calculating your CFD tax liability

Working out what you owe requires accurate records and straightforward arithmetic, though the volume of trades can make this time-consuming.

Working out gains and losses

For each CFD trade, your gain or loss equals the difference between your opening and closing position values, minus any directly attributable costs. These costs typically include:

Spread costs (built into opening/closing prices)

Commission charges (if your broker charges separately)

Overnight financing charges

Your broker should provide transaction records showing these figures. Many platforms offer annual statements specifically designed for tax reporting purposes.

Offsetting losses against gains

Losses on CFD trades can reduce your overall CGT liability. You deduct allowable losses from gains before applying your annual allowance.

If your losses exceed your gains in a given year, you can carry forward unused losses to set against future gains. There is no time limit on carrying forward capital losses, but you must report them to HMRC in the tax year they occur to preserve them.

Example scenario:

Reporting CFD profits to HMRC

UK tax on CFD trading requires active reporting. HMRC does not automatically calculate your liability for you.

Self assessment requirements

If your total taxable gains exceed the annual allowance, you must report them via Self Assessment. This applies even if you have losses that reduce your net position below the threshold, as HMRC needs to record those losses for future use.

The Self Assessment deadline is 31 January following the end of the tax year. For gains made between 6 April 2025 and 5 April 2026, you must file by 31 January 2027.

If you do not already file Self Assessment returns for other reasons (self-employment income, rental income, etc.), you will need to register for the service. Allow adequate time for this process, particularly if approaching the deadline.

Self Assessment reporting requirements can also depend on your total disposals/proceeds and whether you need to claim losses. Check HMRC guidance or a tax adviser for your situation.

Record-keeping obligations

HMRC requires you to keep records supporting your tax return for at least five years after the 31 January submission deadline. For CFD trading, this means retaining:

Contract notes or transaction confirmations

Monthly or annual statements from your broker

Records of deposits and withdrawals

Your own calculations showing how you arrived at your reported figures

Good record-keeping throughout the year makes the annual reporting process far less painful than reconstructing your trading history from memory.

When CFD trading may be classed as trading income

For most retail traders, CFD profits fall under CGT. However, HMRC may classify very active traders as conducting a trade, shifting gains into Income Tax territory.

This distinction matters because Income Tax rates (20%, 40%, 45%) can exceed CGT rates, and Income Tax has no equivalent to the CGT annual allowance. However, being classified as a trader also opens access to business expense deductions not available under CGT.

HMRC considers several factors when making this determination, sometimes called the “badges of trade”:

Frequency and volume of transactions

Level of organisation and sophistication

Whether trading represents your primary income source

The holding period of positions

Your stated intention when entering trades

No single factor is decisive. HMRC looks at the overall picture. A day trader executing hundreds of positions monthly with sophisticated systems faces higher scrutiny than someone making occasional trades.

For corporate entities trading CFDs, different rules apply entirely. The derivative contracts regime under Corporation Tax governs these activities, as outlined in HMRC’s Business Income Manual at BIM56900.

Important limitations and considerations

Several important caveats apply to everything discussed in this guide:

Tax law changes regularly. Rates, allowances and classifications can shift with each Budget or Finance Act. The figures quoted here reflect current rules but may not apply when you read this or when you file your return.

Individual circumstances vary enormously. Your residence status, domicile, other income sources and trading patterns all affect your tax position. Two people making identical CFD profits could face different tax outcomes.

HMRC has broad discretion. The boundary between CGT treatment and Income Tax treatment is not precisely defined. HMRC examines each case on its facts.

This guide cannot cover every scenario. Complex situations involving foreign brokers, non-UK residence, trust structures or corporate trading require specialist professional advice.

Platform tax summaries have limitations. While broker statements help, they may not align perfectly with HMRC requirements. The responsibility for accurate reporting rests with you, not your broker.

Summary

CFD trading profits in the UK are generally subject to Capital Gains Tax at rates of 18% or 24%, depending on your income level. The current annual CGT allowance of £3,000 means traders generating meaningful profits will likely have a tax liability to report.

The ability to offset CFD losses against gains provides some flexibility that spread betting does not offer, though spread betting’s general exemption from CGT remains attractive for consistently profitable traders.

Do you pay tax on CFD trading in the UK? For most retail traders, yes. The amount depends on your net gains, your allowance and your overall income. Accurate record-keeping and timely Self Assessment filing keep you on the right side of HMRC.

Whatever your trading approach, understanding the tax implications helps you make informed decisions. But remember: this content provides general educational information only. For guidance on your specific situation, speak with a qualified tax adviser or contact HMRC directly.

Disclaimer: CMC Markets is an execution-only service provider. The material (whether or not it states any opinions) is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.