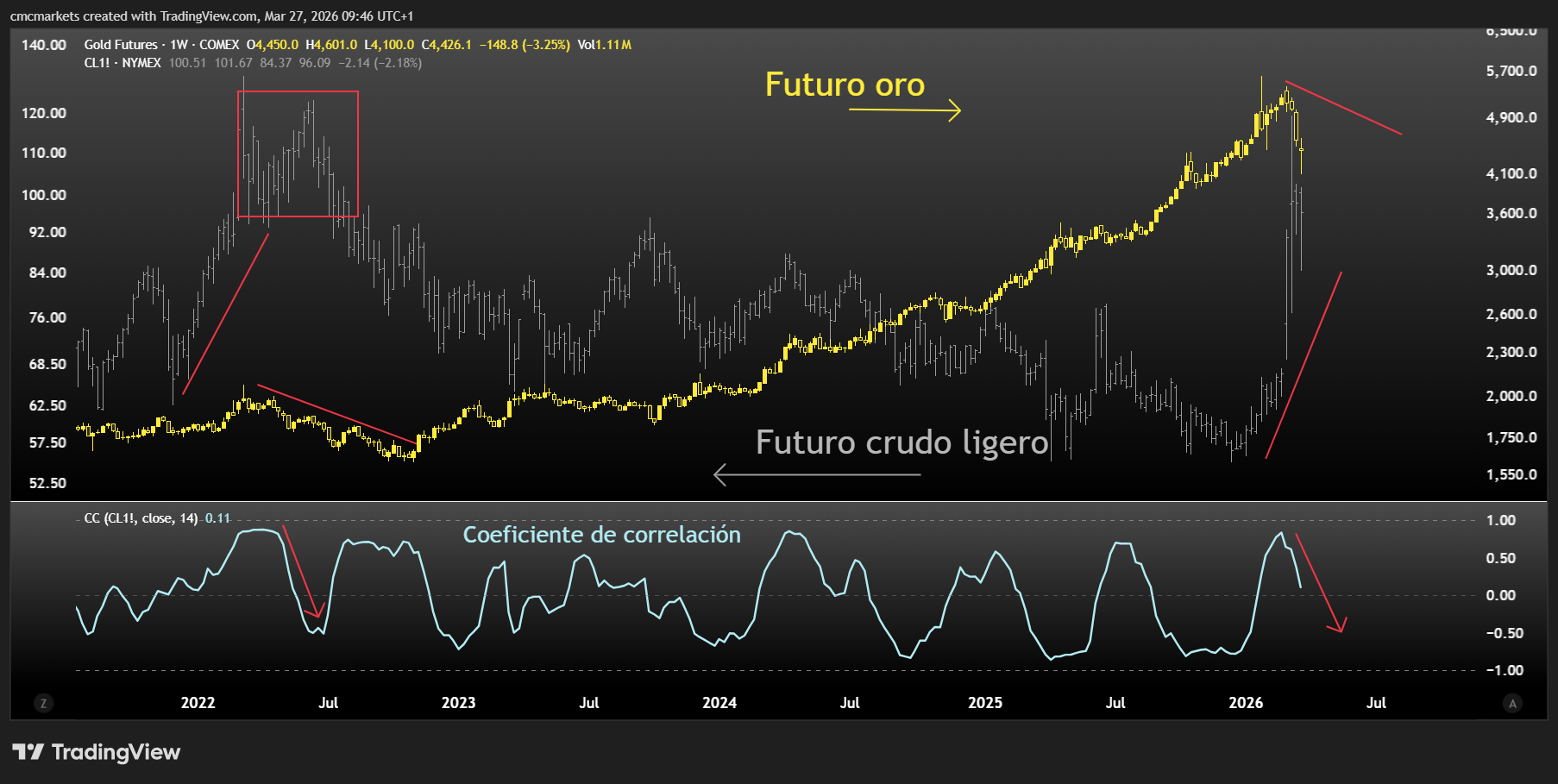

Gold has underperformed during the latest shock

Gold has shown greater relative weakness than the S&P 500 during the latest Middle East crisis. Since the conflict escalated, the metal has fallen by more than $1,000 an ounce, around 20%, while the S&P 500 has been more resilient with a drawdown closer to 5%.

That underperformance, combined with gold's recent positive correlation with equities, has reopened the debate over whether it is still behaving as a true hedge when geopolitical stress intensifies.

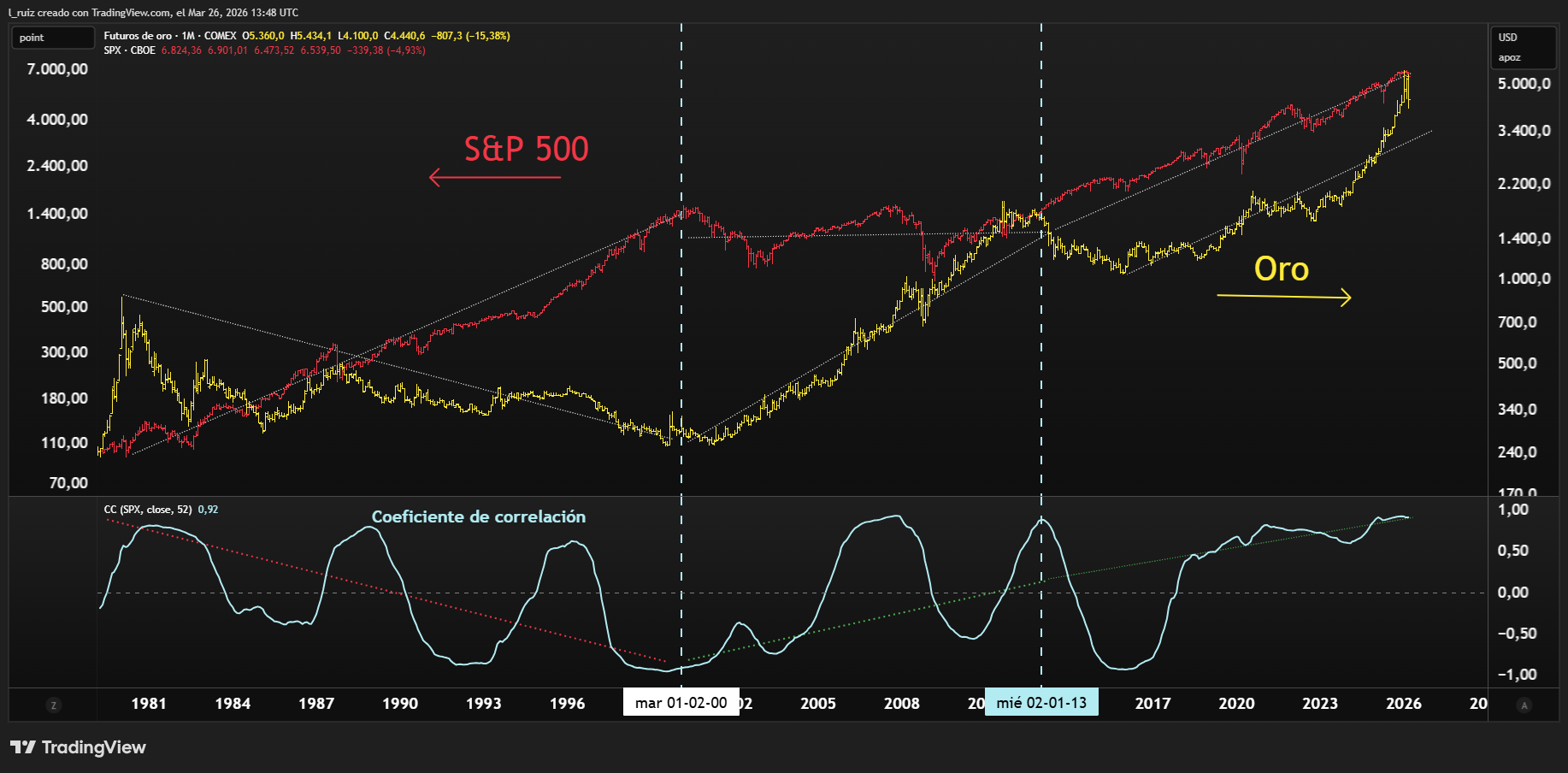

The longer-term record still supports gold's role

Despite the current noise, the longer-term picture from 1980 to 2026 still supports gold as a non-correlated and complementary asset. During the strong equity expansion of the 1980s and 1990s, gold remained in a structural downtrend, while in the crisis period from 2000 to 2012 it behaved much more like a defensive asset as the dotcom bust and the global financial crisis hit equities.

That history matters because it suggests the current episode may be distortion rather than proof that gold has permanently lost its defensive function.

Source: TradingView. 26 March 2026.