Attention is on the US consumer price index (CPI) this Friday at 1.30pm (UK time). Consensus, surveys, and models all agree that inflation will continue moderating, allowing the Federal Reserve to maintain its pause on interest rates.

With the economy in full normalisation, the focus now shifts to the impact on the US dollar and gold. This is a high-impact figure with the potential to generate immediate volatility in the dollar, stock markets, and bond markets.

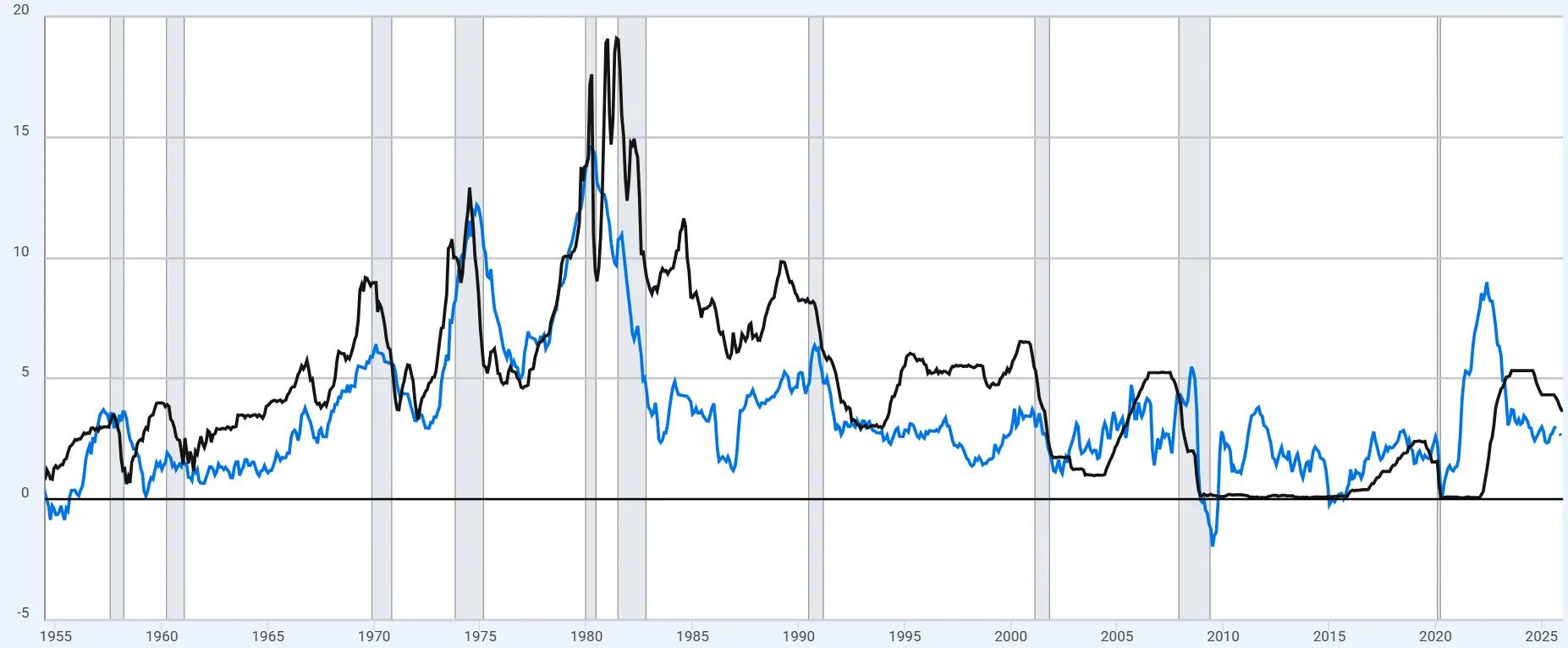

US inflation expected to keep declining

Market consensus, compiled by Trading Economics, expects both core and headline inflation to reach 2.5% year-on-year in January. If confirmed, these would be the lowest core inflation levels in the past five years and annual lows for headline inflation.

Downward trend brings inflation closer to Fed target

The disinflationary trend aligns with consumer inflation expectations measured by the New York Fed, which have also declined toward recent lows. At the same time, the Cleveland Fed’s nowcasting model suggests the surprise could be even stronger, projecting 2.36% for headline CPI and 2.45% for core CPI.

If this trend is confirmed, inflation would continue its path toward the Fed’s 2.0% target, definitively leaving behind the spike seen in September 2025 caused by tariffs introduced by the Trump administration.