Oil volatility has eased even as the geopolitical story stays unresolved

Brent and WTI have both moved into a broader consolidation phase after the most acute period of Middle East tension, and risk gauges tied to oil have also fallen back. The Spanish source argues that this reflects a market increasingly willing to assume that the worst-case supply disruption scenario is fading rather than intensifying.

That calmer pricing matters because it shapes how traders interpret every new headline around the Strait of Hormuz and regional shipping. If the market keeps treating the conflict as manageable, oil may stay contained for longer even if the political backdrop remains fragile.

The futures curve is already pricing in a gradual return to normality

The source highlights that Brent is still in backwardation, but the forward curve points to materially lower prices beyond the current year. That implies traders expect supply stress to ease over time rather than escalate into a more durable energy shock.

Those expectations broadly fit with official forecasts from the US Energy Information Administration, but they also leave less room for error if reality diverges from the path currently embedded in futures pricing. When the market prices normalisation early, even a small delay to that process can start to matter more.

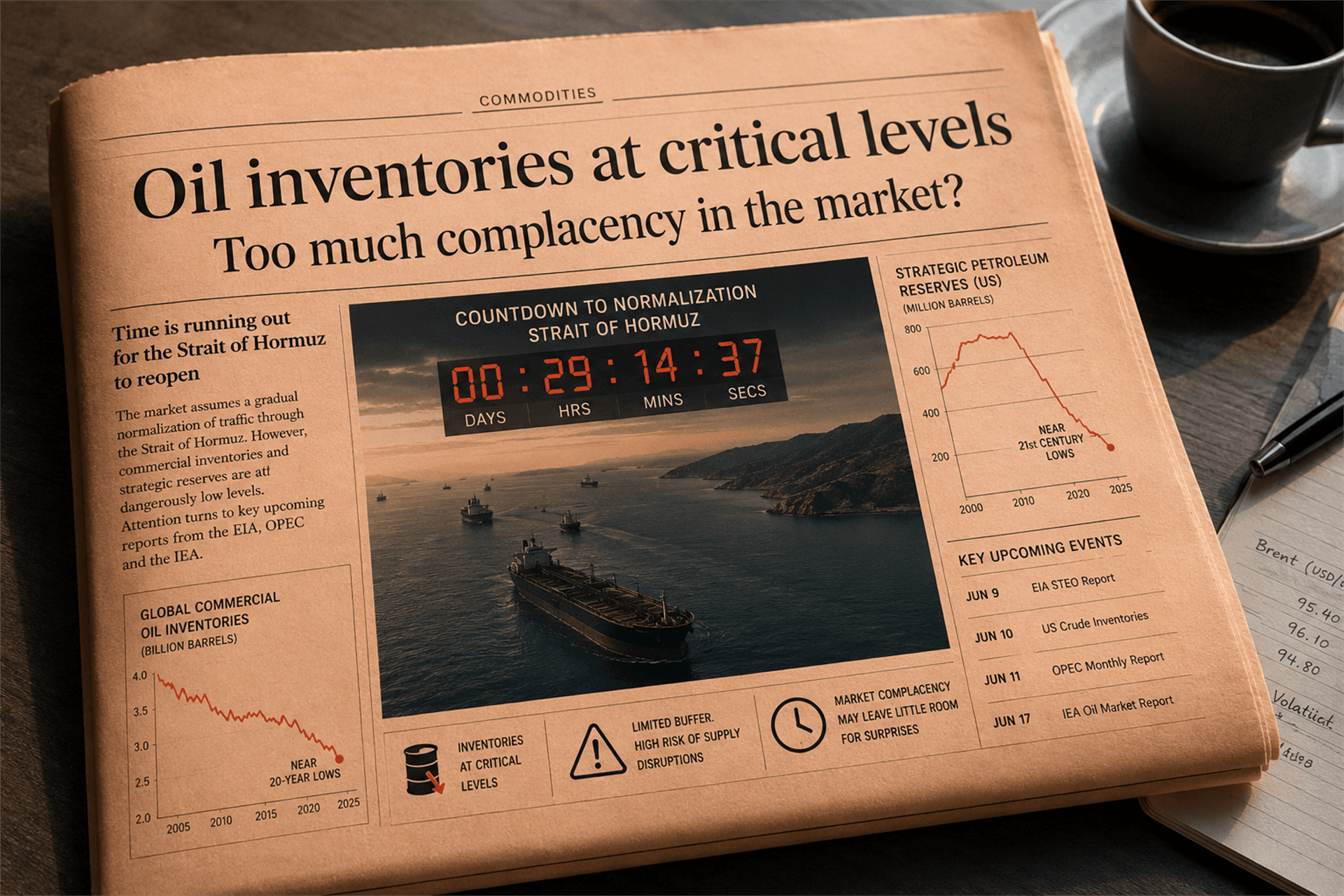

Inventories and strategic reserves still point to a thin safety buffer

This is where the Spanish piece becomes more cautious. Commercial oil inventories remain close to their lowest levels since 2004, while the US strategic petroleum reserve is still depressed after years of drawdowns. In practical terms, that means the physical market may have less protection against a fresh supply shock than current price action suggests.