Headline inflation may rise more sharply than core

US March CPI is due at 14:30 on Friday. It is a high-impact release that may generate immediate volatility across the dollar, equities and bonds.

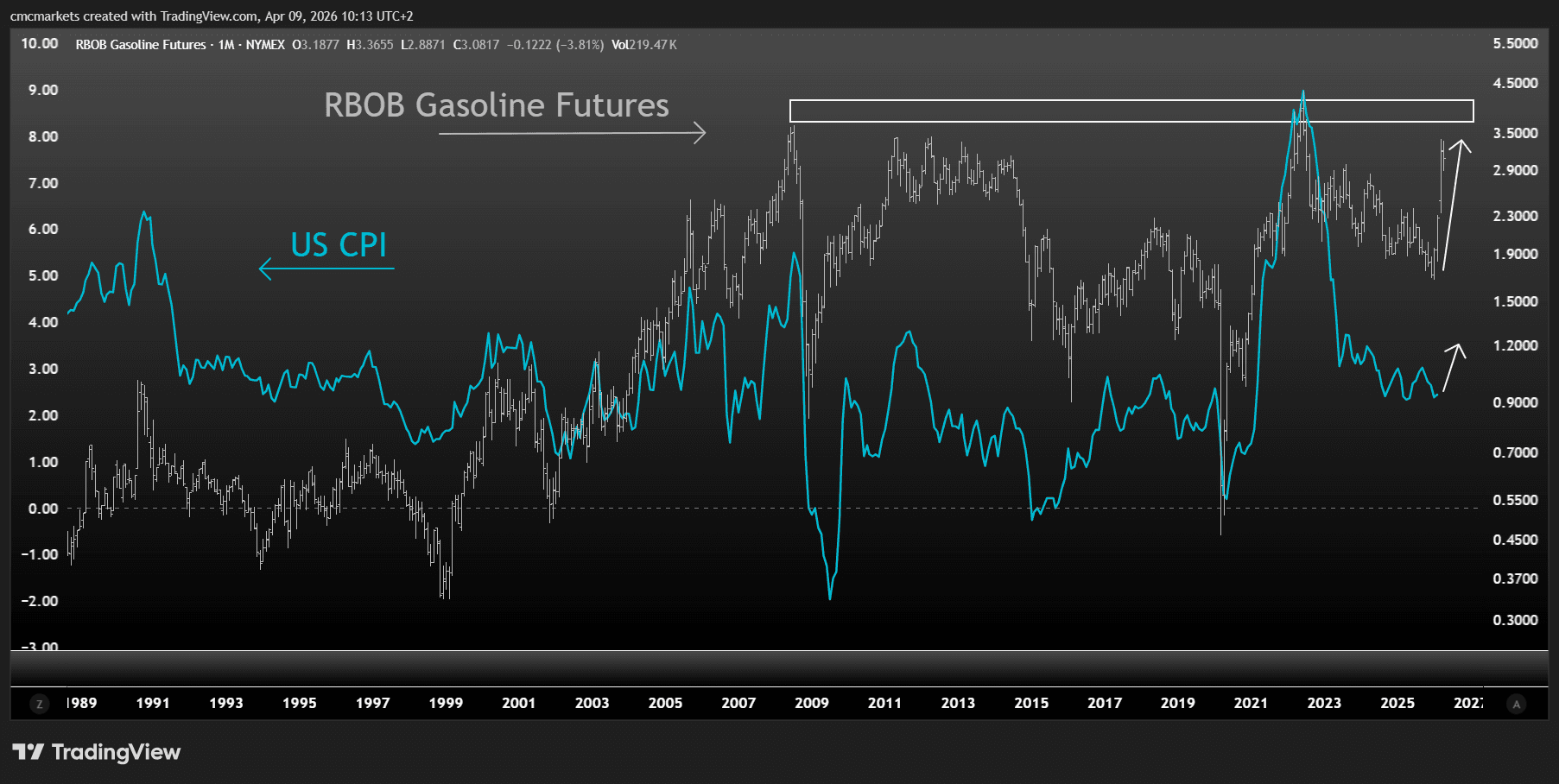

According to Trading Economics consensus data, inflation is expected to rise, with a larger move in the headline rate than in the core rate. Headline CPI is seen rising from 2.4% to 3.3% year on year, while core CPI is expected to increase from 2.5% to 2.7%. The rise in energy prices, led by RBOB gasoline futures, has fed through clearly into business surveys and inflation-expectation measures.

RBOB gasoline futures with US CPI, chart extracted from TradingView on 9 April 2026.

Fed funds still point to stability

The key question is whether inflation may continue to rise and whether that move may spill over more meaningfully into core prices. On that front, the Cleveland Fed's real-time model suggests core inflation may remain broadly stuck around 2.6%, even if headline CPI continues to rise and may move above 3.5%.

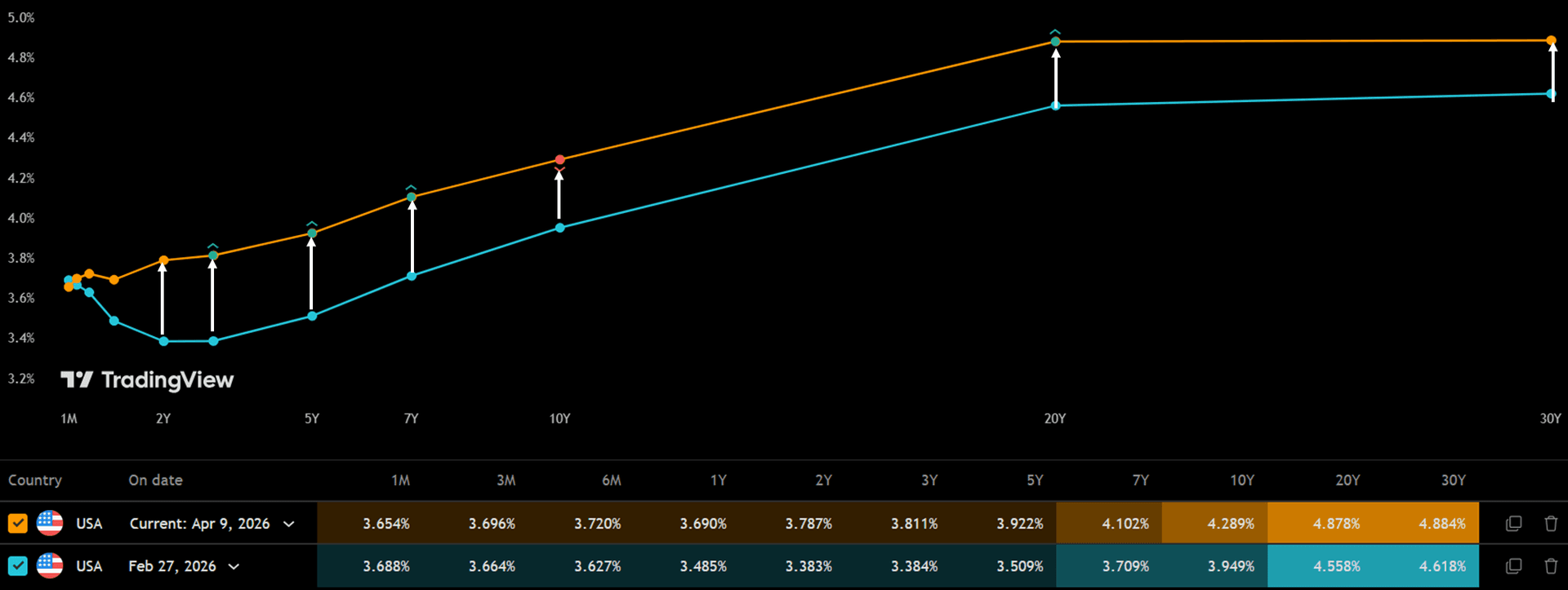

If those estimates prove accurate, it would suggest second-round effects remain contained, which may be positive for the US Federal Reserve. Despite the recent steepening in the rates curve, Fed funds markets still imply no rate rise is needed, with the policy rate seen holding around 3.75% over the next year.