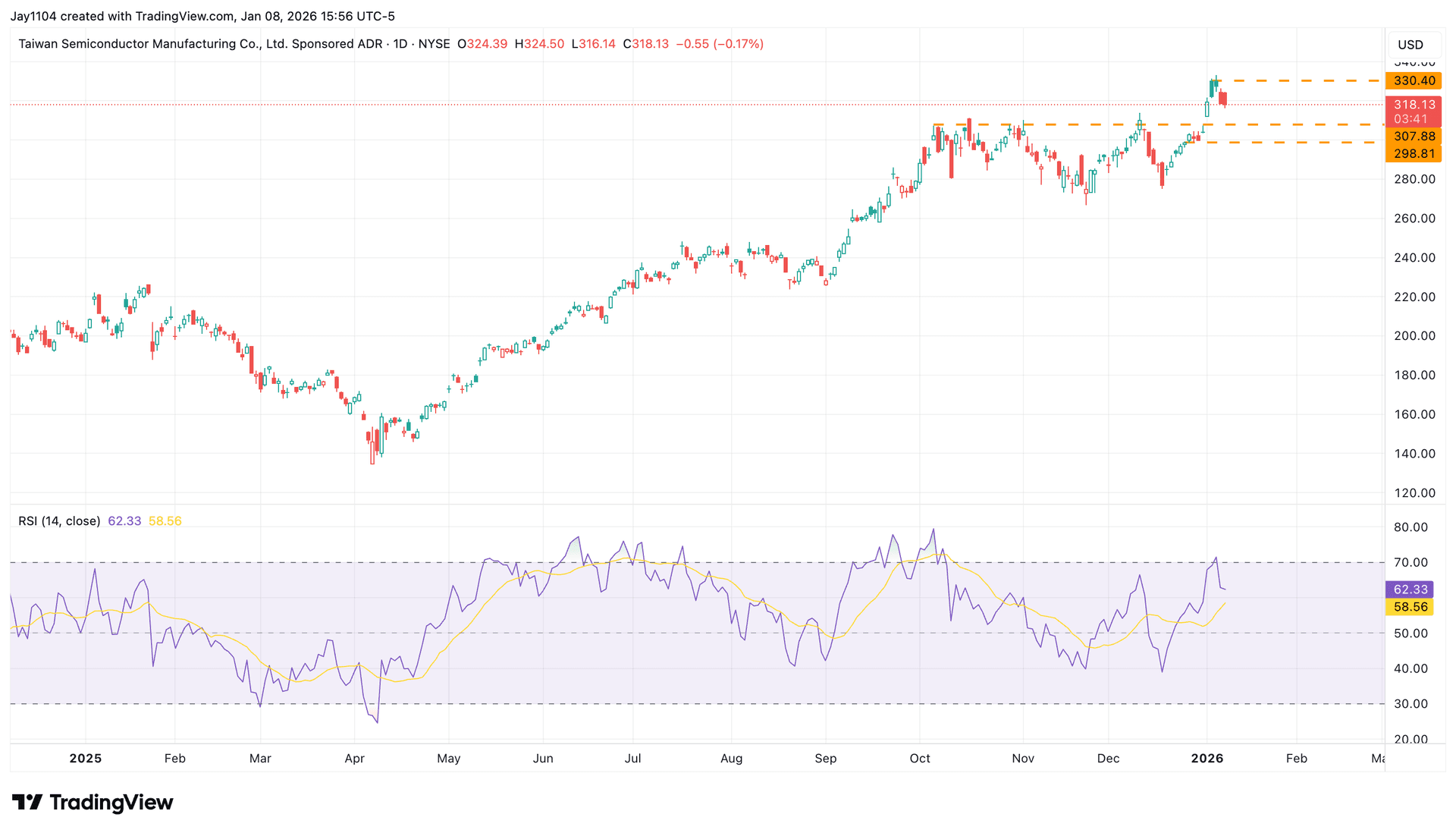

There will be a slew of economic data from the US in the coming week, including updates on consumer and producer prices, as well as retail sales. Leading eurozone nations will also release consumer price index figures, with Germany’s print set to carry added significance given the low preliminary reading of 1.8% issued earlier this month. On the corporate front, US banks kick off a fresh earnings season from Tuesday, with the biggest of them all – JPMorgan – leading the charge. Meanwhile, those with an interest in the AI trade will be paying close attention to fourth-quarter results from Taiwan Semiconductor Manufacturing (TSM) on Thursday – the New York and Taipei dual-listed company is Nvidia’s primary chip supplier.

US December CPI

Tuesday 13 January

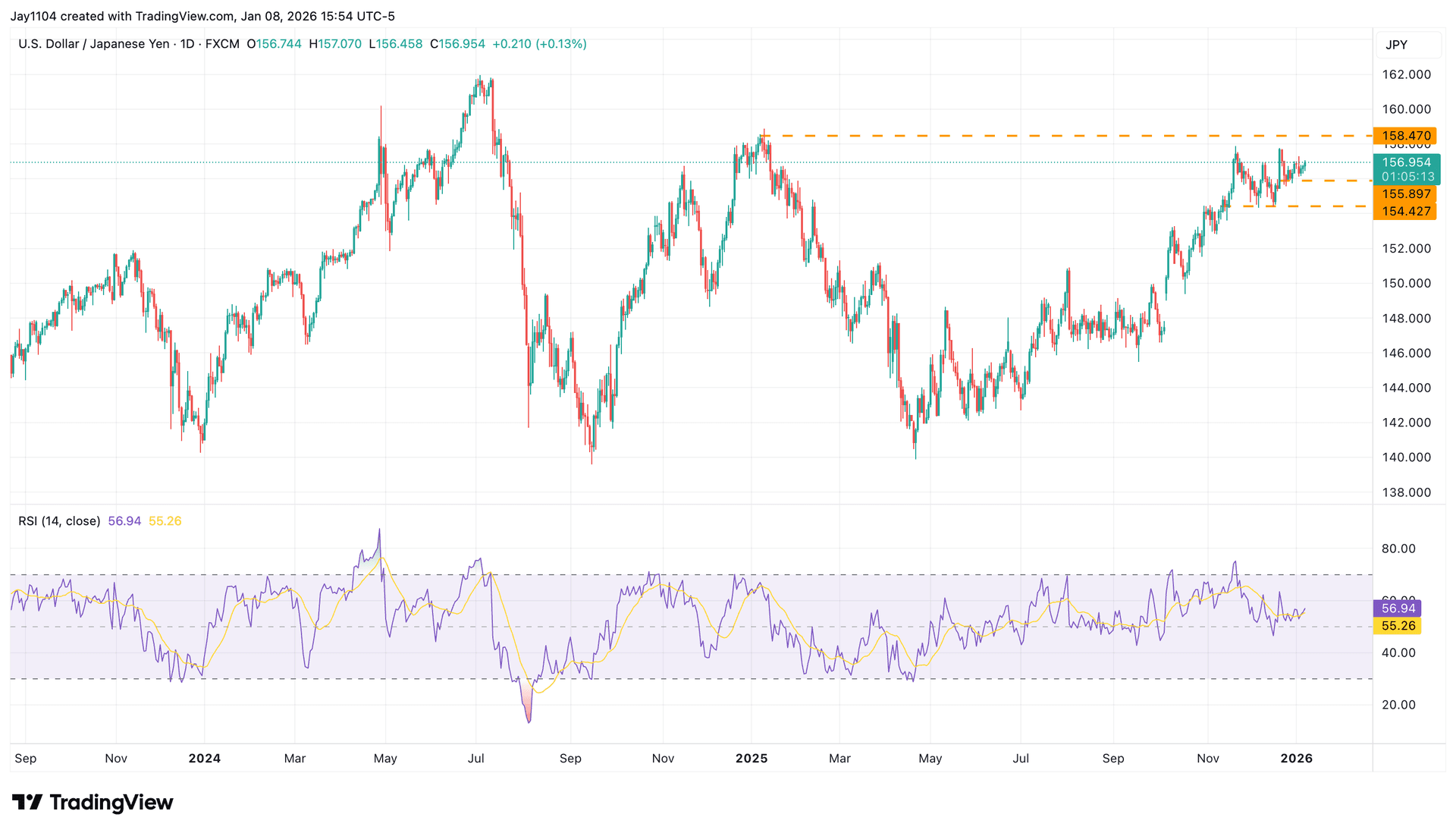

The US consumer price index (CPI) report for November surprised the market as the headline measure of annual inflation and core CPI, which excludes volatile items like food and energy, fell to their lowest levels since July 2025 and March 2021, respectively. Despite ongoing fears that tariffs could prove inflationary, headline CPI eased to 2.7% in November while core CPI cooled to 2.6%, both down from 3% in September, the last month in which data was collected before the government shutdown. Looking ahead to the upcoming release, consensus expectations seem to be that headline CPI remained stable, up 2.7% in the year to December, while core CPI edged higher to 2.7%, based on data available on the prediction market Kalshi. While the November readings may have been negatively affected by patchy data collection at the tail-end of the government shutdown, which ran from 1 October to 12 November 2025, the December figures ought to be based on a full month of data. This imbalance brings the risk of a surprise in the forthcoming inflation report. If the December data beats or misses estimates, currency markets may see some volatility, particularly . The Japanese yen should be strengthening against the dollar, given that in December the Bank of Japan raised its benchmark interest rate to 0.75%, its highest level in 30 years, while in the same month the US Federal Reserve cut interest rates. However, the yen has remained weak against the greenback. On Friday, the yen weakened past ¥157.50 per dollar. One factor that could drive further yen weakness, potentially pushing USD/JPY towards ¥158.50 and possibly beyond, would be a hotter-than-expected US CPI report, which could lead to a material strengthening of the dollar against its FX peers.