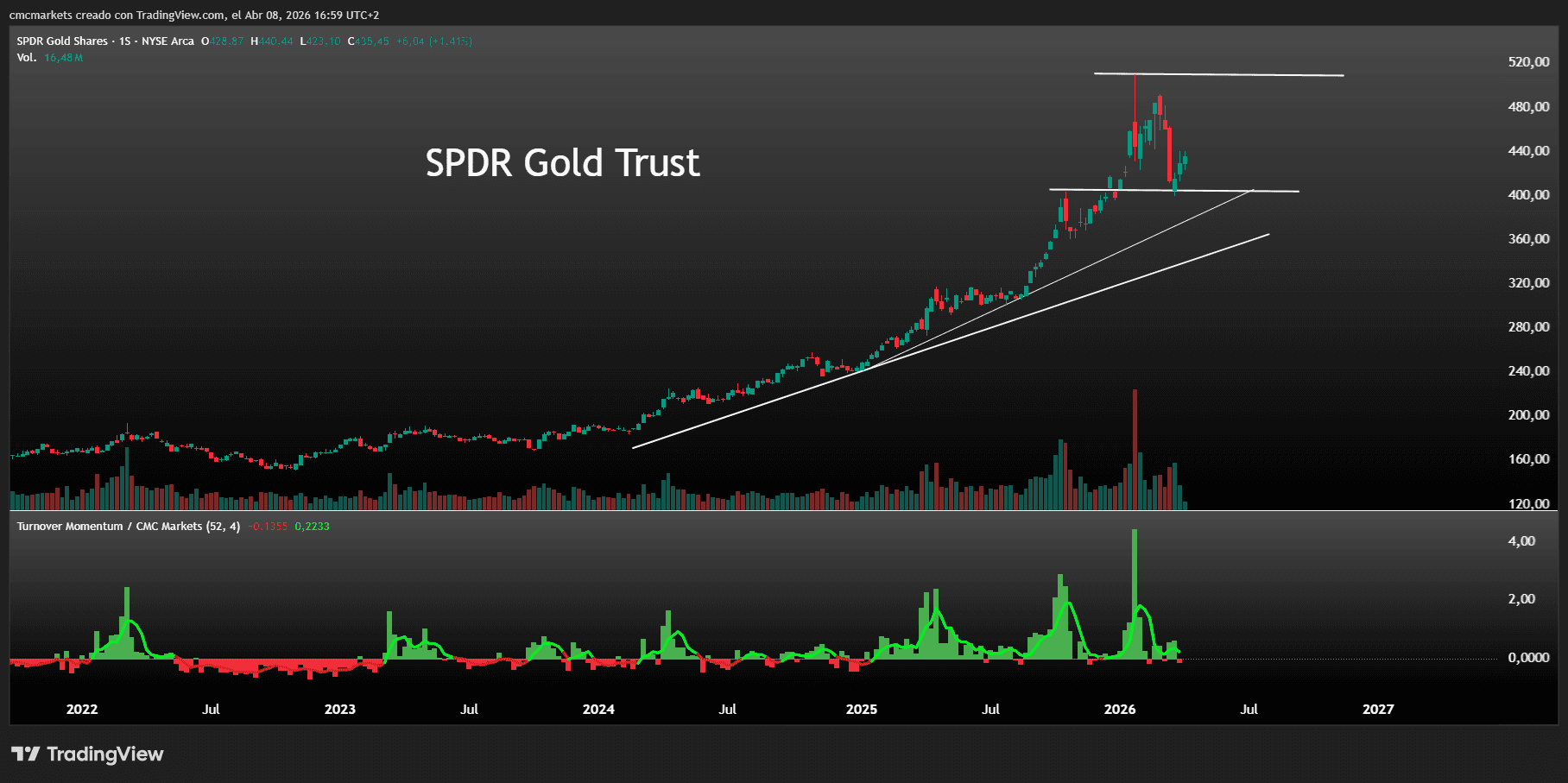

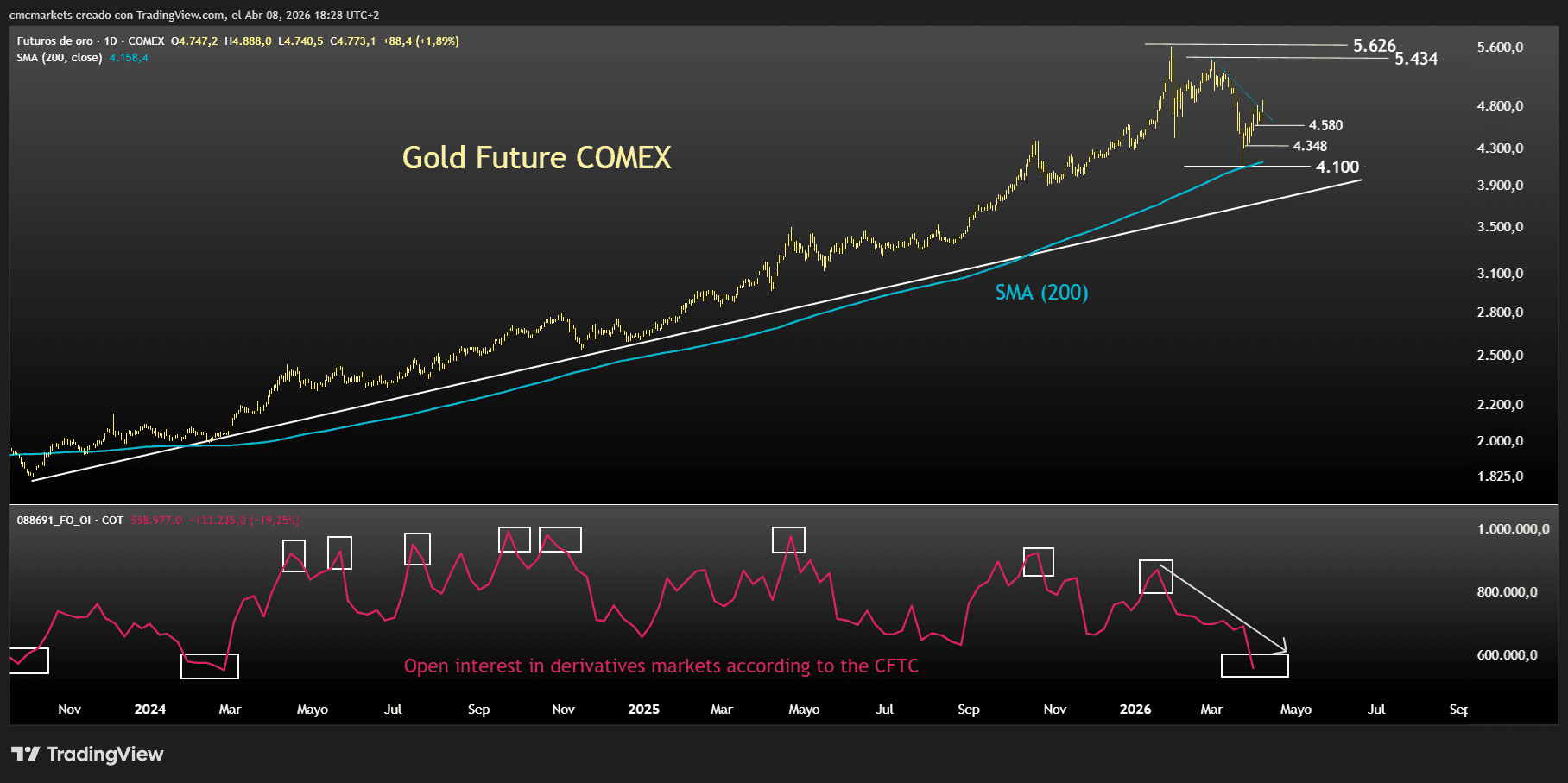

Liquidity, retail selling and long-position cuts

The fall in gold during one of the most acute phases of the war with Iran may be explained by a combination of liquidity demand, retail selling and the reduction of trend-following long positions. That is the message from the latest World Gold Council report, which suggests the move was driven less by a loss of safe-haven appeal and more by forced positioning adjustments.

Flows point to retail selling and long reductions

According to the World Gold Council, 84.8 tonnes of gold were sold through exchange-traded funds in March, a vehicle more commonly used by retail investors. Outflows totalled 87 tonnes in the US and 7.3 tonnes in Europe, partly offset by inflows of 9.9 tonnes in Asia.

At the same time, the non-reportable category in derivatives markets, also associated with retail investors, recorded a reduction equivalent to 18 tonnes of gold. Trend-following participants, grouped in the managed money category, also cut long positions as the price broke below key moving averages. Momentum strategies appear to have played an important role in accelerating the correction.

SPDR Gold Trust, daily