Revolut IPO: what investors need to know

British fintech giant Revolut is expected to pursue a public listing, which could be significant relative to recent European IPOs. Find out more about a potential Revolut IPO, including possible timing, valuation, company financials, risks, and what access may look like if shares become publicly available.

- :

- :

Past performance is not a reliable indicator of future results

What does Revolut do?

Revolut is a digital financial services company that operates as a mobile-first alternative to traditional banks. Founded in 2015 by Nikolay Storonsky and Vlad Yatsenko and headquartered in London, the company now serves over 52.5 million customers across more than 38 countries (Revolut Annual Report, April 2025). It holds a European banking licence and was granted a UK banking licence with restrictions in July 2024.

Revolut’s core products and services

Multi-currency accounts – users can hold and exchange over 25 fiat currencies at interbank rates, with low-fee international transfers.

Stock and crypto trading – customers can invest in stocks, cryptocurrencies, and commodities directly from the app.

Subscription plans – Plus, Premium, Metal, and Ultra tiers offer perks such as cashback, travel insurance, and airport lounge access.

Business accounts – tailored solutions for companies and freelancers, including corporate cards, expense management, and multi-currency payments.

Lending services – personal loans, credit cards, overdrafts, and buy-now-pay-later (BNPL) products, with mortgages being tested in the UK.

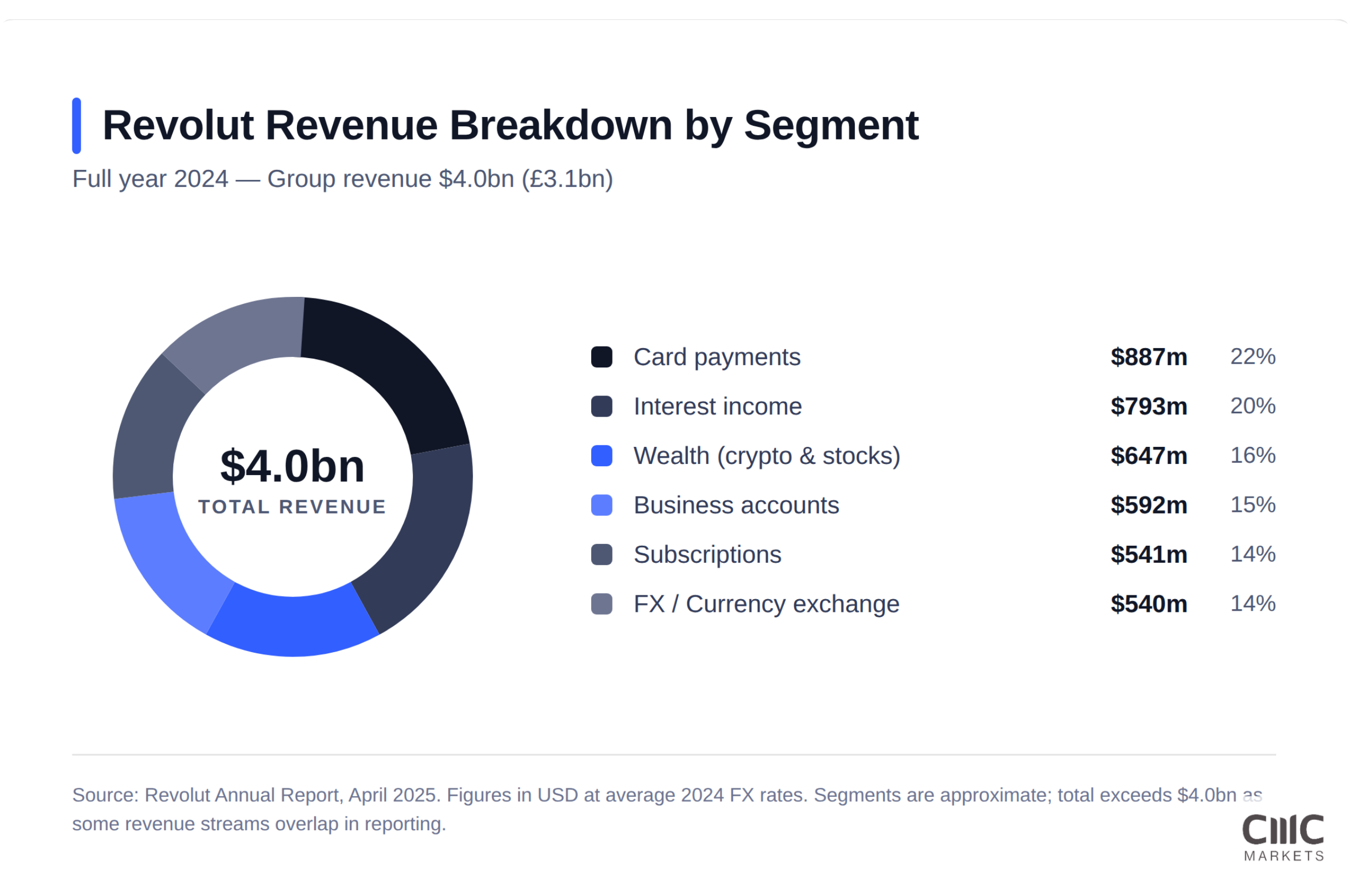

How does Revolut make its money?

Past performance is not a reliable indicator of future results

Revolut operates as a digital financial super app, delivering banking, payments, and investment services through its mobile platform. Unlike traditional banks, it does not rely on physical branches. Instead, it runs a technology-driven model designed to reduce certain operating costs compared with traditional branch-based banks

Revolut’s revenue comes from several key streams – here’s more on the main ones.

Card interchange fees – Revolut earns a small percentage from each card transaction. The merchant pays this fee, not the user. The more transactions processed, the higher the revenue. Card payments generated $887m in 2024, up 43% year on year (Revolut Annual Report, April 2025).

Subscription plans – Revolut offers Plus, Premium, Metal, and Ultra plans, providing perks like higher withdrawal limits, travel insurance, cashback, and airport lounge access for a monthly or annual fee. Subscription revenue ensures predictable recurring income.

Currency exchange – While Revolut offers interbank exchange rates on weekdays, it charges a markup on weekends and for high-volume transactions, generating revenue from forex conversions.

Wealth products – users can buy and sell stocks, cryptocurrencies, and commodities through the app. Revolut earns from commissions, spreads, and withdrawal fees. This segment generated $647m in 2024, up 298% year on year, making it the fastest-growing revenue stream (Revolut Annual Report, April 2025).

Business accounts – Revolut Business offers accounts tailored for companies, freelancers, and entrepreneurs, providing features like multi-currency payments, corporate cards, and expense management. Revenue comes from monthly fees and payment processing charges. The segment contributed $592m in 2024, about 15% of total group revenue.

Lending services – Revolut generates income from personal loans, credit lines, overdrafts, and BNPL products. It earns through interest charges and loan fees. Customer loans grew 86% year on year to $1.3bn in 2024.

What is the Revolut IPO date?

Revolut has not set an official IPO date. In a December 2025 interview, CEO Nik Storonsky said a listing is “most likely” two to three years away, according to a report by Connecting the Dots in FinTech (December 2025). That pushes the earliest likely window to 2027 or 2028.

Earlier reports, including a March 2025 piece from The Wall Street Journal, had suggested a 2026 listing was widely expected. However, Revolut’s completion of a $75bn secondary share sale in November 2025 appears to have reduced the urgency, giving employees liquidity without the pressure of a public offering.

The listing venue also remains undecided. Storonsky has indicated a preference for the US, most likely Nasdaq, citing stronger liquidity and higher valuations for tech companies. The UK government continues to lobby for a London listing, and some reports suggest Revolut may pursue a dual listing in both cities. For UK investors, the eventual listing location could affect ISA eligibility and trading hours.

What could Revolut be worth at IPO?

Past performance is not a reliable indicator of future results

Revolut’s valuation has risen sharply in recent years. A secondary share sale finalised in November 2025 valued the company at $75bn, up from $45bn in August 2024 and $33bn in 2021. Shares in that latest sale changed hands at approximately $1,381 each (Dakota Research, January 2026).

At $75bn, Revolut’s implied valuation already sits alongside established banks such as Barclays and Société Générale. Analysts suggest the IPO valuation could range from $60bn to over $100bn depending on market conditions, growth trajectory, and investor appetite at the time of listing. Comparable publicly listed fintechs include Wise (LSE, market cap roughly £8bn), Nubank (NYSE, approximately $50bn), and SoFi (Nasdaq, around $15bn).

These figures are estimates, not guarantees. Valuations can shift considerably based on market sentiment, profitability trends, regulatory developments, and broader economic conditions. Past valuation levels are not a reliable indicator of future performance.

How can investors get exposure?

How are Revolut’s financials looking?

Past performance is not a reliable indicator of future results

Source: Revolut Annual Reports, April 2025. GBP is the reporting currency; USD figures use average exchange rates.

Revolut delivered its fourth consecutive year of profitability in 2024. Revenue rose 72% to £3.1bn ($4.0bn), while profit before tax climbed 149% to £1.1bn ($1.4bn). The company added nearly 15 million new customers during the year, and total deposits surged 66% to £30bn. All four core segments – card payments, foreign exchange, subscriptions, and wealth – reported growth.

Investors considering the Revolut IPO will typically look at whether this trajectory is sustainable. Key metrics to watch include customer acquisition costs, revenue per user, deposit growth, and the company’s ability to diversify beyond interchange fees into higher-margin products such as lending and wealth management. Past performance is not a reliable indicator of future results.

Why are investors interested in this IPO?

Revolut has grown from a currency-exchange app into a broad financial platform in under a decade. The company now offers banking, trading, insurance, and business tools – and its 52.5 million user base makes it one of the largest digital banks in the world by customer count. That kind of scale, combined with 72% annual revenue growth, is rare in any sector.

The global digital banking market is projected to reach hundreds of billions in value over the coming years, and Revolut aims to expand its market share, though competitive and regulatory factors may influence its ability to do so.. Its acquisition of a UK banking licence in 2024 opens the door to deposit protection, mortgages, and commercial lending, which could deepen customer relationships and boost revenue per user.

Revolut has also invested heavily in AI-powered fraud detection, which the company says protected customers from over $800m in potentially fraudulent transactions in 2024 (Revolut Annual Report, April 2025). Plans for an AI assistant and continued product expansion suggest the company is not standing still. That said, strong interest does not guarantee strong returns, and investors should weigh the growth story against the risks outlined below.

What are the risks and challenges?

Revolut’s UK banking licence remains restricted under a standard “mobilisation” period. Until the company completes this phase, it cannot fully operate as a UK bank. The company has also faced regulatory scrutiny in the past, including concerns over its anti-money-laundering processes and a 2022 cyberattack that exposed data from over 50,000 customers. A £3.5m fine from Lithuania’s central bank in 2023 for compliance failings adds to this picture. Any future regulatory setbacks could delay the IPO or affect the share price at listing.

Competition is intensifying from multiple directions. Traditional banks such as Barclays and HSBC are investing heavily in digital services, while neobank rivals Monzo and Wise continue to grow. Monzo, which has over 10 million UK customers, is also reportedly targeting an IPO. Unlike Klarna, which has built strong international traction, Revolut still relies on the UK for a significant portion of its revenue, which concentrates its risk.

Broader market conditions also matter. Interest-rate movements, geopolitical tensions, and shifts in investor appetite for fintech stocks could all influence the timing and pricing of the Revolut IPO. Recent fintech IPOs have delivered mixed results – Wise, for example, listed on the LSE in 2021 and has seen its share price fluctuate considerably since then. Investors should consider that the IPO market can be unpredictable, and past listings do not guarantee future outcomes.

Who are Revolut’s competitors?

The digital banking space is crowded and competitive. Revolut faces challengers from fintech startups, payment giants, and traditional banks alike.

You can trade or invest in these listed stocks while you wait for Revolut’s IPO.

What sets Revolut apart is the breadth of its product suite. While Wise focuses on transfers and Monzo on current accounts, Revolut combines banking, trading, crypto, insurance, and business tools in a single platform. Its $75bn valuation also places it in the same bracket as some traditional banks, which few fintechs have achieved. Amazon-backed Kuiper and Microsoft’s Azure may not be direct rivals, but the broader tech industry’s interest in financial services keeps the competitive pressure high.

Disclaimer: CMC Markets is an execution-only service provider. The material (whether or not it states any opinions) is for general information purposes only, and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by CMC Markets or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although we are not specifically prevented from dealing before providing this material, we do not seek to take advantage of the material prior to its dissemination.

Ready to get started?

If you already have an account, log in to your chosen platform.

Don't have one yet? Open an account now.