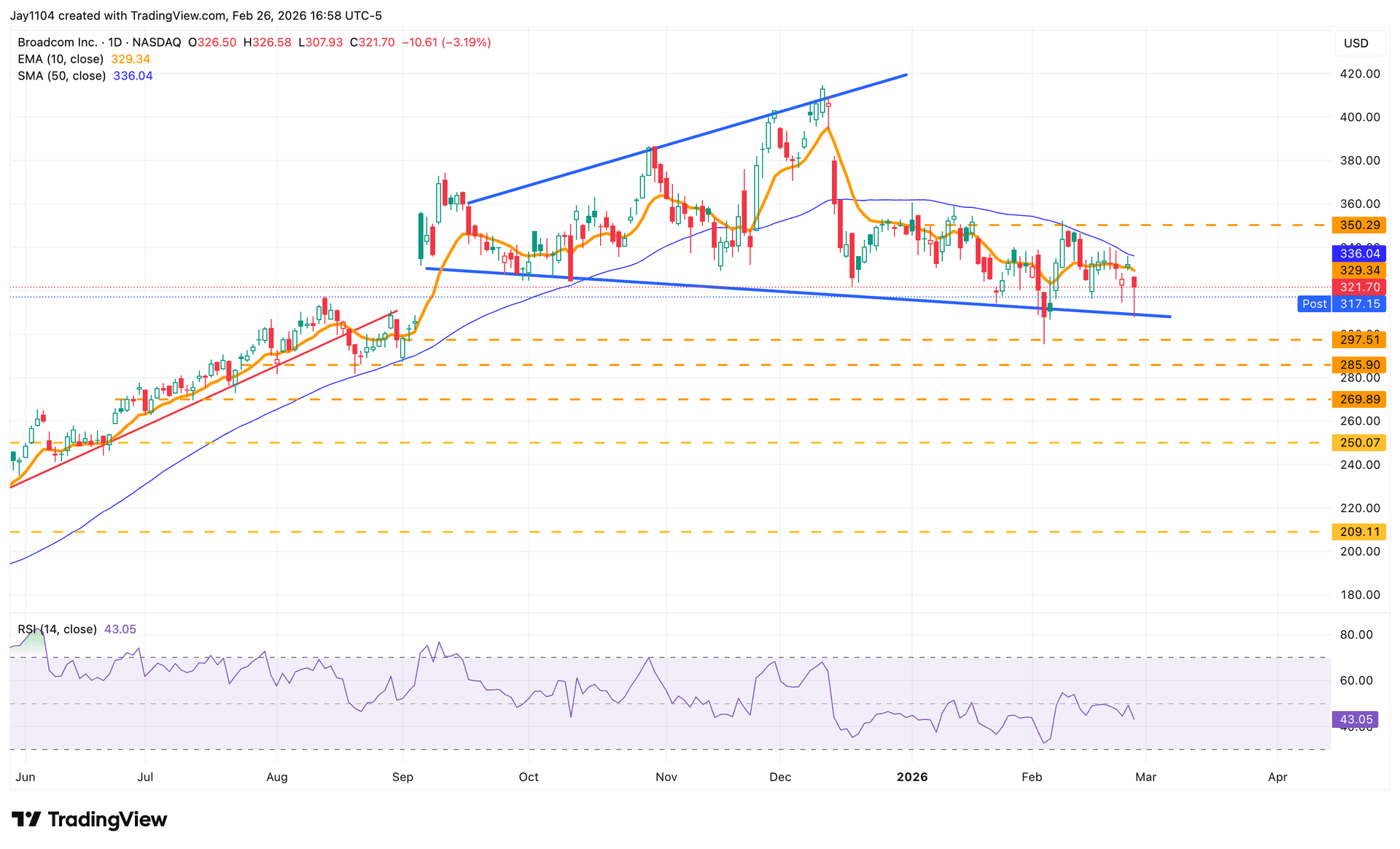

Published: Friday, 27 February 2026 at 12:10 (UK) Welcome to Michael Kramer’s pick of the key market events to look out for in the week beginning Monday 2 March. US economic data will come thick and fast, with the ISM manufacturing and services reports, the ADP private payrolls release and the US non-farm payrolls report all scheduled. Alongside this, artificial intelligence (AI) is likely to remain central to traders’ focus, with chipmaker Broadcom set to report its first-quarter results on Wednesday. Following the downbeat market reaction to Nvidia’s Q4 results, there may be added pressure on Broadcom to present a clearer and more convincing outlook for investors.

US February ISM data

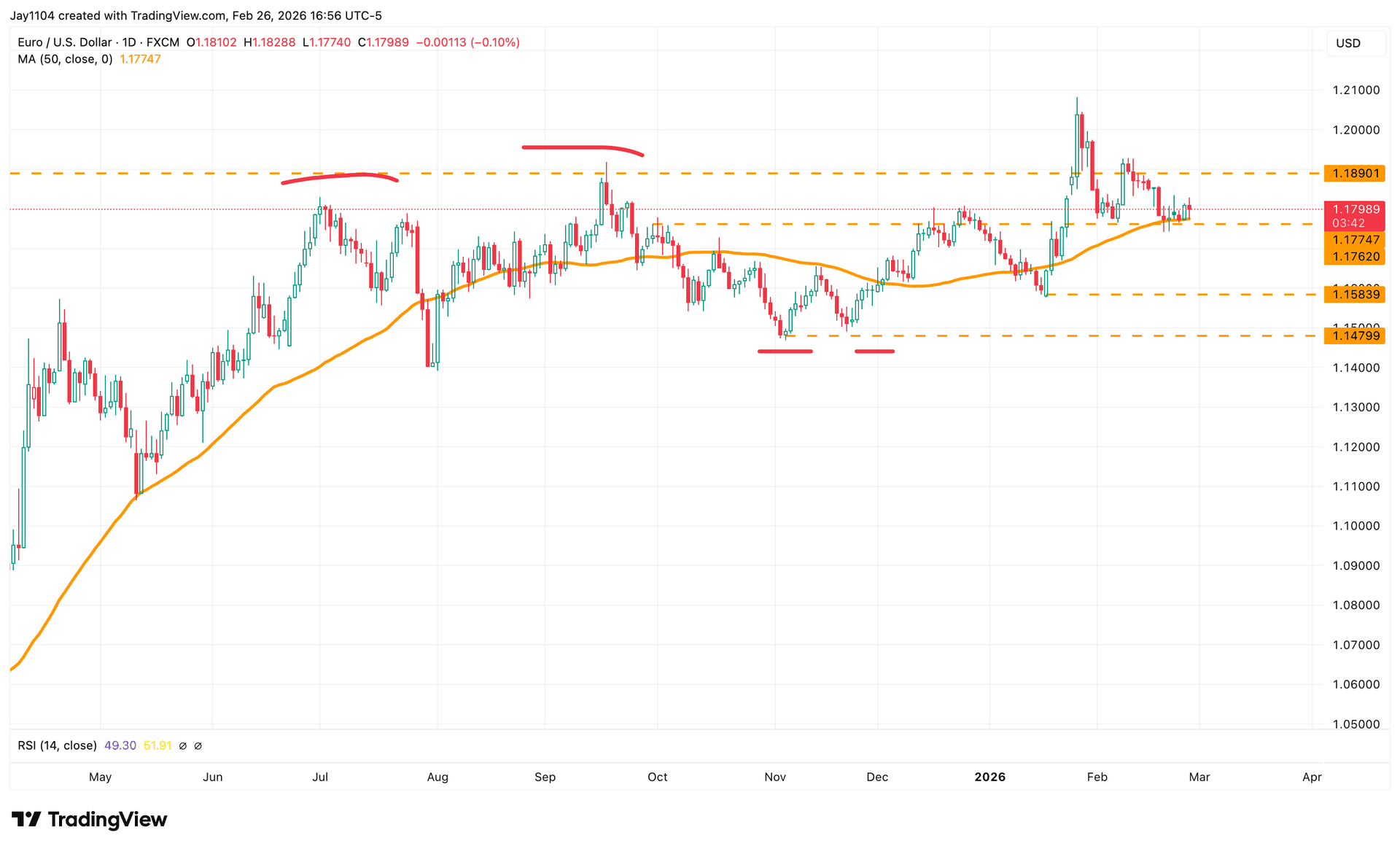

Monday 2 March (manufacturing PMI) Wednesday 4 March (services PMI) The Institute for Supply Management’s (ISM) purchasing managers’ index (PMI) reports will provide a snapshot of how the US manufacturing and services sectors performed in February. The manufacturing report is expected to show that the sector remained in expansion territory with a reading of 52.3, albeit down slightly from 52.6 in January. Meanwhile, activity in the services sector is thought to have edged up, with an expected reading of 54, versus 53.8 in January. These reports – widely regarded as a barometer of the health of the US economy – are likely to influence whether the dollar’s recent rebound can continue. In particular, EUR/USD may be sensitive to the data. The pair is currently trading near support at $1.18 per euro, which aligns with the 50-day moving average. A break below this level, perhaps driven by stronger-than-expected ISM readings (which tend to be bullish for the dollar), could send the pair down towards $1.158, and potentially $1.147. In contrast, weak readings might allow EUR/USD to test resistance near $1.19.